fruit logistica 2012

DESCRIPTION

Especial Quien es QuienTRANSCRIPT

¡Síguenos!

@AmaliaMercados / @RevistaMercados (Twitter)

RevistaMercados (Facebook)

EDITA: Laméyer S.L. DIRECCIÓN: Amalia del Río Laméyer REDACCIÓN: Alicia Lozano, Marga López PRODUCCIÓN EMPRESAS: Alicia Lozano, Marga López ADMINISTRACIÓN: Jorge Cobos. Fotografías Interiores: Laméyer S.L. y otros TRADUCCIÓN: Lázaro Entrenas DISEÑO Y MAQUETACIÓN: Juan Olivares DISEÑO PORTADA: Circus. FOTOGRAFÍA PORTADA: Planasa. Variedad Sabrina REDACCIÓN Y ADMINISTRACIÓN: Ctra. Sevilla-Málaga, Km. 1. Mercasevilla 41020 Sevilla. Teléfono: 954 25 88 51 - 954 25 71 25 Fax: 954 25 19 94 E-mail: [email protected] - www.revistamercados.com FILMACIÓN E IMPRESIÓN: Escandón Impresores Dep. Legal; SE - 917 - 1994 La editora no se hace responsable de los contenidos fi rmados por cada autor, ni tiene porqué compartirlos. Se prohíbe la reproducción total o parcial de los artículos publicados.

en el mercado europeo

AMALIA DEL RÍO, DIRECTORA REVISTA MERCADOS

Em

Mistrust in the European marketA new edition of Fruit Logistica has arrived under the shadow and mistrust generated by the E. coli food crisis, which resulted in consumption decrease and consequently in price fall for the Spanish sector of fruits and vegetables.There is no happiness, the hope that surrounded this event in previous years has vanished, and the year that just ended was a very difficult one for the sector, which learnt a lesson, above all, that it doesn’t matter how hard they worked to obtain safe products because it could become unsafe in just a

blink. All this, together with the economic crisis, drove to a critical situation that ruined many, a situation from which it is difficult to escape as there is no promising future; things are not going to change much.But there is still the hope that crisis times are times for opportunities too for those who dare to innovate and trust their possibilities. We reflect on our pages the concerns of a sector that fights every day, as the Commissioner for Agriculture Dacian Ciolos well said, to have quick reaction capacity against crises that helped them to carry on.

Personalidades / Personalities

Fruit logística ’124

Es

DE UNA CAPACIDAD DE REACCIÓN RÁPIDA ANTE LAS CRISIS”

COMISARIO EUROPEO DE AGRICULTURA Y DESARROLLO RURAL DESDE 2010.

DACIAN CIOLOS,

“We need to acquire the capacity to quickly react against crises”

Dacian Ciolos, European Commissioner for Agriculture and Rural Development since 2010.

It is a pleasure to take part in this special issue of Mercados journal on the occasion of Fruit Logistica 2012. In each edition, this trade fair shows with splendour the diversity and significance of the sec-tor of fruits and vegetables for Spain, and also for the European Union on the whole.The year 2011 has been a difficult one, and it will remain in everyone spirits’ as the year of the E. coli crisis, no doubt. Evidently, such a crisis lasts always too long and violent. But I would like to highlight that, without your work, and the sound strap of trust that has been woven year after year with consum-ers, this chapter would have surely been pretty much longer. European consumers are back into fruits and vegetables. We must seize every opportunity to tell them to what extent consuming these products is good for our health, and to tell them how convenient is developing good habits at a young age. This is what drove me to suggest, within the CAP reform, a

significant amount of the budget allocation for the “School fruit” scheme.I would also like to take advantage of this oppor-tunity to insist in the need of acquiring the capac-ity to quickly react against the crises that threaten to sweep complete sectors of our agriculture. As we saw regarding E. coli, the key for an effective crisis management lies on our capacity of quick reaction, before it’s too late. That is what we exceptionally achieved this year. But we must be better equipped not to be disarmed in the worst moment, typical of juridical errors. For that reason, I proposed to set in motion an enlarged urgency clause that will enable us to quickly solve crises, from 2013 on.Parallel to the CAP reform, I will closely track the sec-tor of fruits and vegetables, and I will analyse its evolution. We must give response to the insufficient payment to growers on one hand, which raises an is-sue of economic health within the sector, and on the

other hand, to the problem of structural slowdown of consumption of fruits and vegetables, which raises an issue of public health for the whole society.I’m sure that the sector of fruits and vegetables has all the means to face these two big economic and citizen challenge. It offers consumers a wide range of healthy, quality products that allow for reducing the risks of cardiovascular diseases and cancer. We have a dynamic sector in Europe, able to mobilise professional competences unlike any other in the world.Besides, the sector’s dynamism translated in the lat-est years into avant-garde approaches, not only as for production techniques but also regarding direct or online contact between producers and consumers.For all these reasons, I trust in the future and the capacity of the sector to be further innovative and better organised, aiming at facing tomorrow’s chal-lenges.

Fruit logística

Fruit logística ’12 5

Personalidades / Personalities

Fruit logística ’126

El

PARA EL NUEVO MINISTRO

Big challenges for our Minister

The year 2011 bade farewell with the appointment of Miguel Arias Cañete as Minister for Agriculture, Food, and the Environment, which meant a double recovery; on one hand, Arias Cañete holds this position again, as he also did between the years 2000 and 2004, on the others, the name “agriculture”, something much acclaimed by many the sector.Nevertheless, Arias Cañete arrives at the Ministry with a very important task ahead. Part of it would be achieving that the imminent reform of the CAP didn’t avoid the major claims of Spanish agriculture; the other part, focusing on fruits and vegetables, that the renewal of the Association agreement between the EU and Morocco didn’t finally displace Spanish products out of European markets.It’s been hardly a month since he was appointed and, during these weeks, we all could see how the Minister’s agenda got filled with meetings and appointments, all them preceded by endless compliments from every link of the value chain. For the Spanish Agro-food cooperatives, the sectors gains weight in Europa thanks to this appointments, at the same time it claims for policies that allowed for restoring the balance in the agro-food chain, strengthening supply concentration and commercial integration of producers, a matter in which cooperatives must be the main players. In this sense, Arias Cañete stated that supply concentration and cooperative integration are two necessary factors to improve the sector’s competitiveness and to restore the balance in the agro-food chain; he also showed himself willing to work hand-in-hand to search for

the most adequate instruments to accomplish both objectives.In turn, the professional association HORTYFRUTA asked him to firmly support measures yet to come to reactivate the sector of fruits and vegetables in Andalusia, as would be a Law on Quality, as well as changes that introduced Template Contracts for trade of fruits and vegetables, and actions against abuse of agro-food distributors that are driving producers of fruits and vegetables to bankrupt. Regarding the Association Agreement between the EU and Morocco, he affirmed to FEPEX that his ministry asked the European Commissioner for Agriculture, Dacian Ciolos, for a reform of the entry prices system in order to avoid the social dumping that Moroccan tomatoes bring by entering the EU even below production costs.Likewise, speakers from FEPEX said that they consider Miguel Arias Cañete a sound asset to solve the crisis in the sphere of agriculture, particularly within the sectors of fruits and vegetables, given his expertise and knowledge of agricultural and Community policy, as well as of how European institutions work.Thus, we face a true challenge for the new Minister and the new Ministry (MAAMA for its name in Spanish), with many obstacles to overcome and many sectors to be contented. Let’s hope that when it comes to make a review in four years’ time, we will be able to write down a long list with all those accomplished goals, and above all, we will see how our agriculture gains back the political, social, and institutional significance it deserves.

Fruit logística

Fruit logística ’12 7

Personalidades / Personalities

Fruit logística ’128

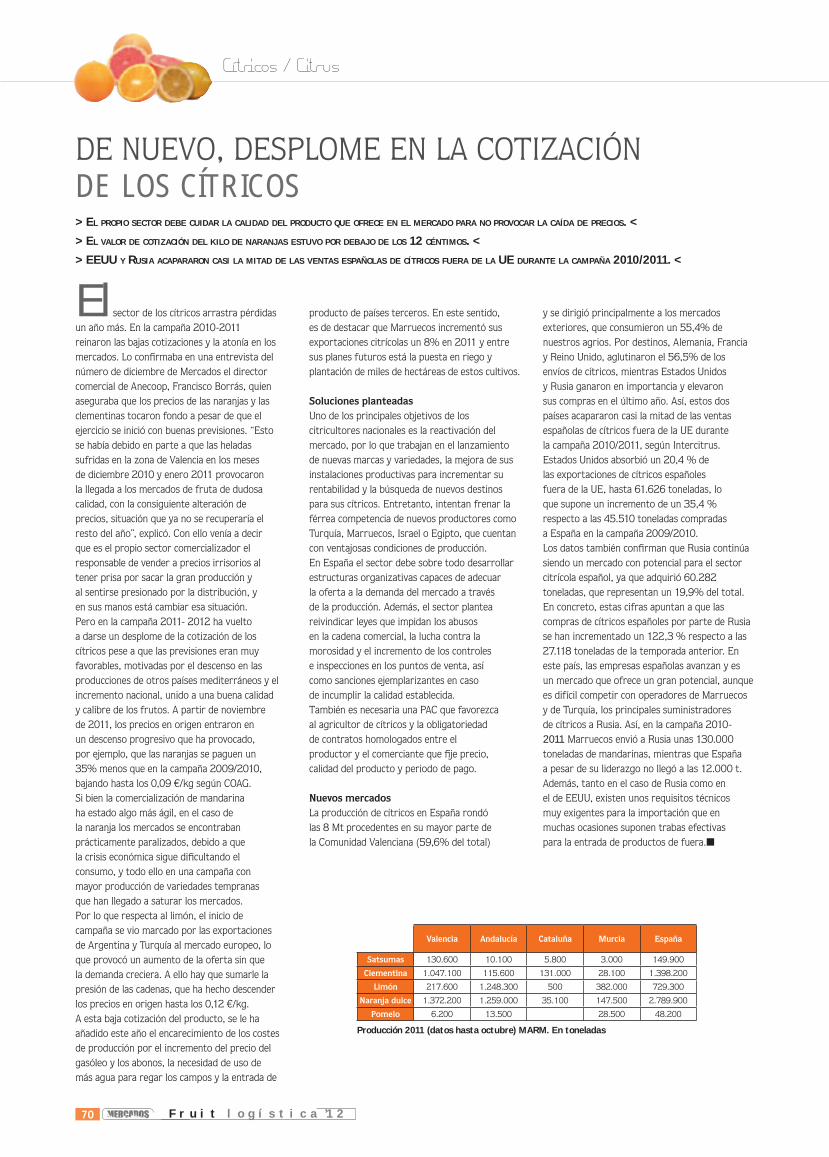

Una de las principales características del sector hortofrutícola español es su importancia económica, que ha seguido una evolución creciente tanto en valor como en su contribución al conjunto del sector agrario, pues es la principal rama de la producción agraria de España. En 2009, representó, con 14.500 millones de €, el 61,1% de la producción

relación a los años anteriores; en 1998 representaba el 51% y en 2002 el 55%. Es previsible que la tendencia creciente de la participación del sector en la producción agraria se incremente en el futuro como consecuencia de la aplicación de la reforma de la PAC y el consiguiente desacoplamiento de las ayudas. En España, este sector está orientado claramente a la exportación, que supone el 40% de la producción por término medio, llegando en algunos casos hasta el 70% de la producción, como es el caso de los cítricos, o las producciones hortícolas de invernadero. La producción de frutas y hortalizas alcanzó en 2009 las 24.500.000 t, de los cuales el 63,2% del volumen total correspondieron al grupo de hortalizas y patata, en particular a tomate, cebolla, melón y pimiento. Le siguieron en importancia los cítricos, con el 22,4% en volumen, destacando las naranjas y pequeños cítricos, que concentran casi el 90% de la producción y el valor de este grupo. Los frutales no cítricos supusieron el 10,5% de la producción hortofrutícola. Como ejemplo para mostrar y entender la situación del sector productor hortofrutícola, por ser el que mejor conozco pongo el citrícola:

