crecimiento del retail chileno encolombia

DESCRIPTION

Jaime Zawadzki - Gerente General Easy ColombiaTRANSCRIPT

CrecimientodelRetailChilenoenColombia

Mayo2012

1

SectorComercioysuimpacto…..

Los canales modernos y su desarrollo han tenido un impacto significativo: – Expansión de la demanda – Deflación – Dinamizador de la eficiencia industrial – Educación del consumidor – Desarrollo y modernización del canal tradicional

• El Comercio, motor del crecimiento económico – 6.9% en el 2011

• Mayor generador de empleo – mas del 21%

2

ResumendelaEmpresa

3

Supermarkets 189

29

35

9

262

269

48

-

14

331

152

-

-

-

152

74

-

-

2

76

-

4

-

-

4

684

81

35

25

825

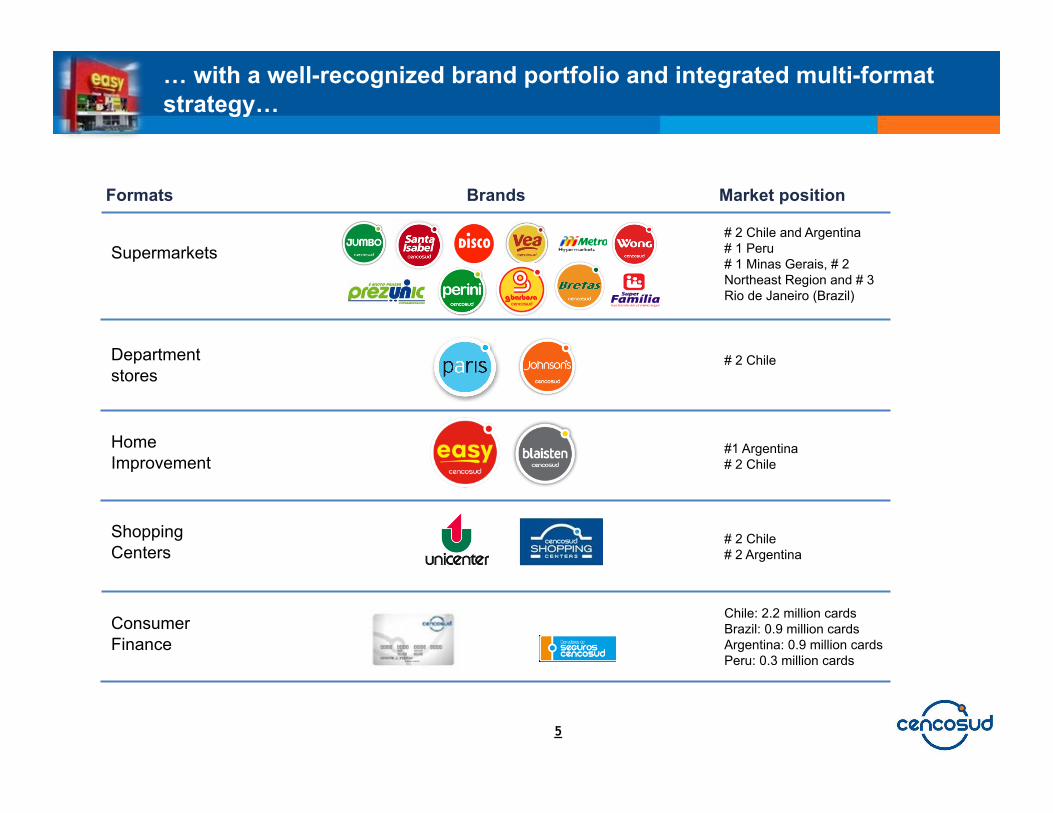

Cencosud is a leading multi-format retailer in Latin America…

Chile 1,295,240 m2 selling space

189 Supermarkets

29 Home improvement stores

35 Department stores

9 Shopping Centers

2.2 million active credit cards

Argentina 1,121,563 m2 selling space

269 Supermarkets

48 Home improvement stores

14 Shopping Centers

0.9 million active credit cards

Brazil 380,845 m2 selling space

152 Supermarkets

0.9 million active credit cards (JV with Bradesco)

Colombia 35,360 m2 selling space

4 Home improvement sores

Peru 288,081 m2 selling space

74 Supermarkets

2 Shopping Centers

0.3 million active credit cards

Note: Figures exclude Prezunic (31 stores and net sales of R$2.2 billion during 2011) acquired on January 2, 2012 1 As of March 15, 2012 2 EBITDA, further adjusted to exclude the effect of exchange differences, increase on revaluation of investment properties, results from price level restatement and negative goodwill associated with Johnson’s acquisition

4

Numberofstores: 825Sellingspace: 3,121,089m2

Numberofcustomers: 800mmNumberofemployees: 131,505

Creditcardsissued: 4.2mmMarketcapitalizaIon1: US$15,108mmNetrevenues: US$15,625mm

AdjustedEBITDA2: US$1,287mmLoansoutstanding: US$1.5billion

Key metrics (2011)

Stores and shopping centers (2011)

Home Improvement

Department stores

Shopping Centers

Total

Formats Total

… with a well-recognized brand portfolio and integrated multi-format strategy…

Formats

Supermarkets

Department stores

Home Improvement

Shopping Centers

Consumer Finance

Brands Market position

# 2 Chile and Argentina # 1 Peru # 1 Minas Gerais, # 2 Northeast Region and # 3 Rio de Janeiro (Brazil)

# 2 Chile

#1 Argentina # 2 Chile

# 2 Chile # 2 Argentina

Chile: 2.2 million cards Brazil: 0.9 million cards Argentina: 0.9 million cards Peru: 0.3 million cards

5

2007

2006

2005

2004

2003

2002

2000

1993

1988

1982

1976

2008

2009

Source: Cencosud, Factset Note: Figures exclude Prezunic (31 stores and net sales of R$2.2 billion during 2011) acquired on January 2, 2012 1 EBITDA, further adjusted to exclude the effect of exchange differences, increase on revaluation of investment properties, results from price level restatement and negative goodwill associated with Johnson’s

acquisition 2 As of December 31, 2011

2010

Opened the first supermarket

IPO in the Santiago Stock

Exchange

…and a proven track record in successfully integrating acquisitions

And a new cycle of growth has began

6

2011

2012

2006 2011

# of stores

2011 vs. 2006

Selling space (mm sq. meters)

Net revenues ($ million)

Adjusted EBITDA ($ million)1

486

1.9

5,874

495

825

3.1

15,625

1,287

1.7x

1.6x

2.7x

2.6x

Expansion in key metrics

Market capitalization ($ million) 6,223 13,1082 2.1x

Chilean market consolidation

During last five years Cencosud has made 8

acquisitions for more than US$2.2 billions

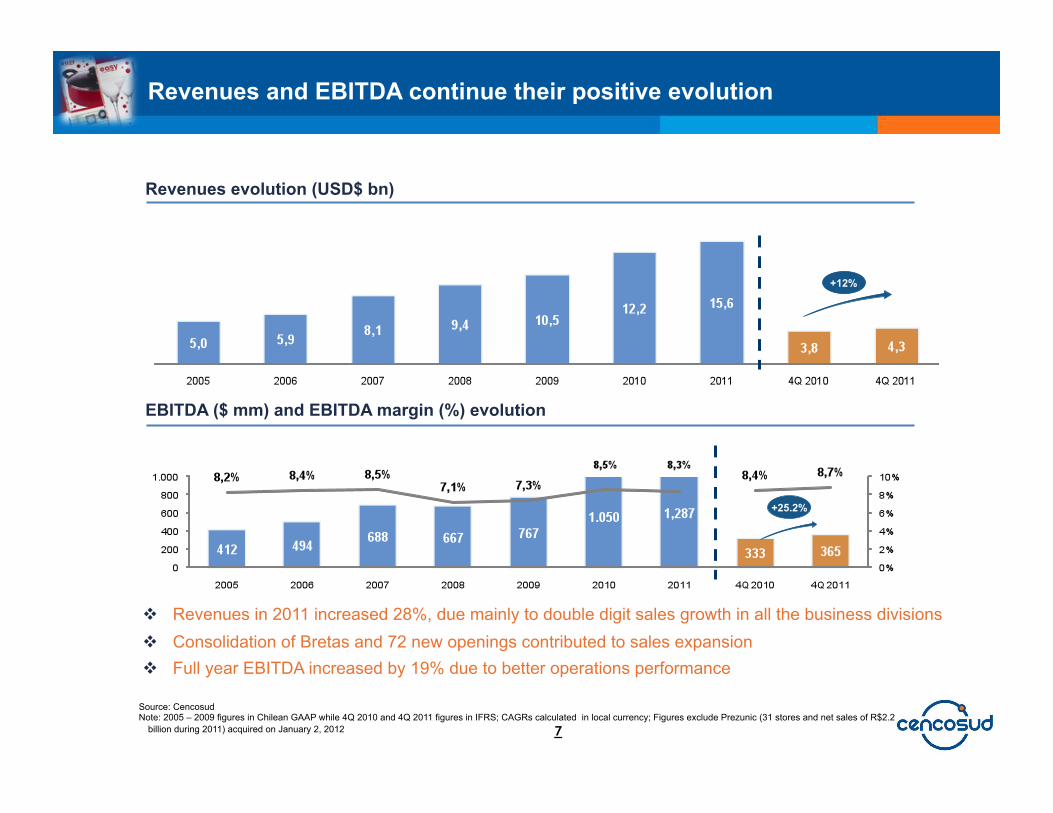

Revenues in 2011 increased 28%, due mainly to double digit sales growth in all the business divisions Consolidation of Bretas and 72 new openings contributed to sales expansion Full year EBITDA increased by 19% due to better operations performance

Revenues evolution (USD$ bn)

EBITDA ($ mm) and EBITDA margin (%) evolution

Revenues and EBITDA continue their positive evolution

Source: Cencosud Note: 2005 – 2009 figures in Chilean GAAP while 4Q 2010 and 4Q 2011 figures in IFRS; CAGRs calculated in local currency; Figures exclude Prezunic (31 stores and net sales of R$2.2