SITUACIÓN DEL SECTOR HORTOFRUTÍCOLA EN ESPAÑA, SOLUCIONES

Con una facturación de 3.000 millones de €, de los cuales el 80% es exportación. Esta producción es comercializada por 480 operadores de los que 150 son cooperativas, generando más de 70.000 empleos. El valor añadido generado en una campaña en transporte es del orden de 220.000 envíos por camión, más barco y tren, además del transporte interno o de almacén. Se utilizan 600 millones de cajas por campaña, elaboradas por 60 pequeñas empresas dispersas por todo el ámbito rural que emplean más de 3.000 personas. Se estima que los viveros dan trabajo a más de 2.000 personas. La industria de transformación: 31 empresas que emplean a 700 personas dando valor a la fruta que no tiene aptitud para comercializar en fresco. El valor del zumo exportado es de 158 millones de €. Hay 4 industrias de transformación de mandarinas que ocupa a 2.400 personas y factura 40 millones de €. Las industrias químicas, las fábricas de maquinaria, tractores, herramientas y toda la investigación en I+D con su industria para los almacenes de confección. Todo esto está en juego y subsiste gracias a una fruta llamada naranja y clementina de la que el agricultor año tras año pierde dinero al producirla, y que va a decir “BASTA”.

Este ejemplo no es huérfano, sino que sirve para todas las frutas, hortalizas y multiplica su repercusión del valor añadido en la producción

políticos respecto de la defensa de una política agrícola nacional y europea, especialmente a la de las frutas y hortalizas, por su capacidad de generación de empleo, riqueza y valor añadido, que por sí solo, con el 10% del suelo agrícola, factura el 62% del valor de la producción total agraria y da empleo al 60% del empleo de la rama agrícola. Las causas de esta situación son varias: la liberalización de las importaciones, una tendencia de consumo poco propicia, en algún momento agravada por las condiciones climáticas pero sobre todo por la crisis de consumo generalizada, la situación delicada de la industria

ayudas a la transformación, que ha atacado directamente a socios y cooperativas, ocasionando problemas de liquidez, inseguridad en la exportación o riesgo de insolvencia de clientes; las condiciones climáticas, que en unos casos han frenado el consumo y en otros han hecho que se solapen los periodos de comercialización de las distintas variedades. Pero hay dos factores que hay que destacar por encima de los anteriores: el desequilibrio de poder de la cadena alimentaria y la falta de un sistema público de regulación de mercado. El mayor de los problemas del sector agrario es el desequilibrio de poder en la cadena agroalimentaria. Los productores, mayoritariamente atomizados, se enfrentan a una distribución cada vez más concentrada.

Parlamento Europeo, varios EEMM, en referencia a varios sectores. En

en el sector FH, donde ya están implantadas las OP, sigue habiendo desequilibrio. No hay más que ver el sistema de pago de la fruta al agricultor. Las OP agrupan a menos del 50% del sector y, además, las OP son muy pequeñas: tenemos más de 600 en España, con una facturación media de menos de 10M€; una cooperativa “muy grande”, en términos relativos, factura 400M€. En el otro lado de la balanza, la empresa de distribución alimentaria que más factura sobrepasa los 10.000M€ y los 5 más grandes de la distribución alimentaria, concentran más del 60%...

PRESIDENTE SEC. FRUTAS Y HORTALIZAS DE COOPERATIVAS AGROALIMENTARIAS

CIRILO ARNANDIS NÚÑEZ,

Fruit logística

Fruit logística ’12 9

Personalidades / Personalities

Fruit logística ’1210

EsY LA CONVENIENCIA DE LO SALUDABLE

The pleasure, the experience, and the convenience of what’s healthy

José Mª Bonmatí, Director General at AECOC, one of the biggest enterprise association in Spain and the only one in which manufacturers and distributors work alongside to improve the sector, aiming at providing higher value to consumers.

A new year just started and, as usual, it’s time to make a review, but above all to define the best strategies to face this new year. Nobody is alien to the fact that the complex economic situation, which first affected the most expendable goods and services, already hit the sector of agriculture and food, and in a market with “new game rules” the old tactics won’t do. Therefore it is essential to be now closer to consumers than ever, for despite being very struck by the crisis won’t give up quality or pleasure.These are then two important drivers of consump-tion and two factors that the sector of fruits and veg-etables should take advance of. Regarding the first one, the sector has an important advantage for no other product can be proud of being an example of healthy product, matching the lifestyle that more and more consumers want to adopt. Nevertheless, regard-ing pleasure, the sector still has a long path to walk. For that reason, it is important that enterprises –indus-try and distributors- dared to innovate, and to do it in the broadest sense of the word, that is, in product, packaging, assortment, information/communication to consumers, purchasing experience, creation of new consumption moments, etc. Always getting a competi-tive advantage from innovation.Also pursuing that global aim of improving competi-tiveness, enterprises in the sector must be able to study the opportunities that other markets give them, economies that are less damaged by the crisis and that may be a good option in a complex moment for the domestic market. All this, not forgetting the sig-nificant opportunities for improvement that the value chain offers, which must be now more than ever re-garded as a unity without cleavage or inefficiency. Aiming at that goal, the business standards promoted and developed in Spain by AECOC in fields like prod-uct identification or e-commerce –EDI, e-invoice…- or efficient practices in logistics and transport, commer-cialisation, demand, etc. are always a good ally, but particularly in a moment like this, when the capacity to save resources is a rising value.New consumers, future consumers will only commit to those who differentiated themselves from their com-petitors, who innovated, who provided more value, definitely: those who count for them. That and no other is the true challenge.

DIRECTOR GENERAL DE AECOC, UNA DE LAS MAYORES ASOCIACIONES EMPRESARIALES DE ESPAÑA Y LA ÚNICA EN QUE FABRICANTES Y DISTRIBUIDORES TRABAJAN CONJUNTAMENTE PARA LA MEJORA DEL SECTOR CON EL FIN DE APORTAR MAYOR VALOR AL CONSUMIDOR.

JOSÉ Mª BONMATÍ,

Fruit logística

Fruit logística ’12 11

Personalidades / Personalities

Fruit logística ’1212

Y PAGOS JUSTOS

Fair prices, fair margins, fair payments

Francisco Sanchez Pro, manager at Onubafruit, Europe’s biggest marketer of berries with a turnover close to € 130 million.

Analysing the situation that the sector of fruits and veg-etables is experiencing we must take into account sev-eral factors that helped us to understand why prices fall unstoppably.Maybe the most highlighted is the much mentioned crisis we are living, that is resulting in excessive purchase reces-sion due to fear of a new relapse, which makes consum-ers be ultraconservative. This is but a mistake for if we don’t consume, we will feed more and more the fall of prices, we will increase the enterprise crisis and ours too definitely.On the other hand, big distribution is fighting its own battle, which looks more like a war for its stupidity, as their aims are not clear. They fight to see who will market the cheap-est product, the most submissive, the one which losses more, the one with lowest quality. The most used sentence is “I less…”, as if being less nowadays was some kind of value added. Faced with it, distribution chains with clear aims, which are very few truth be told, are growing much more than the rest, offering enough profitability and, which is more important, helping their suppliers to get out of the crisis. Examples are Ahorramás in Spain, COOP in Switzer-land, LIDL in Germany, and in general the English chains,

stood out for their own business strategies, and there are they: they grow and their suppliers are happy. I would rec-ommend for big distribution to bank on acknowledge and appreciate the quality of our fruits and vegetables.The media are playing a fundamental role in this price crisis, besides organisations and growers in general. We blame distribution for everything. Today it’s abusive prices that result in consumption drop; tomorrow it will be pretty low prices resulting in profit loss. Let’s clear up our mind and stop looking at our own belly. We can’t compare prices at origin and at destination without a comparative basis, driving distribution to lower the already risible prices and to ruin ourselves a bit more. Comparisons should be made with the same product quality, size, manufacturing, transport, etc. for easy comparisons using extreme value and without a basis only harm us and lower prices even further. As I said before, the responsibility for low prices is a matter of everyone and it is pointless to blame distribution for low prices today, high prices tomorrow, and whatever the day after. Let’s ask for fair prices, fair margins, the ob-servance of the Trade Laws and that’s it. The rest will come on its own.

All this situation of low prices makes growers consider, too frequently, their expenses, which have a direct impact on quality. If I don’t get paid I don’t produce well, but we must be aware that if I don’t produce well I will get paid less and back to the beginning.Despite everything, producers must place on supermar-ket shelves quality products that could be massively consumed, no matter the price. This is our only and most important weapon. Holding the banner of quality will be able to have credibility and reasons for effective protests, we will fight a battle of equals. And without quality we do nothing but increasing our own ruin.I don’t want to forget the lack of union that there is amongst producer, unlike what happens in distribution, which up-sets the balance. If we don’t unite, they will sweep us. But it seems that the feeling of independence lasts to ruin and poverty. Few effective unions succeed and even fewer are known. Disunity is trendier.But that is just another mistake, and one of the biggest. If we don’t know how to collaborate with our peers, we will only end deeper and deeper into barren lands.Onubafruit is union, and this is not a mistake.

GERENTE DE ONUBAFRUIT, LA MAYOR COMERCIALIZADORA DE BERRIES DE EUROPA, CON UN VOLUMEN DE NEGOCIO CERCANO A LOS 130 MILLONES DE €.