billion during 2011) acquired on January 2, 2012 7

+12%

+25.2%

2011 2010

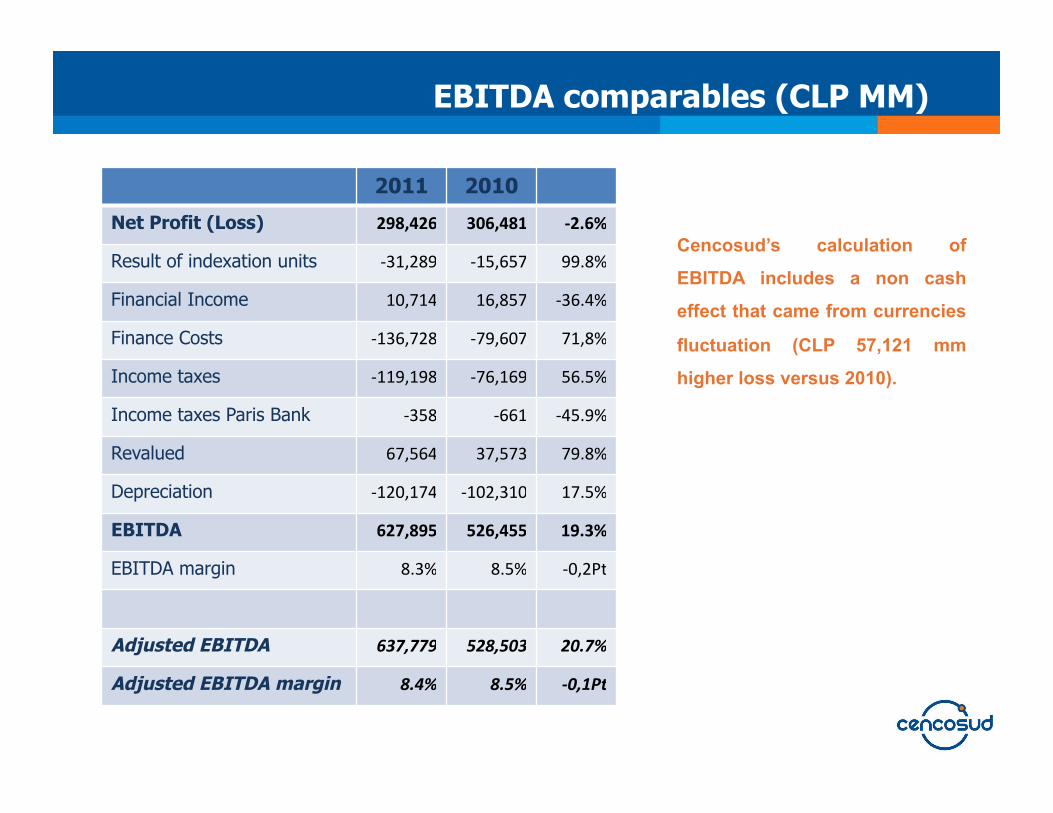

Net Profit (Loss) 298,426 306,481 ‐2.6%

Result of indexation units ‐31,289 ‐15,657 99.8%

Financial Income 10,714 16,857 ‐36.4%

Finance Costs ‐136,728 ‐79,607 71,8%

Income taxes ‐119,198 ‐76,169 56.5%

Income taxes Paris Bank ‐358 ‐661 ‐45.9%

Revalued 67,564 37,573 79.8%

Depreciation ‐120,174 ‐102,310 17.5%

EBITDA 627,895 526,455 19.3%

EBITDA margin 8.3% 8.5% ‐0,2Pt

Adjusted EBITDA 637,779 528,503 20.7%

Adjusted EBITDA margin 8.4% 8.5% ‐0,1Pt

EBITDA comparables (CLP MM)

Cencosud’s calculation of

EBITDA includes a non cash

effect that came from currencies

fluctuation (CLP 57,121 mm

higher loss versus 2010).