FRANCISCO SANCHEZ PRO,

Fruit logística

Fruit logística ’12 13

Onubafruit’s efforts on promotion help to reach € 130 million worth turnover

Onubafruit, the Huelva-based enterprise that is Europe’s main exporter of berries, which gathers the cooperatives Cobella, Cartayfres, CoopHuelva, Freslucena, Bonafru and SAT Condado, ended 2011 with an increase of € 29 million in invoicing over the previous campaign, going from 101 to 130 million

In this line, Onubafruit’s CEO, Antonio Tirado, explains that the company will keep working to “make headway for the joint commercialisation of up to one third of Huelva’s production, with supply able to satisfy the needs of national and international big distribution as for quality, customer service, price, and production technology, keys to guarantee direct interaction and progressive increase of negotiation capacity with Europe’s big chains, obviating the intervention of commercial agents, an effort that allowed for saving € 5.5 million in commissions since 2003.”In this sense, Tirado highlights that “these figures reinforce the position of our company in European markets, and also strengthen the upward trend that the company has followed since its beginning in 2004, despite the economic crisis”. On these figures, Onubafruit’s CEO stresses that success is based on “the quality of the circa 75,000 tonnes of fruit we handled in the last campaigns, as well as on the joint work of the cooperatives and Onubafruit.”But the work of this Huelva enterprise doesn’t only reflect on figures, as they made a strong effort to improve their internal and external communication channels in the

last campaign, at the same time they kept on making progress on diffusion and promotion of their products. An example of it is the modernisation of their corporate image, the edition of a professional bulletin, and their attendance to the most relevant trade fairs and forums in the sector of agriculture at the national and international level.

Promotion effortsFramed in their strategy of actions to keep boosting international commercialisation, amongst other events, Onubafruit attended Fruit Attraction with its own stand in 2011, carrying out diverse promotion actions such as the sponsoring of the I Conecta Awards to Distribution, organised by Mercados magazine and the agency Circus. With this initiative, the Huelva company contributes to foster the approach of producers and marketers to big distribution as the only mechanism to achieve managerial growth in the sector of fruits and vegetables, so that Onubafruit takes another leap for the sake of commercialisation in Huelva.

El

ONUBAFRUIT, LA EMPRESA ONUBENSE LÍDER EN EXPORTACIÓN DE BERRIES EN EUROPA Y QUE ESTÁ INTEGRADA POR LAS COOPERATIVAS COBELLA, CARTAYFRES, COOPHUELVA, FRESLUCENA, BONAFRU Y SAT CONDADO, FINALIZÓ EL PASADO AÑO CON UN

INCREMENTO DE 29 MILLONES DE EUROS EN LA FACTURACIÓN CON RESPECTO A LA TEMPORADA ANTERIOR, PASANDO DE LOS 101 MILLONES DE 2010 A 130 MILLONES EN 2011.

EL ESFUERZO DE PROMOCIÓN DE ONUBAFRUIT AYUDA A ALCANZAR 130 MILLONES DE EUROS

DE FACTURACIÓN

ESFUERZO DE PROMOCIÓN

Personalidades / Personalities

Fruit logística ’1214

ENCARANDO EL FUTURO DESDE EL CUARTO AÑO DE CRISIS

DIRECTOR – DEPARTAMENTO DE EMPRESAS ALIMENTARIAS. INSTITUTO INTERNACIONAL SAN TELMO

PROF. JOSÉ ANTONIO BOCCHERINI BOGERT,

Food chain: facing the future from the fourth year of crisis

Prof. José Antonio Boccherini Bogert, Director – Department of Food Enterprises. San Telmo International Institute.

After three years of crisis, the food chain will face 2012 with good and bad news. Good news is that we all still need to eat and food will be one of the least affected sectors. Bad news is that adjustment measures imposed by the sovereign-debt crisis will keep restraining consumption.The crisis is prompting structural changes that will persist once the storm was over. To deal with the short run, good financial health will be necessary, and having done our homework too. In order to tackle the future, one must understand the structural nature of changes and develop new capacities.Regarding structural factors, consumers will keep buying cheap, as they already gave economical products a try (private brand, for instance), and saw they have good quality. They won’t pay more for products that don’t give differential value. Quality is essential, but not enough.Efficiency and low cost (without compromising quality) will be essential. We must keep optimising the processes and looking for economies of scale, increasing the business dimension. We will see concentration operations (mergers, alliances, etc.) at all levels. It will also be necessary to globalise operations, acquiring global efficiencies as for procurement and production, in order to contend on equal terms with competitors from emerging countries.Launching new products will still have sense, but they must provide differential, tangible value: it will be difficult to make consumers pay for unnecessary

differences. Besides, it will be difficult to find room on shelves so that the new products will have to contribute value to the channel, helping it to overcome its profitability issues. And, to a channel, value means margin, rotation, and logistics efficiency.The developed markets (Europe and North America above all) will show little growth. Consumption will fall in emerging countries, so that internationalisation will be the main priority for the companies that wanted to grow.Consumers are becoming digital and they feel more and more comfortable on the internet. They are overcoming their reticence (to great extent involving payment safety). They will use the internet to get informed about products (trusting more a friend from a social network than advertising campaigns), to compare prices (those who don’t adapt their prices won’t survive), and to look for convenience and comfort (they don’t want to lose their time going shopping). They will have more power and brands will have to learn to relate with them within the digital ecosystem, and to have influence on their purchase decisions. Few know how to do it nowadays.Growing in international markets, being very efficient, gaining dimension, providing real value, and embarking on digital transformation. These are the priorities. A world full with opportunities for companies that knew how to develop the necessary capacities.

Entidades / Organizations

Fruit logística ’1216

El

¿QUÉ SE APORTA AL SECTOR AGROALIMENTARIO?

What do business school contribute to the sector of agro-food?

By Javier María de Domingo Morales, EOI Escuela de Organización Industrial, in charge of the Programmes of Agro-food Business Management for FAECA www.eoi.es

The sector of agro-food, mainly identified with producers, agro-food industries and distributors, is undoubtedly starred by these. Other players and entities that also work for and in the sector are: auxiliary industries, technology centres, business associations…Business Schools also play a significant role, like EOI Escuela de Organización Industrial does, whose mission includes training and keeping executives up to date with necessary knowledge and skills in the current context.

In the last years, EOI has been strengthening an interesting project destined to professionals in the sector of agro-food. What would you highlight of it? Undoubtedly, the tailored programmes of business management that we have been developing since longer than 8 years ago for executives and managers of the cooperatives member to FAECA (Andalusian Federation of Agricultural Cooperative Enterprises), or for federations of agro-food cooperatives in Castile – La Mancha, the Basque Country, and Aragon. Next February, in collaboration with the CAAE Association, we will start the second programme of Organic Enterprise Management; in March, the fifth edition of the Programmes of Agro-food Business Management for enterprises member to FAECA will be set in motion.At present, we also bank on open training, that is, programmes of agro-food business management with participation of various enterprises and organisations that are interested in staying up to date. We are to start the second edition of the High Training Course on Agro-food Business Management next February in Seville; it is a 120-hour, open programme course.We couldn’t forget that we have been training executive and middle-rank officers of enterprises in the sector since

1955 thanks to our master courses and programmes. A new edition of the MBA Executive will start next February at our offices in Seville and Madrid.

What “does one learn” in the programmes of agro-food executive development at EOI? One thinks about and learns how to better manage. We help participants to face the challenges of the sector; mainly to achieve enterprise survival in the long run, to learn doing, to be efficient as for production, to orient their decisions to the market, to develop brand value and differentiation, to search for a greater dimension, to achieve internationalisation, to be competitive, and to generate value in their local and global spheres.

What else would you highlight regarding EOI’s training programmes? They are professional-to-professional training. Likewise trainees, teachers in our training programmes are professional in the agro-food sector. They are high rank officers that devote part of their time to teach, sharing their day-after-day experiences and focusing on joint reflection with trainees.

Tell a reason to “abandon our daily routine” and devote part of our time to training. One doesn’t need to abandon their daily routine; our programmes for professionals are compatibles with their calendars. More so, we aim at their daily routine to be part of the debate within the classroom. Undoubtedly, taking part in training programmes is but an opportunity to enter a forum in which to debate on solutions to the possible difficulties of our business, and to discover new opportunities above all. For instance, social networks as a tool to strengthen brands and business strategies and as a powerful communication channel.

DIRECTOR DEL ÁREA DE EMPRESAS Y ADMINISTRACIÓN PÚBLICA DE EOI ESCUELA DE ORGANIZACIÓN INDUSTRIAL.

JAVIER DE DOMINGO MORALES,

Fruit logística

Fruit logística ’12 17

ADESVA, CENTRO TECNOLÓGICO DE LA AGROINDUSTRIA

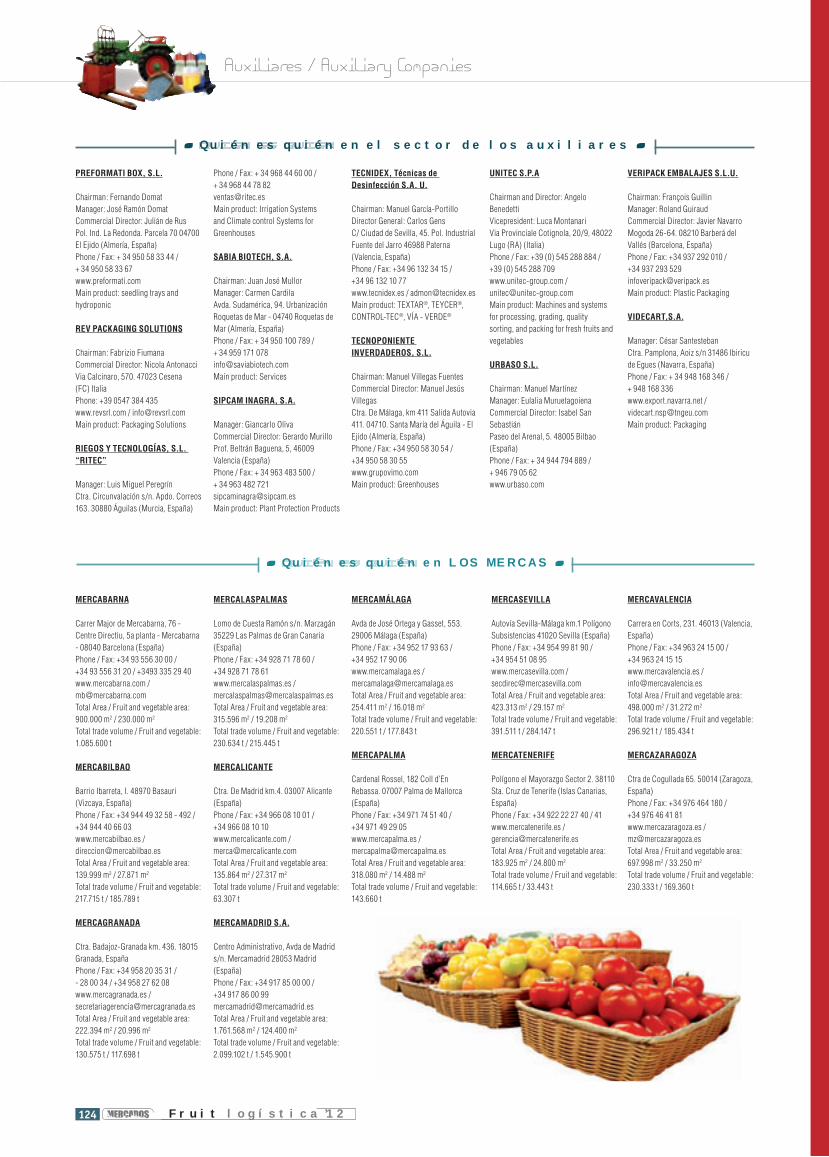

Chairman: Esteban SánchezManager: Aurelio Gómez Commercial Director: José BourreParque Empresarial La Gravera 1. Apdo. 394. 21440 Lepe (Huelva, España)Phone / Fax: +34 959 64 90 62 / +34 959 64 90 61www.citadesva.comMain product: R & D projects