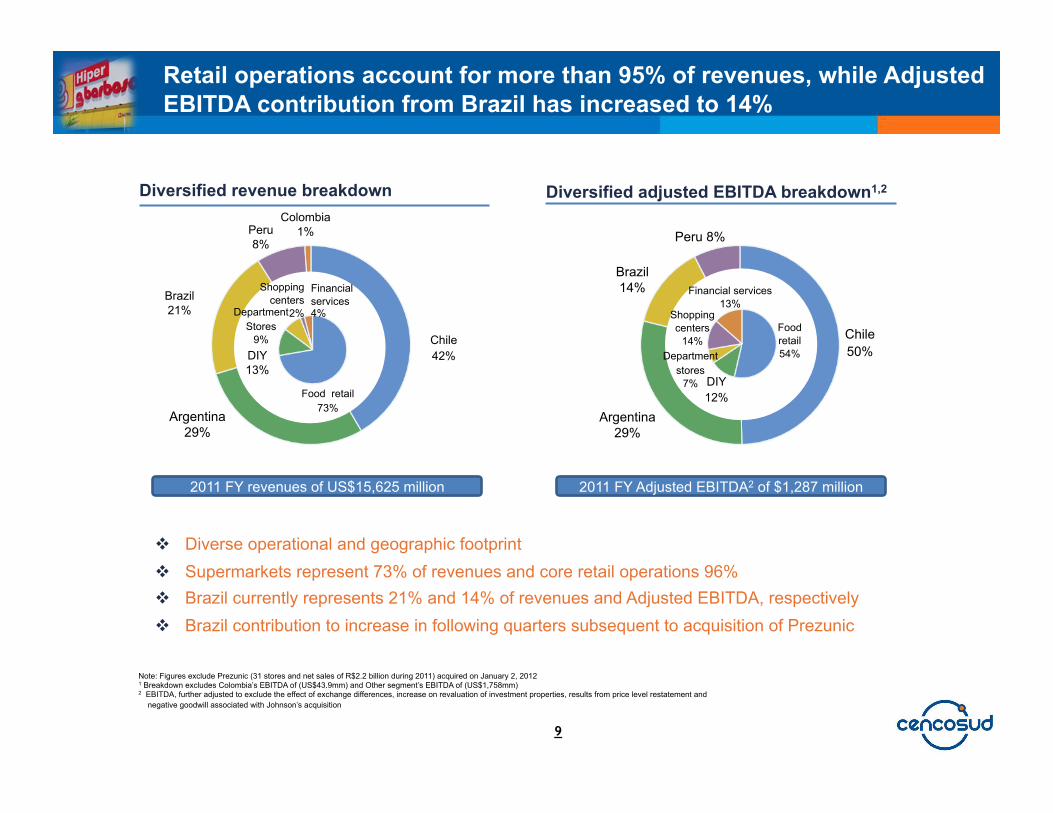

Retail operations account for more than 95% of revenues, while Adjusted EBITDA contribution from Brazil has increased to 14%

Diversified revenue breakdown Diversified adjusted EBITDA breakdown1,2

2011 FY revenues of US$15,625 million

9

2011 FY Adjusted EBITDA2 of $1,287 million

Note: Figures exclude Prezunic (31 stores and net sales of R$2.2 billion during 2011) acquired on January 2, 2012 1 Breakdown excludes Colombia’s EBITDA of (US$43.9mm) and Other segment’s EBITDA of (US$1,758mm) 2 EBITDA, further adjusted to exclude the effect of exchange differences, increase on revaluation of investment properties, results from price level restatement and

negative goodwill associated with Johnson’s acquisition

Diverse operational and geographic footprint Supermarkets represent 73% of revenues and core retail operations 96% Brazil currently represents 21% and 14% of revenues and Adjusted EBITDA, respectively Brazil contribution to increase in following quarters subsequent to acquisition of Prezunic

Chile 42%

Argentina 29%

Brazil 21%

Peru 8%

Colombia 1%

Chile 50%

Argentina 29%

Brazil 14%

Peru 8%

Food retail 54%

DIY 12%

Department stores

7%

Shopping centers

14%

Financial services 13%

Food retail 73%

DIY 13%

Department Stores

9%

Shopping centers

2%

Financial services 4%

FinancialHighlights

10

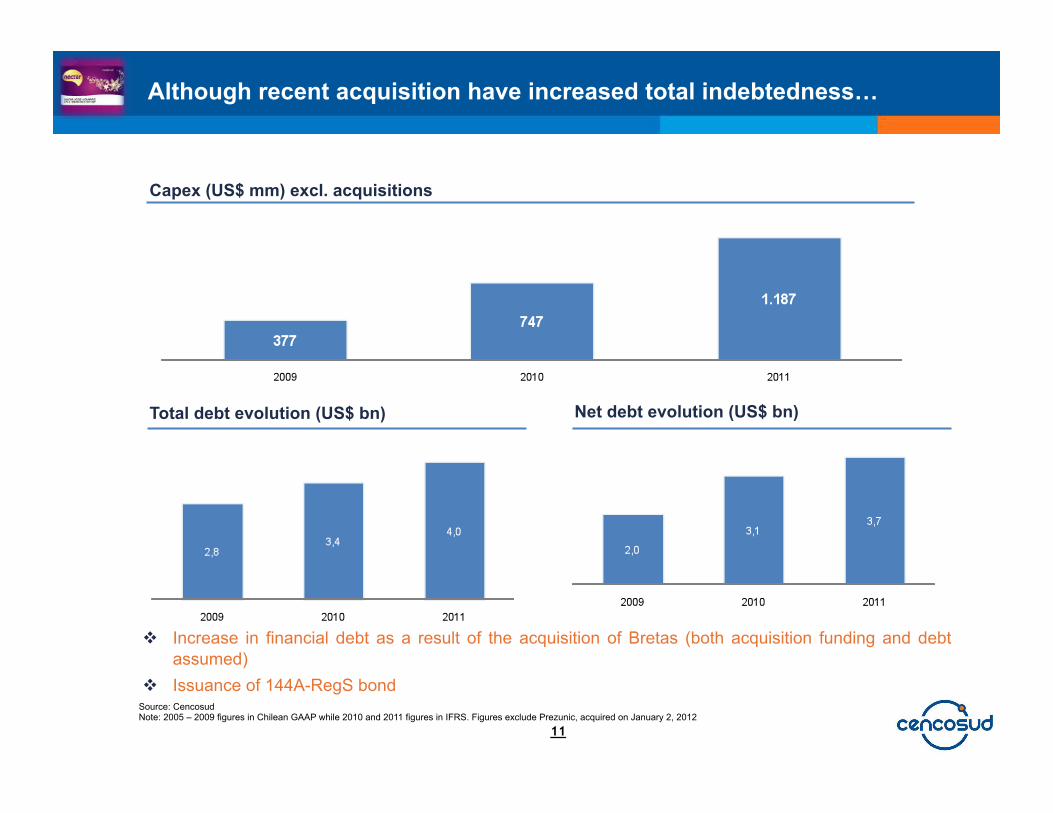

Although recent acquisition have increased total indebtedness…

Total debt evolution (US$ bn) Net debt evolution (US$ bn)

Capex (US$ mm) excl. acquisitions

Source: Cencosud Note: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS. Figures exclude Prezunic, acquired on January 2, 2012

Increase in financial debt as a result of the acquisition of Bretas (both acquisition funding and debt assumed)