AFRUCAT

Chairman: Francesc Argilés FelipManager: Manel Simón i BarberoAvd. Tortosa 1. 25001 Lleida (España)Phone / Fax: +34 973 22 01 49 / +34 973 22 04 37www.afrucat.comMain product: Stone fruit & Pomes

AFRUEX. ASOCIACIÓN DE FRUTICULTORES DE EXTREMADURA

Chairman: Antonio Chavero Manager: Miguel Ángel Gómez-Carsoso Cánovas del Castillo, s/n. 06800 Mérida (Badajoz, España)Phone: +34 924 30 42 00 www.afruex.comMain product: Summer fruit

AILIMPO

Chairman: Rafael Sánchez Manager: José Antonio García C/ Villaleal, 3 bajo. 30001 Murcia (España)Phone: +34 968 21 66 19 www.ailimpo.com [email protected] product: Lemon and grapefruit

ANAPE (Asociación Nacional de Poliestireno Expandido)

Chairman: José María FontManager: Raquel López de la BandaPº de la Castellana, 203. 1º Izq. 28046 Madrid (España)Phone / Fax: +34 913140807 / +34 913 78 80 01www.anape.es / [email protected] product: Applications of expanded polystyrene

APOEXPA (A. Productores y Exportadores Fruta de Hueso, Uva de Mesa y otros productos agrícolas)

Chairman: Joaquín GómezC/ San Martín de Porres, nº 3, 1ª. 30001 Murcia (España)Phone / Fax: +34 968 20 49 49/ +34 968 20 48 77www.apoexpa.esMain product: Stone fruit and grape table

AREFLH

Manager: Jacques Dasque37 Avenue du Géneral de Larminat. Inmeuble Point Centre 33000 Bordeaux. FrancePhone / Fax: +33 (0) 556 48 88 48 / +33 (0) 556 48 88 40www.arefl h.orgMain product: Fruits and vegetables

ASOC. PRODUCTORES COMERCIALIZADORES GRANADAS DE ELCHE

Chairman: Andrés Irles IbarraPorta Oriola 6 bajo 03203 Elche (Alicante, España)Phone / Fax: +34 902 36 57 35 / +34 966 61 35 63www.granadasdeelche.org /[email protected] product: Pomegranates Mollar

ASOC. PROMOCIÓN DE LA PERA DE RINCÓN DE SOTO

Chairman: Eduardo Pérez MaloAvda. Príncipe Felipe, 7, bajo. 26550 Rincón de Soto (La Rioja - España)Phone / Fax: +34 941 14 19 54 / +34 941 14 19 [email protected] / [email protected] Main product: Pear (Blanquilla y Conferencia)

ASOC. CITRIC. PROV. DE HUELVA

Ctra. N.431,km.111 apdo.96. 21450 HuelvaPhone / Fax: 43 959 39 07 52 / 34 959 39 22 [email protected] product: Citrus

ASOCIACIÓN CAAE

Chairman: Francisco CaseroManager: José Luís García MelgarejoCommercial Director: Arantxa EslavaAvda Emilio Lemos,2. Edif Torre Este, Mod. 603. 41020 Sevilla (España)Phone / Fax: + 34 902 521 555/ + 34 955 029 491www.caae.es / [email protected] / [email protected] product: Ecological agriculture services

Asociación de Empresarios Mayoristas del Mercado Central de Frutas de Madrid ASOMAFRUT

Manager: Luis Alberto CarriónMercamadrid, Carretera Villaverde a Vallecas km 3,8. Nave J-2 Entrada Norte. 28053 Madrid (España)Phone: +34 917 85 32 11 www.asomafrut.comMain product: Fruit and vegetables

ASOCIACIÓN DE PRODUCTORES Y COMERCIALIZADORES DE ANDALUCÍA (A.P.R.O.C.O.A.)

Chairman: Miguel del Pino NietoAncha 21. 14548 Montalbán de Córdoba (Córdoba, España)Phone: +34 607 55 55 82 [email protected] product: Garlic

ASOCIACIÓN ESPAÑOLA DE COSECHEROS EXPORTADORES DE CEBOLLA (ACEC)

Chairman: Alfonso TarazonaC/ Hernán Cortés, 4 46004 Valencia (España)Phone / Fax: +34 963 51 74 09www.acec.info / [email protected] product: Onion

ASOCIACIÓN PARA LA PROMOCIÓN DEL MELÓN DE LA MANCHA

Chairman: Ramón Lara SánchezC/ Pedro Domecq, 2. 13700 Tomelloso (Ciudad Real, España)Phone: +34 926 53 82 16 [email protected] product: Melon from La Mancha

ASOCIACIÓN PINK LADY EUROPA

Chairman: Didier CrabosManager: Thierry MellenotteTrade Marketing Director: Jean-Louis Colombat436, Avenue Charles de Gaulle. 84100 Orange (Francia)Phone / Fax: +33 490 119180 / +33 432 81 13 [email protected] product: Pink Lady Apples

ASOCIACIÓN PROFESIONAL CITRÍCOLA PALMANARANJA

Chairman: Teodoro RevillaManager: Mª Fuensanta ÁlvarezAvda. Félix Rodríguez de la Fuente s/n. 14700 Palma del Río (Córdoba, España)Phone / Fax: +34 957 64 40 34 / +34 957 64 40 34www.palmanaranja,com / [email protected] product: Citrus

ASOCIAFRUIT

Chairman: Enrique Pérez SaturninoManager: Luís Marín LampareroAvda de Málaga, 16, 1ºC. 41004 Sevilla (España)Phone / Fax: +34 954 42 42 98 / +34 954 41 00 60www.asociafruit.com / [email protected] product: Summer fruit, citrus, potato, carrot, etc.

ASPROCAN

Chairman: Francisco RodríguezManager: Esther Domínguez PalareaAvda. José Manuel Guimerá, nº3. Edif. Urbis, 5º piso. Ofi cina C.D. 38003 Santa Cruz de Tenerife (Islas Canarias, España)Phone / Fax: +34 922 53 51 42 / +34 922 53 51 [email protected] product: Plátano

AUTORIDAD PORTUARIA DE CARTAGENA

Chairman: Adrián Ángel ViudesManager: José Pedro VindelCommercial Director: Fernando MuñozPlaza Héroes de Cavite s/n. 30201 Cartagena (Murcia, España)Phone / Fax: +34 968 325 800 / +34 968 325 815www.apc.es / [email protected] product: Services

C. R. .I. G. P. PATATA DE GALICIA

Chairman: Julio Gómez FernándezManager: Ricardo Losada BlancoFinca Devesa s/n. 32630 Xinzo De Limia (Ourense, España)Phone / Fax: +34 988 46 26 50www.patacadegalicia.es / [email protected] product: Potato PGI Regulatory Board. Kennebec variety

C. R. I. G. P. DEL MELÓN DE TORRE PACHECO

Avda. Luis Manzanares, s/n (Ed. Vivero de Empresas) 30700 Torre Pacheco (Murcia, España)Phone / Fax: +34 968 576 [email protected] product: Melon

Quién es quién en ENTIDADES

Entidades / Organizations

Fruit logística ’1218

C. R. I.G.P. ESPÁRRAGO DE NAVARRA

Chairman: Martín Barbarin LogroñoManager: Ana Juanena LazcanoAvda. Serapio Huici, 22 31610 Villava (Navarra, España)Phone / Fax: +34 948 01 3 045 www.denominacionesnavarra.com / [email protected] product: White Asparagus

C.R. I. G. P. CEREZAS DE LA MONTAÑA DE ALICANTE

Chairman: Elvira Sánchez MengualCtra. Albaida-Denia, s/n. 03788 Alpatró. La Vall de Gallinera

Quién es quién en ENTIDADES

(Alicante, España)Phone / Fax: +34 966 40 66 40 / +34 966 40 66 11www.cerezas.orgMain product: Cherry

C. R. I.G.P. TOMATE LA CAÑADA NÍJAR

Chairman: Francisco LópezCertification Director: Cristóbal José Múñoz FernándezCtra de Ronda nº 11 Bajo. 04004 Almería (España)Phone / Fax: +34 950 28 03 80 / [email protected] product: Tomato La Cañada Níjar

C.R.D.E. ESPÁRRAGO DE HUÉTOR TÁJAR

Chairman: Antonio Fco Zamora Manager: Encarnación Campaña Commercial Director: Antonio Sanjuan PinillaCtra. De la Estación s/n. 18360 Huétor-Tájar (Granada, España)Phone / Fax: +34 958 33 34 43 / +34 958 33 25 22www.esparragodehuetortajar.com / [email protected] product: Huetor Tájar green-purple asparagus. Fresh and canned

C. R. D.O. CEREZA DEL JERTE

Chairman: José Fernández GarcíaManager: Pilar Díaz FloresCtra. N110 Km 381. 10613 Navaconcejo (Cáceres, España)Phone / Fax: +34 927 47 11 01 / +34 927 47 10 67www.cerezadeljerte.org / Main product: Picota del Jerte Cherry

C. R. D.O. KAKI RIBERA DEL XUQUER

Chairman: Cirilo ArnandisManager: Rafael PeruchoPlaza Pais Valencia, 7 46250 L Alcudia (Valencia, España)

Phone / Fax: +34 962 99 77 [email protected] / www.kakifruit.comMain product: Kaki Persimon

C.R.D.O. MANZANA REINETA DEL BIERZO

Chairman: Ángel Garnelo AbramoManager: Pablo Linares BarrealCtra. N.VI, km 398. 24549 Carrecedelo (León, España)Phone / Fax: +34 987 56 28 66 / +34 987 56 28 69www.manzanareinetadelbierzo.es Main product: Reineta del Bierzo Apple

AMENAZA, DESAFÍOS Y OPORTUNIDADES

Queriendo olvidar el 2011, que sin duda ha sido el año más complicado que conozco en la historia del sector de frutas y verduras frescas, y dejando a un lado la volatilidad de

mensaje de ánimo a productores, exportadores y comercializadores en general de nuestro sector.Sin duda, estamos preparados para lo que venga en este 2012, aunque sea lo peor, pero debemos pensar que debe ser el punto de

una manera más o menos incierta, nos ha estado azotando en los últimos cuatro años. Unas empresas habrán desaparecido y otras se habrán visto fortalecidas por una mayor

teniendo productos novedosos y diferentes.

la calidad y, por tanto, la competitividad.En la industria de frutas y verduras

encontremos, debemos buscar un camino

PRESIDENTE DE FRESHFEL. ASOCIACIÓN EUROPEA DE FRUTAS Y HORTALIZAS FRESCAS, QUE INCORPORA A MÁS DE 200 MIEMBROS DE TODA LA CADENA DEL SECTOR DE FRUTAS Y HORTALIZAS CON INTERÉS EN EL MERCADO EUROPEO.

RAMÓN REY,

Threats, challenges, opportunities

By Ramón Rey, president at Freshfel. European Association of Fresh Fruits and Vegetables, which gathers 200 plus players of the whole chain in the sector of fruits and vegetables, with interests in the European market.

Wanting to forget 2011, which has undoubtedly been the most complex year I’ve ever seen in the history of the sector of fresh fruits and vegetables, and leaving aside the volatility of financial markets, I would like to send a message of courage to producers, exporters, and marketer in general in our sector.Undoubtedly, we are ready for what is to come in 2012, even for the worst, but we should think that it must be the turning point of this severe instability that has whipped us during the last four years, one way or another. Some enterprises disappeared;

others grew stronger thanks to further specialisation, diversification, or thanks to novel and different products. Anyway, the edge will be efficiency, quality, and therefore competitiveness.In the sector of fresh fruits and vegetables, no matter the link of the chain, we must look for a shared path to increase consumption.We enjoy a reputation of healthy product but we don’t manage to sell or communicate it adequately and widespread to the public, and this should be the main aim for the sector in this year of shortage. In order

to sell more, consumers must appreciate our products and repeat their purchases, and we need to coordinate to convince them, not only from producers to retailers but from breeders, irrigation suppliers, producers of fertilisers, cardboard manufacturers, hauliers, and the rest of professionals that orbit around our sector.All this is synthesised and balanced on the platform www.enjoyfresh.eu, to which I send my greetings, support, and encouragement from these lines, and which I foster you to support and join. It is our challenge and our opportunity. All together.

conjunto para incrementar el consumo de las frutas y verduras en fresco. Gozamos de una imagen saludable como producto, sin embargo, no sabemos venderlo o comunicarlo de una manera adecuada y en

vender más, el consumidor debe apreciar más nuestros productos y realizar una compra repetitiva, y para ello le debemos convencer de una manera coordinada, no solamente desde

empezando desde las compañías de semillas de suministros para riegos o fertilizantes, cartoneras, transportistas y todo el resto de sectores que giran alrededor del nuestro. Todo esto está sintetizado y conjugado en la plataforma www.enjoyfresh.eu, a la cual saludo desde estas líneas, apoyo y aliento, y a la que les animo a apoyar e incorporarse. Es nuestro desafío y nuestra oportunidad. Todos juntos.

Fruit logística

Fruit logística ’12 19

C.R.D.O. MELOCOTÓN DE CALANDA

Chairman: Samuel Sancho VillarroyaManager: Ana Omedes JordánC/ Muro Sta María s/n.Edif. Mayor. 1ª planta. 44600 Alcañiz (Teruel, España)Phone / Fax: +34 978 83 56 93 / +34 978 83 43 [email protected] product: Peach from Calanda

C.R.D.O. UVA MESA EMBOLSADA VINALOPO

Chairman: José Bernabeu Manager: Luis González Virgen del Remedio, nº33. 03660 Novelda (Alicante, España)Phone / Fax: +34 965 60 48 59 / +34 965 60 48 [email protected] product: Grape

CEBACAT

Chairman: Ramón JounouManager: Josep BoqueAvinguda Lleida, 81, 25250 Bellpuig Lleida SpainPhone / Fax: +34 973 337 281 / +34 973 602 209www.cebacat.com / [email protected] product: Onions

COEXPHAL

Chairman: Manuel GaldeanoManager: Juan Colomina FigueredoCtra. Ronda nº11. 1º. 04004 Almería (España)Phone / Fax: +34 950 62 11 62www.coexphal.es / [email protected] product: Fruits and vegetables

COMITÉ DE GESTIÓN DE CÍTRICOS

Chairman: Antonio Muñoz - Vicente BordilsManager: Francisco José MartínezMonjas de Santa Catalina, 8 4º. 46002 Valencia (España)Phone / Fax: +34 963 52 11 02 / +34 963 51 07 [email protected] product: Citrus

D.O.P. COSTA TROPICAL GRANADA-MÁLAGA

Chairman: Antonio Osuna Carillo de AlbornozManager: Coordinadora: Pilar Fajardo AneasAvda Juan Carlos I. Edif Estación s/n. Apdo 648. Almuñécar (Granada, España)Phone / Fax: +34 958 63 58 65 / +34 958 63 92 01www.crchirimoya.org / [email protected] product: Custard apple - cherimoya with qualit certifi cation protected designation of origin

D.O.P. PERA DE JUMILLA

Chairman: Diego GarcíaManager: José FerrándizC/ Almería, 1 bajo. 30520 Jumilla (Murcia, España)Phone / Fax: +34 968 716 [email protected] product: Pear

ECOHAL GRANADA (Asociación Empresarios Comercializadores Hortofrutícolas de Granada)

Chairman: José Muñoz Manager: Alfonso Zamora Marqués de Vistabella 16-2º D. 18600 Motril (Granada, España)Phone / Fax: +34 958 83 41 93 / +34 958 83 41 [email protected]

EXCOFRUT. Asoc. Profesional de Frutas y Hortalizas de Huesca

Chairman: José Antonio Coll BeanC/ Huesca, 66. Altillo 22520 Fraga (Huesca, España)Phone / Fax: +34 974 47 17 00 / +34 974 45 38 64www.excofrut.com / [email protected] product: Peach, nectarine, paraguaya, pear, apple, apricot, cherry, plum, fi g

FRESHUELVA

Chairman: Alberto GarrochoManager: Rafael Domínguez GuillénC/ Manuel Sánchez Rodríguez 1 Apdo. Correos. 140 21001 Huelva (España)Phone / Fax: +34 959 24 82 22 / +34 959 25 83 73www.freshuelva.es / [email protected] product: Berries

HORTYFRUTA. Interprofesional de Frutas y Hortalizas de Andalucía

Chairman: Fulgencio TorresManager: María José PardoAvda. Montserrat 16, 5º 04006 Almería (España)Phone / Fax: +34 950 26 9161www.hortyfruta.es / [email protected] product: Fruits and vegetables

I.G.P. AJO MORADO DE LAS PEDROÑERAS

Chairman: José Suárez OsaManager: Juan Martínez BravoPlaza Arrabal del Coso s/n. 16660 Las Pedroñeras (Cuenca, España)Phone / Fax: +34 967 139 333 / +34 967 139 334www.igpajomorado.es / [email protected] product: Purple garlic

I.G.P. CÍTRICOS VALENCIANOS

Chairman: José BarrésManager: Juan Bta. Juan GimenoC/ Guillem de Castro, 51. 46007 Valencia (España)Phone / Fax: +34 963 15 40 52 / +34 963 15 51 [email protected] product: Citrus Fruits (orange, tangerine and lemon), Certifi cation of Citrus

I.G.P. PATATES DE PRADES

Chairman: Antonio Anselmo PonsManager: Inma Sahún JovéAvda. Verge de L’Abellera,1. 43364 Prades (Tarragona, España)Phone / Fax: +34 977 86 84 40 / +34 977 86 81 [email protected] product: Potato de Prades

I.G.P. POMA DE GIRONA

Chairman: Venanci GrauMas Badia 17134 La Tallada d´Empordá (Girona, España)Phone / Fax: +34 972 78 08 16 / +34 972 78 05 17www.pomadegirona.cat / [email protected] product: Apple (Golden, Royal Gala, Granny Smith and Red Delicious)

INTERCITRUS. Interprofesional Cítricola Española

Chairman: Felipe JuanCalle de la Paz, 14p-7. 46003 Valencia (España)Phone / Fax: +34 963 94 22 20 / +34 963 52 47 [email protected] product: Citrus

MARCA DE GARANTIA PERA CONFERENCIA DEL BIERZO

Chairman: Mª Eugenia Alba PotesManager: Pablo Linares BarrealCtra. N-VI km.398. 24549 Carracedelo (León, España)Phone / Fax: +34 987 56 27 13 / +34 987 56 28 69www.peraconferenciadelbierzo.es / [email protected] product: Conferencia del Bierzo Pear

PROEXPORT (Asociación de Productores - Exportadores de Frutas y Hortalizas de la Región de Murcia)

Chairman: Juan Marín BravoManager: Fernando P. Gómez MolinaRonda Levante, 1 - Entlo. 30008 Murcia (España)Phone / Fax: +34 968 27 17 79 / +34 968 20 00 [email protected] product: Fruits and vegetables

RED ANDALUZA DE SEMILLAS CULTIVANDO BIODIVERSIDAD-RAS

Manager: Alonso Navarro ChavesCaracola del CIR, Parque de San Jerónimo s/n 41015 Sevilla (España)Phone / Fax: +34 954 40 64 [email protected] / www.redandaluzadesemillas.org

Quién es quién en ENTIDADES

Tomate / Tomato

Fruit logística ’1220

En

DESBANCA AL TOMATE ESPAÑOL EN EUROPA

> SE PIDE LA NO RATIFICACIÓN DEL NUEVO ACUERDO DE LA UE CON MARRUECOS. <

> LA CRISIS DEL E.COLI HA REDUCIDO EL VALOR ECONÓMICO DE LAS EXPORTACIONES ESPAÑOLAS DE TOMATE EN UN 27% EN 2011. <

Datos de FEPEX en toneladas.

Datos de la FAO.

Datos del MARM de tomate español hasta octubre.

Fruit logística

Fruit logística ’12 21

Morocco replaces Spanish tomato in Europe> Many claim not to ratify the new EU-Morocco agreement. <

> The E. coli crisis cut the worth of Spanish tomato exports by 27% in 2011. <

The sector of tomato in Spain has undergone a sig-nificant crisis in the last years, which shrank general production and triggered the disappearing of many enterprises in diverse producer areas. Thus, production hit 4,797,900 tonnes and farmland 63,800 hectares in 2009 whereas, according to the Ministry for the En-vironment and Rural and Marine Affairs, up to October 2011, production only reached 3,891,000 tonnes and farmland only 51,500 hectares. Both figures dropped by 20% in just two years.This decrease was mainly due to competition from Mo-roccan tomato after the passing of the Agricultural Pro-tocol within the Association Agreement signed between the EU and Morocco in 2010, which set an increase of the allowed quota at zero tariff, and that meant the entry with almost no control of Moroccan produce in Europe, not observing the allowed volume nor the minimum price. This violation of the agreement resulted in a situation of unfair competition against European producers of tomato, particularly affecting Spain, as our production dates coincide.An example of this violation is that 23,335 tonnes of Moroccan tomato entered the EU last October exceed-ing the fixed monthly quota -10,600 tonnes- by 120%; besides, 14,000 tonnes entered through Perpignan at lower prices than the agreed. So Morocco replaces Spanish tomato in what had been its traditional, main market: France. Thus, in November, Moroccan exports to Perpignan reached 27,589 tonnes, five times the 4,879 tonnes exported by Spain. This and other in-stances were denounced by the Spanish Government to the European Commission.