Issuance of 144A-RegS bond

11

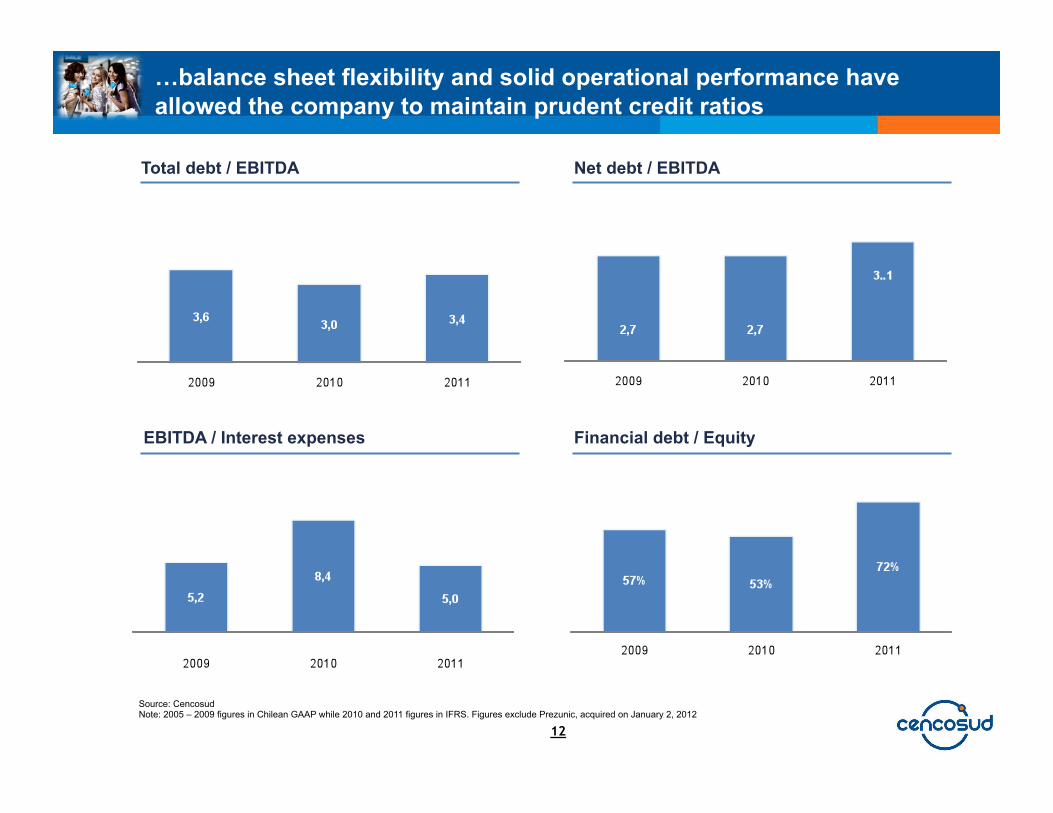

…balance sheet flexibility and solid operational performance have allowed the company to maintain prudent credit ratios

Net debt / EBITDA

Financial debt / Equity

Total debt / EBITDA

EBITDA / Interest expenses

12

Source: Cencosud Note: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS. Figures exclude Prezunic, acquired on January 2, 2012

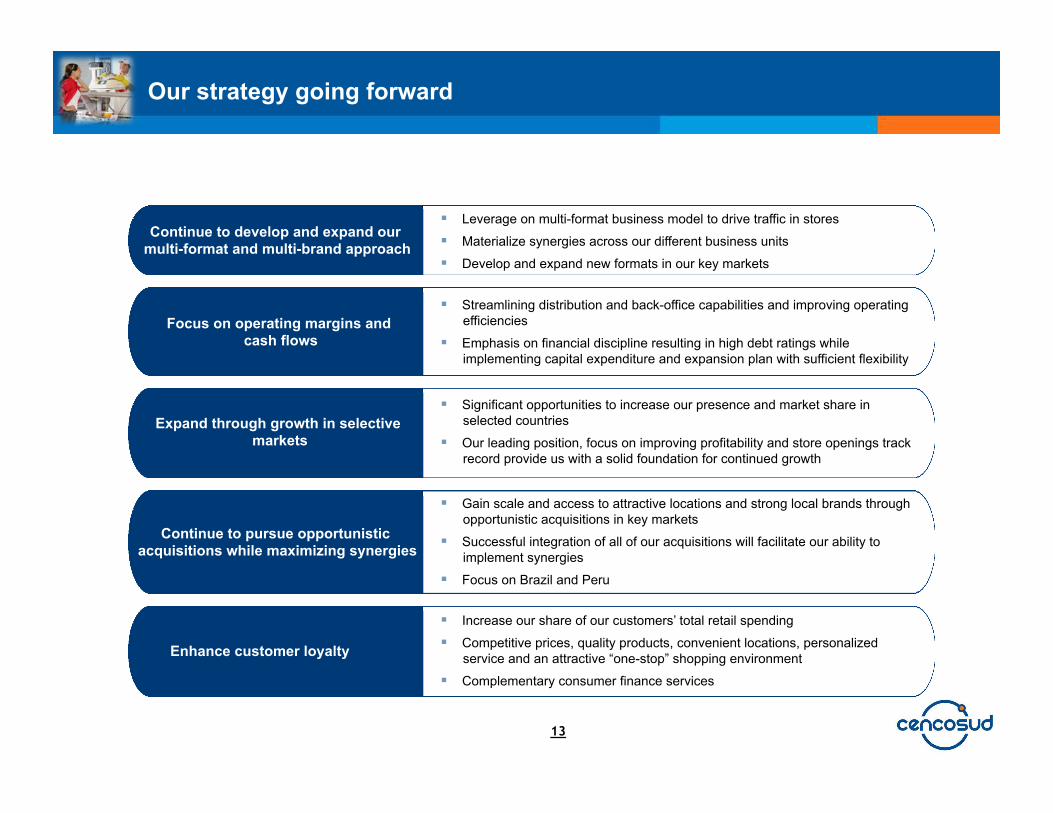

Our strategy going forward

Leverage on multi-format business model to drive traffic in stores

Materialize synergies across our different business units

Develop and expand new formats in our key markets

Continue to develop and expand our multi-format and multi-brand approach

Focus on operating margins and cash flows

Expand through growth in selective markets

Continue to pursue opportunistic acquisitions while maximizing synergies

Enhance customer loyalty

13

Streamlining distribution and back-office capabilities and improving operating efficiencies

Emphasis on financial discipline resulting in high debt ratings while implementing capital expenditure and expansion plan with sufficient flexibility

Significant opportunities to increase our presence and market share in selected countries

Our leading position, focus on improving profitability and store openings track record provide us with a solid foundation for continued growth

Gain scale and access to attractive locations and strong local brands through opportunistic acquisitions in key markets

Successful integration of all of our acquisitions will facilitate our ability to implement synergies

Focus on Brazil and Peru

Increase our share of our customers’ total retail spending

Competitive prices, quality products, convenient locations, personalized service and an attractive “one-stop” shopping environment

Complementary consumer finance services

PrincipalesdetallesdelNegocio

14

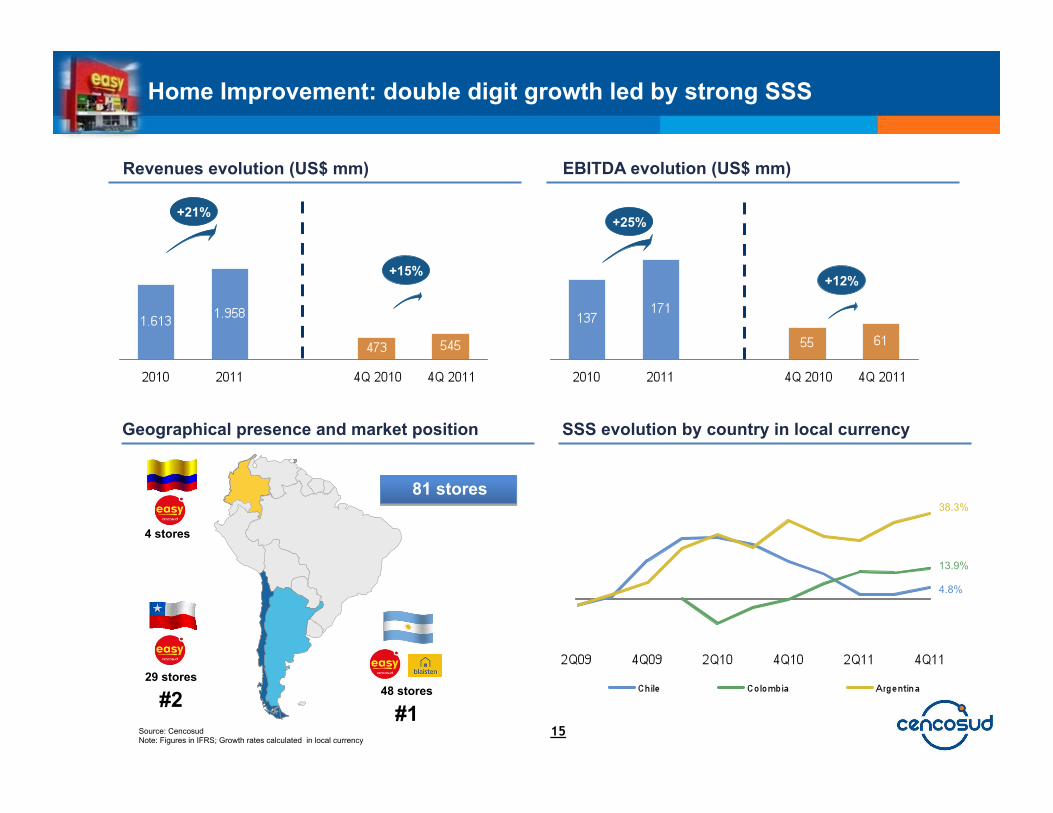

Geographical presence and market position

EBITDA evolution (US$ mm) Revenues evolution (US$ mm)

29 stores

#2

4 stores

48 stores

#1

81 stores

SSS evolution by country in local currency

Home Improvement: double digit growth led by strong SSS

15

+21%

+15%

+25%

+12%

Source: Cencosud Note: Figures in IFRS; Growth rates calculated in local currency

4.8%

13.9%

38.3%

Source: Cencosud Note: Figures in IFRS; Growth rates calculated in local currency 1 As of September 2011, does not include acquisition of Johnson’s

SSS evolution in local currency

Department Stores: recovering same store sales growth

35 stores

16

EBITDA evolution (US$ mm) Revenues evolution (US$ mm)