The Spanish sector finds them impossible to compete with this country, considering that Almeria tomatoes are sold for € 0.80 apiece, whereas Moroccan ones hardly reach € 0.40. Furthermore, salaries in Almeria are € 45 per day, and only € 0.60 per hour in Morocco.In this sense, Fepex warned that the Association Agreement between the EU and Morocco prompted the destruction of 12,500 jobs within the sector of tomato in the last year. Thus, every 1,000 tonnes of tomato that we stop ex-porting mean 50 jobs less in tomato producer areas, amongst which we find Andalusia, Murcia, the Canaries and the Valencian Community, regions with the highest unemployment rates in the EU according to Eurostat.

New agreement with MoroccoThe European Parliament is expected to ratify again the Agricultural Protocol within the EU-Morocco Association Agreement next February; the aim is getting deeper in the reciprocal free trade of agricultural produce, fresh and manufactured, and fisheries. Morocco offers imme-diate free trade for 45% of the Community agro-food exports, 61% in five years, and 70% in ten years’ time. Amongst the benefited products: fruits, vegetable, canned products, and dairy products.The EU in turn offers almost complete free trade to Mo-rocco for fresh and manufactured agricultural produce but for some sensitive produce like tomato, zucchini, cucumber, clementine, and strawberry. Reduced rights or tariffed quotas are set for these products.As for tomato, the quota has been raised by 50,000 tonnes; entry price still reduced.

The Spanish sector of tomato hopes the agreement will be rejected after the voting next February and demands the Moroccan tomato to meet the same requirements Eu-ropean producers are demanded.This strong competition and the liberalisation of imports from third countries to the EU have driven the enterprises in the sector of tomato, the most exported vegetable from Spain, to innovate, to diversify their supply as a way to keep growing, to optimise resources, to modernise pro-duction structures, and to advance in biological fight as well. They also claim for the need of adapting the en-terprises to the new varieties demanded by consumers, and for top quality to be a trademark of Spanish exports.

The E. coli crisis and the Spanish sector of tomatoThe E. coli scandal has had enormous consequences for the Spanish sector of tomato. To Fepex, this crisis resulted in damage due to production loss and also to non-commercialisation of produce, commercial damage because of the general price drop, and also harmed the product image and consumers’ trust. In the first months of 2011, exports registered a positive evolu-tion until the alarm was raised on 26th May. From that moment on, our sales abroad plummeted, not only cu-cumber but also tomato and all fruits and vegetables in general. In particular, and according to figures provided by Fepex, exports of tomato dropped by almost 17% from June to September 2011 compared to the same period of 2010, from 88,703 to 74,043 tonnes. Re-garding the economic worth of it, the fall reached 27%: € 95 million in 2010 against 69 million in the same dates in 2011.

Tomate / Tomato

Fruit logística ’1222

ha puesto en evidencia, por un lado, el mal funcionamiento de los servicios de la Comisión responsables de las alertas

agraria comunitaria de gestión de crisis de mercado.Por otro lado, el fuerte crecimiento de las importaciones procedentes de Marruecos de productos como fresa, calabacín o tomate han agudizado la crisis en 2011.

de Saint Charles, en Perpignan, Francia, cuadruplicó a la española en el mes de octubre y la quintuplicó en noviembre, lo que para FEPEX supone que Marruecos ha expulsado al tomate español del que ha sido su tradicional y principal mercado. El fuerte incremento de exportaciones se está produciendo, además, incumpliendo el Acuerdo con la UE. En octubre, Marruecos sobrepasó lo establecido en el Acuerdo un 120% y en noviembre un 37%. Ante esta situación, FEPEX ha pedido a los eurodiputados

, cuya votación esta prevista en el pleno del Parlamento

del sector, dadas las diferencias abismales existentes entre los salarios (0,60 € hora en Marruecos) y las condiciones de producción en España y Marruecos. Y las más perjudicadas serán las comunidades que concentran la mayor parte

las que tienen las tasas más altas de paro de la UE.

EL E.COLI Y LAS IMPORTACIONES DE MARRUECOS, FACTORES DETERMINANTES DE LA CRISIS DEL SECTOR HORTOFRUTÍCOLA

La crisis que hemos vivido en 2011 en el sector del tomate y, en general, en las frutas y hortalizas, se ha debido principalmente a dos factores: la epidemia de E.coli y las importaciones de Marruecos.

pepinos españoles eran la causa del brote de E.coli que sufrió Alemania. Desde ese momento la exportación cayó drásticamente afectando

en general a todas las frutas y hortalizas. Hasta mayo las exportaciones aumentaron de forma continua; en enero de 2011 el valor de

relación al mismo mes de 2010; en febrero un 1,7%, en marzo un 1%, en abril un 2,6%; en mayo un 6%. En junio la exportación cayó un 10%, en julio un 23,5% y en agosto un 6%. Para FEPEX, los daños causados por la crisis del E.coli han sido de tres tipos:producción y por no comercialización de productos; daños comerciales por el descenso de precios

los consumidores. La Comisión Europea aprobó dos medidas: compensaciones para la retirada de cinco productos y medidas de apoyo a la promoción, que no han compensado el daño provocado. Esta crisis

E. coli and imports from Morocco, determining factors for the crisis of fruits and vegetables

By Jorge Brotons, chair at FEPEX. Established in 1987, this entity is composed by 26 regional or provincial associations, which in turn gather 1,500 plus enterprises in the sector of agriculture and commerce.

The crisis we have experienced in 2011 in the sector of tomato, and in the whole sector of fresh produce in general was prompted mainly by two factors: the E. coli scandal and the imports from Morocco.Exports recorded a positive development in the first months of 2011. It changed later, on 26th May, when Spanish cucumbers were wrongly and unfairly pointed as the cause of the E. coli outbreak that happened in Germany. From that moment on, exports dropped dramatically, not being cucumbers the only affected but also tomatoes and all fruits and vegetables in general.Exports increased continuously until May; in January 2011, the worth of our sales to foreign markets was 19% higher than that of January 2010; in February 1.7%, 1% in March, 2.6% in April, in May 6%. In June, exports dropped by 10%, in July by 23.5%, and in August 6%.To FEPEX, the damage caused by the E. coli crisis has had three components: production loss and non-commercialisation of produce; commercial damage due to general fall of prices; damage to the product image and consumers’ trust. The European Commission passed two measures: payments for withdrawal of five products, and support for promotion; neither of them compensated the harm caused. This crisis took out into the open the improper functioning of the Commission’s services in charge of

sanitary alerts on one hand, and on the other, the ineffectiveness of the measures of the common agricultural policy for market crisis management.Besides, the significant rise of Moroccan imports of strawberry, zucchini, or tomato worsened the crisis in 2011. As for tomato, the Moroccan exports to the Saint Charles market in Perpignan (France) were four times the Spanish batch in October, five times in November; according to FEPEX, it means that Morocco has just expelled Spanish tomato from its traditional, main market. Furthermore, the great increase of exports doesn’t comply with the Agreement signed with the EU; in October, Morocco exceeded the quota established in the Agreement by 120%, in November by 37%.Faced with this situation, FEPEX asked the Spanish members of the EU Parliament to vote against the new agricultural protocol framed in the Association Agreement, which is expected to be voted in the European Parliament plenary session in February, for it would lead to job destruction, farms closure, and to the disappearing of the sector, given the profound differences between salaries (€ 0.60/hour in Morocco) and production conditions in Spain and Morocco. And the most affected would be the regions that concentrate most of the Spanish production of fruits and vegetables, namely the Canaries, Andalusia, Murcia, and the Region of Valencia, which are also those with the highest unemployment rates in the whole EU.

PRESIDENTE DE FEPEX, CREADA EN 1987, ESTÁ INTEGRADA POR 26 ASOCIACIONES DE ÁMBITO AUTONÓMICO O PROVINCIAL, QUE A SU VEZ ESTÁN CONSTITUIDAS POR MÁS DE 1.500 EMPRESAS AGRARIAS Y COMERCIALES.

JORGE BROTONS,

Fruit logística

Fruit logística ’12 23

Nuestra industria está sufriendo una de sus peores crisis en décadas, con precios tan bajos que no permiten cubrir ni los costes de producción. Las perspectivas de los principales organismos económicos indican que no habrá una recuperación económica global en varios años. Mirando hacia delante, la concentración de la distribución da pocas perspectivas de mejora en los precios en los próximos años.Sin embargo, en medio de estas condiciones, existen ciertas empresas del sector hortofrutícola que están aumentando sus ventas y cuota de mercado, hasta un 20% anual. ¿Cómo lo están haciendo?Mediante dos claves: innovación y marketing

en los años 80 que las dos únicas fuentes de creación de valor de la empresa son la innovación y el marketing. Todas las otras funciones son costes.

para la horticultura) siempre ha dado resultados, incluso en épocas de recesión. La innovación asegura la disponibilidad de productos atractivos para los clientes; el marketing asegura que todos los clientes potenciales conocen las ventajas de mis productos.Empecemos por innovación. Aquí hay un pequeño test que medirá el progreso de su actividad en la innovación:

costes, bajar pérdidas o aumentar calidad del producto?

manejo de inventario, de la programación de la producción o del enfriado?

La innovación en la empresa puede ser de nuevos productos, nuevos procesos o nuevos modelos de negocio. La función del gerente, más allá del día a día, debe ser prepararse para nuevos escenarios en el futuro, formas en las que complacer a los clientes con nuevos

más calidad, mejor sabor, oferta de calidad

sus procesos, es decir, cómo producir más

menos mano de obra, menos capital…)Sólo aquellos profesionales que se diferencian de los demás con mejores técnicas de producción, recolección, envase y transporte pueden mejorar cuota de mercado, un

La segunda herramienta importante es el marketing. El marketing son todos aquellos

pasos que facilitan que la venta se haga fácil a todos mis clientes potenciales. Empieza por una actividad de estudio del posible mercado, analizando la demanda que hay hacia mi producto y los similares, y nuevas formas de llegar a más clientes, vender más por momento de compra y aumentar la frecuencia de compras.

en mi producto o servicio respecto a mis competidores? ¿En qué me diferencio? Si no hay diferenciación, probablemente las ventas están basadas en costumbre o relación personal, que no son duraderas frente a las enormes fuerzas de la oferta y la demanda.

del cliente: segmentación, posicionamiento y acercamiento. Aquí la estrategia de comunicación por todos los medios disponibles es clave.