+16%

+3%

+20%

+16%

40 stores

Market Share by selling space – Chile1

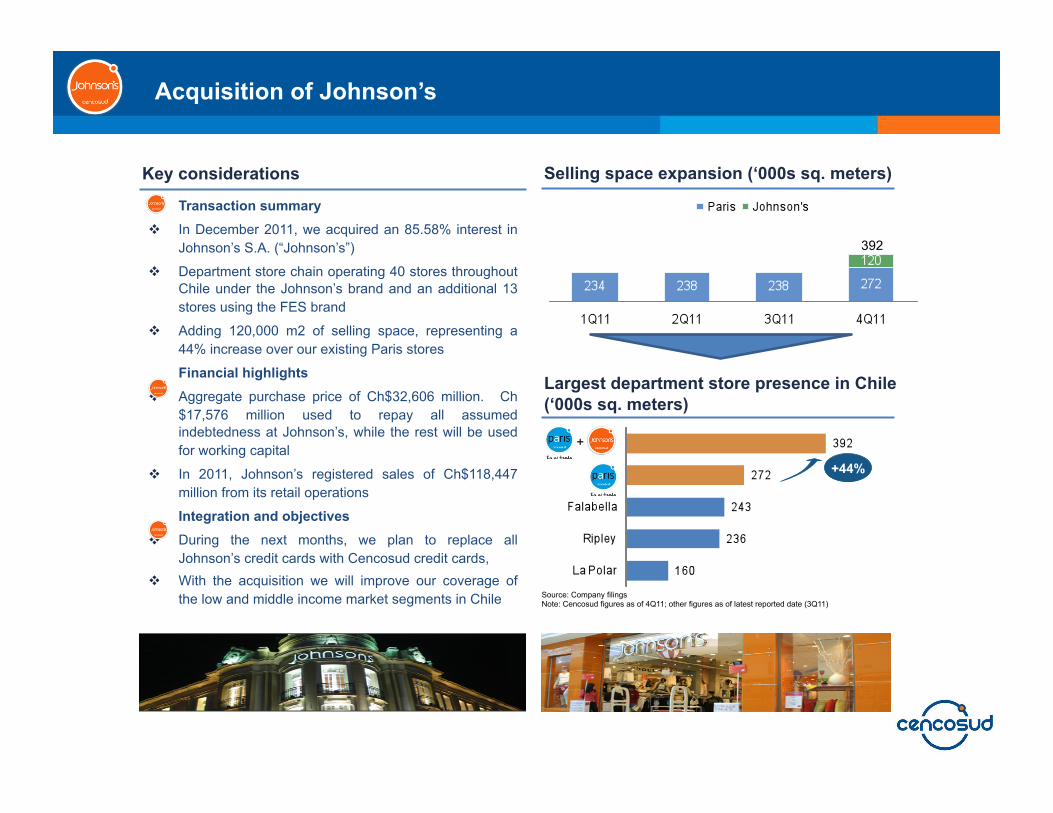

Acquisition of Johnson’s

Transaction summary In December 2011, we acquired an 85.58% interest in

Johnson’s S.A. (“Johnson’s”)

Department store chain operating 40 stores throughout Chile under the Johnson’s brand and an additional 13 stores using the FES brand

Adding 120,000 m2 of selling space, representing a 44% increase over our existing Paris stores

Financial highlights Aggregate purchase price of Ch$32,606 million. Ch

$17,576 million used to repay all assumed indebtedness at Johnson’s, while the rest will be used for working capital

In 2011, Johnson’s registered sales of Ch$118,447 million from its retail operations

Integration and objectives During the next months, we plan to replace all

Johnson’s credit cards with Cencosud credit cards, With the acquisition we will improve our coverage of

the low and middle income market segments in Chile

Key considerations Selling space expansion (‘000s sq. meters)

392

Largest department store presence in Chile (‘000s sq. meters)

+44%

Source: Company filings Note: Cencosud figures as of 4Q11; other figures as of latest reported date (3Q11)