¿Cómo pueden las empresas hortofrutícolas acelerar sus procesos de innovación y marketing?

en los próximos años) y aumento de la

recursos humanos y capital adecuado, y

marketing, más allá de la comunicación, y actuar consistentemente en él. Finalmente es importante utilizar la asesoría de empresas especializadas en innovación tecnológica y marketing, pues existe el riesgo, si no se está bien asesorado, de invertir en innovación o marketing y no

CÓMO MANTENER Y AUMENTAR INGRESOS EN SU EMPRESA DURANTE ESTA CRISIS

GERENTE DE FRUITPROFITS, EMPRESA DE ASESORÍA DEDICADA AL AUMENTO DE PRODUCTIVIDAD Y MEJORA DE VENTAS DE FRUTAS Y HORTALIZAS MEDIANTE EL ANÁLISIS DE SUS PROCESOS, ESTRATEGIA DE MARKETING Y APLICACIÓN DE TECNOLOGÍA. WWW.FRUITPROFITS.COM [email protected]

MANUEL MADRID,

Tomate / Tomato

Fruit logística ’1224

CASI, SCA

Chairman: José Mª AndújarCtra. Níjar-Los Partidores. 04120 La Cañada (Almería, España)Phone / Fax: +34 950 62 60 07 / +34 950 62 61 85www.casi.es / [email protected] turnover: 193.499.852 €Main product: TomatoProduction volume: 248.495 t

BONNYSA AGROALIMENTARIA

Chairman: Jorge F. Brotons CampilloCommercial Director: Teresa Brotons C/ La Font, 1. 03550 San Juan (Alicante, España)Phone / Fax: +34 965 65 37 00 / +34 965 94 03 [email protected] turnover: 190.000.000 €Main product: Tomato, banana and tropical fruitsProduction volume: 160.000 t

VICASOL, S.C.A.

Chairman: Juan Antonio González RealManager: José Manuel FernándezCommercial Director: Isidoro Sánchez y Manuel BarrionuevoC/ Vicasol 37. 04738 Puebla de Vícar (Almería, España)Phone: +34 950 55 32 00 [email protected] turnover: 90.000.000 €Main product: Tomato, cucumber, pepper, aubergine and melonProduction volume: 100.000 t

GRANADA LA PALMA, S.C.A.

Chairman: Pedro RuizManager: David Del PinoCommercial Director: Carmelo SalgueroCrta. Nac. 340 km 342. 18730 Carchuna (Granada, España)Phone / Fax: +34 958 62 39 03/ www.lapalmacoop.com / [email protected] turnover: 88.455.090 €Main product: Cherry tomato, tomato and cucumberProduction volume: 56.000 t

AGRUPALMERIA, S.A.

Chairman: Francisco J. García QueroCtra. De Níjar km 8. Frente Aeropuerto 04120 La Cañada (Almería, España)Phone / Fax: +34 950 29 06 60 / +34 950 29 23 [email protected] turnover: 75.000.000 €Main product: Tomatoes, bunch, plum, lose, green salda, marmande RafProduction volume: 100.000 t

GRUPO LA CAÑA (MIGUEL GARCÍA SÁNCHEZ E HIJOS S.A. Y EUROCASTELL, S.A.T.)

Manager: Jesús Fco. García PuertasCommercial Director: Antonio García PuertasCtra. Vieja de Carchuna s/n. Puntalón. 18600 Motril (Granada, España)Phone / Fax: +34 958 60 10 52 / +34 958 83 04 [email protected] turnover: 67.300.000 €Main product: Cherry tomato, pepper, avocado, mango, custard apple, etc.Production volume: 90.000 t

AN, S. Coop.

Chairman: Francisco ArrarasManager: Jesús SarasaCommercial Director: Iván Romero / Juan Miguel ArtazcozCampo de Tajonar, s/n. 31192 Tajonar (Navarra, España)Phone / Fax: + 34 948 29 94 00 / + 34 948 29 94 20www.grupoan.comYearly turnover: 67.000.000 €Main product: Tomato, lettuce, asparragus, peach, appleProduction volume: 170.000 t

DUNIA CAMPOALMERÍA S.L.

Chairman: Serafín Mateos CallejónParaje la Cumbre s/n. 04700 El Ejido (Almería, España)Phone / Fax: +34 950 02 12 24 / [email protected] turnover: 45.000.000 €

Main product: TomatoProduction volume: 60.000 t

S.A.T. AGRÍCOLA PERICHAN

Chairman: Celestino Méndez RajaManager: Celestino Méndez RajaCommercial Director: Juan Cruz Sánchez CabezasCañada de Gallego, s/n. 30876 Mazarrón (Murcia, España)Phone / Fax: +34 968 15 88 10 / +34 968 15 88 [email protected] turnover: 45.000.000 €Main product: Tomato, cucumber and beansProduction volume: 60.000 t

FULGENCIO SPA, S.L.

Chairman: Fulgencio Spa VázquezManager: Javier Jiménez MedinaCommercial Director: Francisco Ruiz ReyesAvda. de las Palmeras, 9 Carchuna-Motril (Granada, España)Phone: + 34 958 623 136 www.fsagro.com / [email protected] turnover: 43.000.000 €Main product: Tomato, cucumber, cherry and beansProduction volume: 45.000 t

HORTAMAR, S.C.A.

Chairman: Juan Montoya JiménezCommercial Director: Juan Vergara GóndoraCtra. De Alicún, 148. 04740 Roquetas del Mar (Almería, España)Phone / Fax: +34 950 33 82 05 / +34 950 33 82 50www.hortamar.es / [email protected] turnover: 35.750.000 €Main product: Tomato, cucumber, pepper and melonProduction volume: 50.000 t

CASUR, S.C.A.

Chairman: José Martínez PorteroManager: Antonio Mª Martín CamposCommercial Director: Miembro de UNICA GROUP, S.C.A.Paraje Pisaica de la Virgen s/n. 04210 Viator (Almería, España)Phone / Fax: + 34 950 30 60 00 / +34 950 30 60 17www.casur.com / [email protected] turnover: 33.000.000 €Main product: Tomato (specialists with more than 6 references)Production volume: 31.000 t

FERVA S.A.T.

Chairman: Marcos Hidalgo LópezManager: Francisco Sabio PérezCommercial Director: Emilio Villegas BenalidesCtra. De Málaga, km 417,7. Diseminado, 3. San Nicolás, La Mojonera (Almería, España)Phone / Fax: +34 950 60 33 07 / +34 950 60 34 30 / +34 950 60 34 33www.ferva.com / [email protected] turnover: 33.000.000 €Main product: Tomato

S.A.T. HORTICHUELAS

Chairman: Juan Antonio Maldonado ValdecillosManager: Manuel Escamez GarcíaBarrio Ojeda s/n El Parador. 04721 Roquetas de Mar (Almería, España)Phone / Fax: +34 950 34 90 16 / +34 950 34 23 58www.hortichuelas.es / [email protected] turnover: 30.000.000 €Main product: TomatoProduction volume: 30.000 t

CAPARROS NATURE, S.L.

Chairman: Pedro CaparrósCtra de Níjar km 8,400. 04130 El Alquián (Almería, España)Phone / Fax: +34 950 60 02 31 / +34 950 297 268www.caparrosnature.com / [email protected] / facebook/caparrosnatureYearly turnover: 28.000.000 €Main product: TomatoProduction volume: 30.000 t

S.A.T HORTOVENTAS N. 4534

Chairman: Salvador Martín MartínManager: Jesús PalmaCommercial Director: Mario MorenoC/ Estación s/n. 18125 Ventas de Zafarraya (Granada, España)Phone / Fax: +34 958 36 21 90 / +34 958 36 20 [email protected] turnover: 27.000.000 €Main product: Salad tomato, artichoke, beans, cauliflower and lettuceProduction volume: 45.000 t

MERCOMOTRIL S.A.

Chairman: Ad Ven Der WindtManager: Adrian Picazo MartínezCommercial Director: Antonio Palamós MontañanaPol. Alborán. Parc 54. 18600 Motril (Granada, España)Phone / Fax: +34 958 60 16 00 / +34 958 82 08 62www.mercomotril.com / [email protected] turnover: 25.000.000 €Main product: Cherry tomato, cucumberProduction volume: 22.000 t

NTRA. SRA. DE LAS VIRTUDES, S.C.A.

Chairman: Bartolomé Ramírez SánchezManager: Gregorio Sánchez CaroCommercial Director: Antonio Sánchez MuñozCtra. Cádiz-Málaga km 21. 11149 Conil de la Frontera (Cádiz, España)Phone / Fax: +34 956 44 08 35/ +34 956 44 07 61www.coagrico.com / [email protected] turnover: 19.500.000 €Main product: Tomato, pepperProduction volume: 23.000 t

LAS MARISMAS DE LEBRIJA

Chairman: Jesús Valencia MatosManager: Juan García GonzálezPol.Ind Las Marismas P.1029. 41740 Lebrija (Sevilla, España)Phone / Fax: +34 955 97 70 11 / +34 955 97 70 [email protected] turnover: 18.000.000 €Main product: Tomato concentrateProduction volume: 33.000 t

FRUNET S.L.

Chairman: Antonio LavaoCommercial Director: Javier LópezCtra. Algarrobo km 2,5. 29750 El Agarrobo (Málaga, España)Phone / Fax: +34 952 52 75 10 / +34 952 52 75 11www.frunet.net / [email protected] turnover: 15.750.000 €Main product: Cherry tomatoProduction volume: 8.400 t

MERCOPHAL, S.L.

Commercial Director: Juan José VargasBulevar Ciudad de Vícar, 1226 04738 Puebla de Vícar (Almería, España)Phone / Fax: + 34 950 34 61 15 / + 34 950 34 09 [email protected] turnover: 14.500.000 €Main product: Tomato and lettuceProduction volume: 12.000 t

Quién es quién en el sector DEL TOMATE

Fruit logística

Fruit logística ’12 25

PARQUE NATURAL S.COOP.AND.

Chairman: José Ángel González GarcíaManager: Director Financiera: José Mariano López GalindoCommercial Director: Juan Gabriel HernándezCtra. San José km 5. 04117 Níjar (Almería, España)Phone / Fax: +34 950 61 10 40 / +34 950 61 10 42www.parquenat.comYearly turnover: 14.000.000 €Main product: TomatoProduction volume: 18.500 t

PROCAM S.C.A.

Chairman: Antonio Castilla AlcaideManager: Fernando Martín CallejónCommercial Director: José María CuadradoCtra. Almería km 1,6. 18600 Motril (Granada, España)Phone / Fax: +34 958 820 197 / +34 958 600 306www.procamsca.com / [email protected] turnover: 13.000.000 €Main product: Dutch cucumber and cherry tomato (convencional and organic) and subtropical fruits (avocado and cherimoyas)Production volume: 14.000 t

VEGA COSTA MOTRIL, S.L.

Chairman: Manuel Fernández SolerManager: Modesto Gaspar MonllorCtra. De Almería, km 3,4. 18720 Motril (Granada, España)Phone / Fax: +34 958 83 55 60 / +34 958 83 56 [email protected] turnover: 11.000.000 €Main product: Cherry tomatoProduction volume: 4.500 t

S.A.T. VALERÓN

Chairman: Ismael López FalcónManager: Ismael López Falcón, Narciso López PérezCommercial Director: Tomás López FalcónAngel Guimerá, 3. 35259 Ingenio (Gran Canaria, España)Phone / Fax: +34 928 12 42 63 / +34 928 12 42 [email protected] turnover: 5.000.000 €Main product: Round tomato, pear and cocktailProduction volume: 8.000 t

VEGACAÑADA S.A.

Chairman: Diego Amat NavarroManager: Francisco LópezCommercial Director: Andrés SolerAutovía del Mediterráneo, Salida 456.

Paraje Los Mayorales s/n. 04130 El Alquián (Almería, España)Phone / Fax: +34 902 50 10 95 / +34 902 50 10 [email protected] product: TomatoProduction volume: 60.200 t

COPROHNIJAR, S.C.A.

Chairman: Antonio García PadillaCommercial Director: Miguel Pérez LópezOlivar, s/n. 04117 Níjar (Almería, España)Phone / Fax: +34 950 36 60 15 / +34 950 36 60 89www.coprohnijar.com / [email protected] product: Tomato, squash, pepperProduction volume: 40.000 t

INVER S.T.

Chairman: Manuel López OjedaManager: Manuel López MartínezCtra. Málaga, 427. 04740 Roquetas de Mar (Almería, España)Phone / Fax: +34 950 34 24 62 / +34 950 34 37 14www.satinver.comMain product: Tomato, pepper, melon and cucumberProduction volume: 16.800 t

AGRÍCOLA NAVARRO DE HARO, S.L.

Manager: José Alonso Navarro FloresCtra de Palomares a Cueva km 2. 04617 Palomares (Almería, España)Phone / Fax: +34 950 46 75 39 / +34 950 46 73 [email protected] product: Tomato and watermelonProduction volume: Tomato: 6.000 t, melon and watermelon: 21.000 t, iceberg lettuce and escarole: 14.500.000 unid.

LOOIJE AGUILAS S.L.

Chairman: Jos LooijeManager: Juan José LópezCommercial Director: Juan José LópezCtra. Los arejos km 5,2. 30880 Aguilas (Murcia, España)Phone / Fax: +34 968 43 92 87www.looijetomaten.nl / [email protected] product: Cherry tomatoProduction volume: 1.500 t

BLAKY FRUIT, S.L.

Matagorda. Ctra. Almerimar, 04700 El Ejido (Almería, España)Phone / Fax: + 34 950 498 508 / + 34 950 498 [email protected] product: Tomato and pepper

HORTASOL

Ctra. San José km 2,5. 04117 Níjar (Almería, España)Phone / Fax: + 34 950 380 673 /+ 34 950 380 [email protected] product: Tomato

TOMARAF

Ciudad del Transporte. Parcela 10. Nave 7. 04740 La Mojonera (Almería, España)Phone / Fax: + 34 950 558 [email protected] product: Tomato

Quién es quién en el sector DEL TOMATE

Importadores / Importers

Fruit logística ’1226

EN EL MERCADO ALEMÁN”

DIRECTOR GERENTE DE LANDGARD OBST - GEMÜSE GMBH, GRUPO IMPORTADOR ALEMÁN INTEGRADO POR PRODUCTORES DE FRUTAS Y HORTALIZAS, FLORES Y PLANTAS.

ENTREVISTA A MARTÍN BAUMERT,

“Spain is very well positioned in the German market”

Interview with Martin Baumert, managing director at Landgard Obst - Gemüse GmbH, German importer that gathers producers of fruits, vegetables, flowers, and plants.

Which is the situation of Spanish products in the Ger-man market?The crisis and the E. coli issues we experienced last year in Germany have had a strong influence on con-sumption, but we can say that Spain has gained back these consumers’ trust. Furthermore, during summer, autumn and winter, Spanish products are principal in Germany. I’m sure that there are not enough alterna-tives now in winter, which reinforces Spain’s role, which is as important as it used to be in Germany. In general, I consider that Spain is very well positioned in the Ger-man market.What didn’t recover are product prices, mostly of veg-etables and citrus during 2011. For that reason, our work with a view to the future is collaborating with customers and producers to know their needs and to study how we can add more value to the product, aim-ing at higher profitability.

Why big distribution bases its strategy on price only? I think each supermarket is looking for its own phi-losophy, its own path, whether it is product quality, packaging, price, etc. adapting to current demands, as the situation of families also changed in Germany like in Europe: there are more singles with different purchasing systems. For instance, in Germany, local productions will be very important as a strategy for the demand of these has grown after the E. coli crisis, given that German consumers are more demanding now and look for total product reliability; they want to know what they are eating, where it comes from, they want to consume products grown in their region,

they are concerned about the environment, haulage costs, they want their products to have undergone as few treatments as possible, etc. Many factors now and German supermarkets must find a new formula to earn customers’ trust.

To meet these needs of German consumers, what should Spanish producers do?We work in a very dynamic market, so that Spanish producers must be in constant evolution as for their customers’ demand, always alert, trying to innovate for customers to differentiate them from their competitors. Spanish producers must be watching the business, collaborating closely with their main customer, with the market; one cannot sleep, and what was talked about one year ago, is history.

Do you think that consumers, besides asking for low prices, are looking for experiences being willing to pay more for them?I think there are always customers willing to pay more for a product, and there still will be, like those who prefer organic or local produce. But 50% German con-sumers go to discount establishments and they want to acquire good products, so that we will always be under pressure as for quality, and we must find a way where price made up for that quality. One of the pos-sible paths would involve that distributors and produc-ers cut their costs. In the end, this is the only formula to guarantee success, together with good collaboration between producers and department stores, and finally, between all members of the value chain.

Fruit logística

Fruit logística ’12 27

NOTICIA

EMBALAJE ESTANDARIZADO Y SOSTENIBLE EN FRUIT LOGÍSTICALA MARCA ESPAÑOLA PLAFORM PRESENTARÁ EN BERLÍN LAS PRINCIPALES VENTAJAS DE SUS CAJAS DE CARTÓN ONDULADO PARA FRUTAS Y HORTALIZAS: CALIDAD, AHORRO DE COSTES, COMPATIBILIDAD, HIGIENE, SOSTENIBILIDAD, FUERZA DE GRUPO Y MARKETING.

Con el apoyo del ICEX, el Grupo Plaform asiste, un año más, a la cita de Berlín para promocionar su embalaje estandarizado y sostenible. En el stand A-5, situado en el Hall 11.2, divulgará las principales ventajas competitivas del envase de cartón ondulado líder en el segmento de frutas y hortalizas.Plaform es un sistema compatible. Ha sido la primera marca española en adherirse al Common Footprint (CF), un sistema de estandarización de tamaños promovido a nivel europeo por FEFCO, la Federación Europea de Fabricantes de Cartón Ondulado. El CF facilita los intercambios comerciales entre diversos productores de Europa y EEUU. Las bandejas Plaform ya llevan el sello CF creado por FEFCO. Así, el Grupo Plaform asume el liderazgo en la implantación de este estándar, que en España es la Norma UNE 137005.Gracias a esta homologación de las medidas exteriores de las cajas, es posible paletizar y comercializar de manera conjunta cualquier tipo de frutas y hortalizas en bandejas apilables. Se pueden configurar palés mixtos seguros y con suficiente altura para aprovechar al máximo el espacio en camiones y almacenes. Además, con la estandarización se logra un gran impacto en el punto de venta, que resulta más atractivo y refuerza la imagen de marca.

Fruit logística ’1228

Pimiento / Pepper

Si

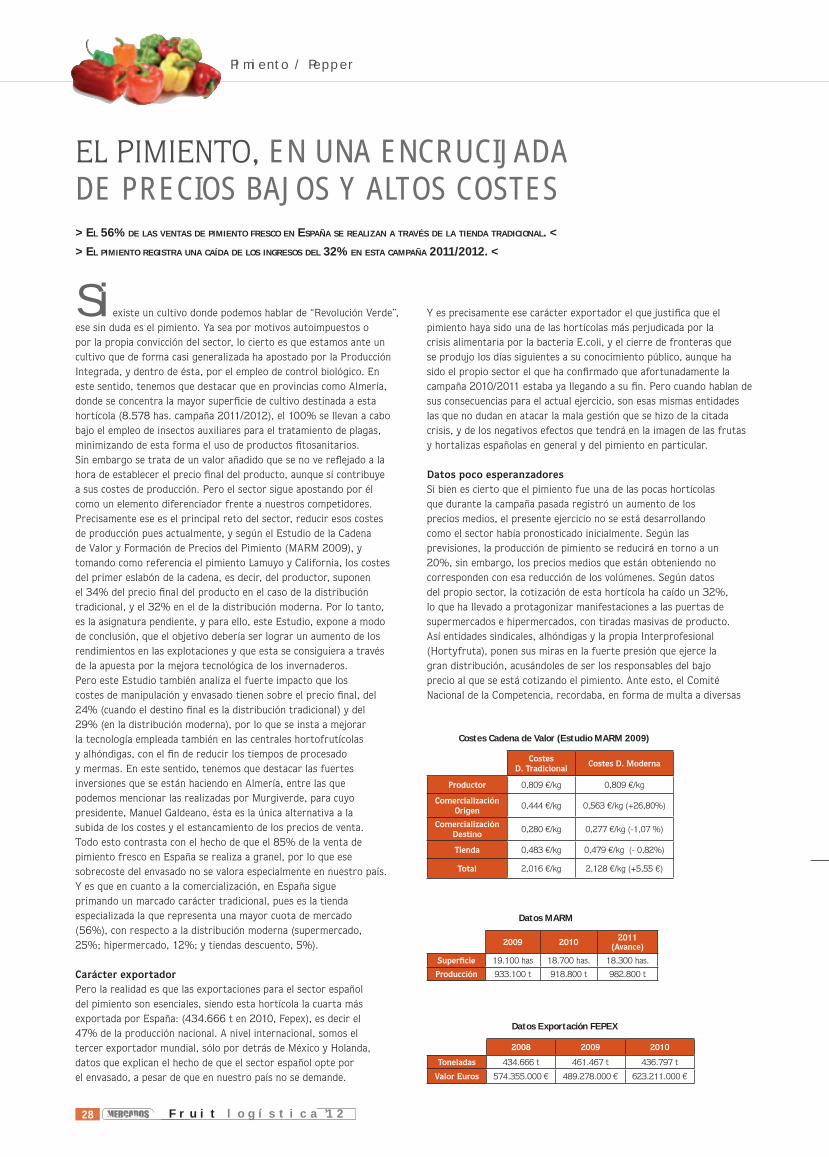

EN UNA ENCRUCIJADA DE PRECIOS BAJOS Y ALTOS COSTES> EL 56% DE LAS VENTAS DE PIMIENTO FRESCO EN ESPAÑA SE REALIZAN A TRAVÉS DE LA TIENDA TRADICIONAL. <

> EL PIMIENTO REGISTRA UNA CAÍDA DE LOS INGRESOS DEL 32% EN ESTA CAMPAÑA 2011/2012. <

Costes Cadena de Valor (Estudio MARM 2009)

Datos MARM

Datos Exportación FEPEX

Fruit logística ’12 29

Fruit logística

Pepper, at a crossroads of low prices and high costs

> 56% of sales of fresh pepper in Spain take place at traditional retailers. <

> The sector of pepper to experience a drop of income by 32% in the 2011/2012 trade campaign. <