+

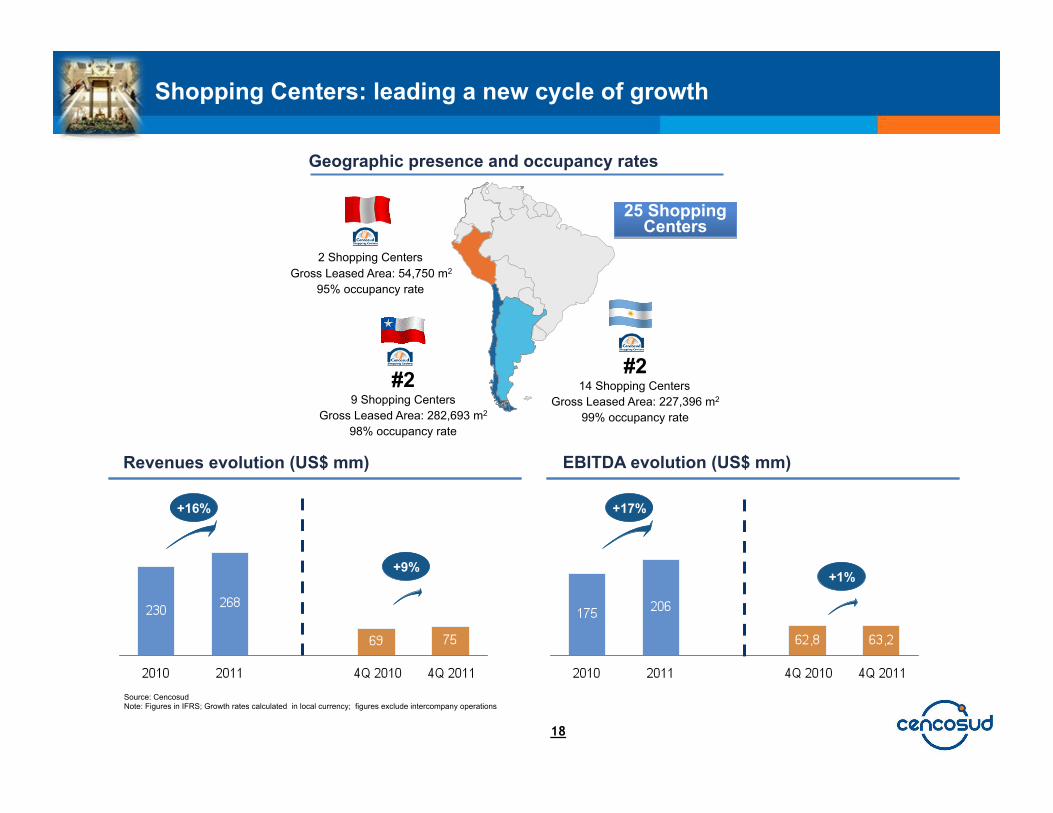

Geographic presence and occupancy rates

#2 14 Shopping Centers

Gross Leased Area: 227,396 m2

99% occupancy rate

#2 9 Shopping Centers

Gross Leased Area: 282,693 m2

98% occupancy rate

2 Shopping Centers Gross Leased Area: 54,750 m2

95% occupancy rate

25 Shopping Centers

Shopping Centers: leading a new cycle of growth

18

EBITDA evolution (US$ mm) Revenues evolution (US$ mm)

+16%

+9%

+17%

+1%

Source: Cencosud Note: Figures in IFRS; Growth rates calculated in local currency; figures exclude intercompany operations

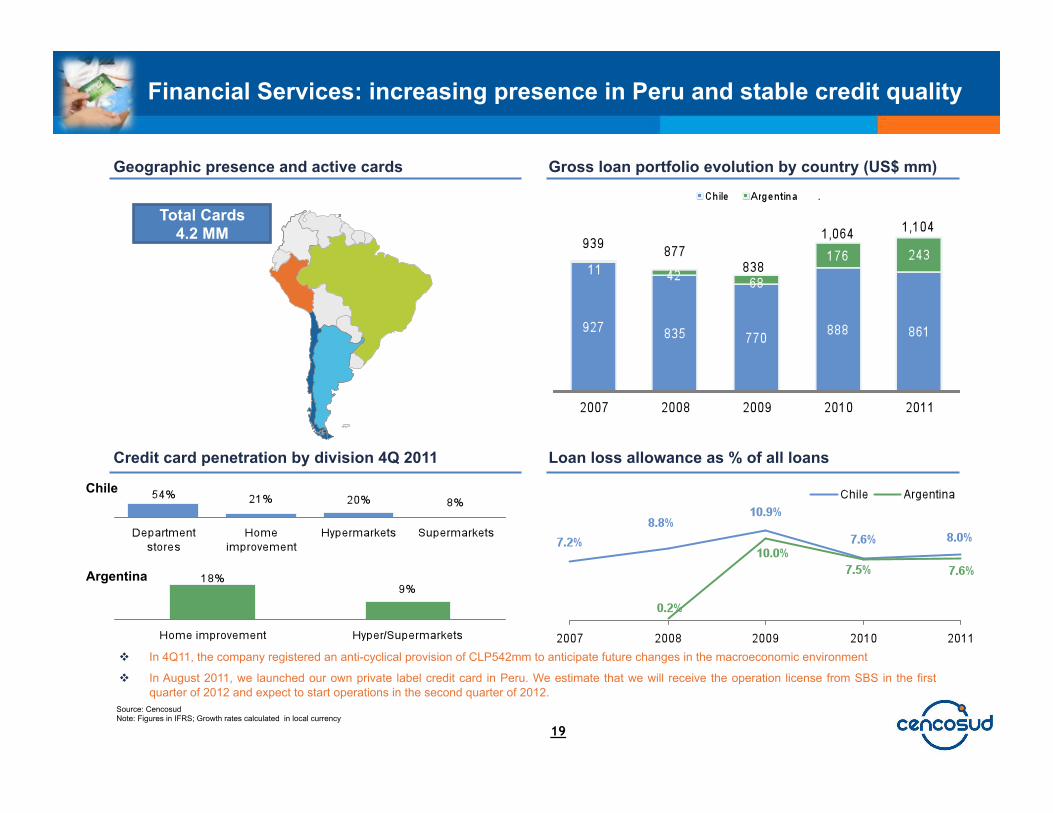

In 4Q11, the company registered an anti-cyclical provision of CLP542mm to anticipate future changes in the macroeconomic environment

In August 2011, we launched our own private label credit card in Peru. We estimate that we will receive the operation license from SBS in the first quarter of 2012 and expect to start operations in the second quarter of 2012.

Credit card penetration by division 4Q 2011

Source: Cencosud Note: Figures in IFRS; Growth rates calculated in local currency

Geographic presence and active cards

Total Cards 4.2 MM

Financial Services: increasing presence in Peru and stable credit quality

Loan loss allowance as % of all loans

Gross loan portfolio evolution by country (US$ mm)

19

Chile

Argentina

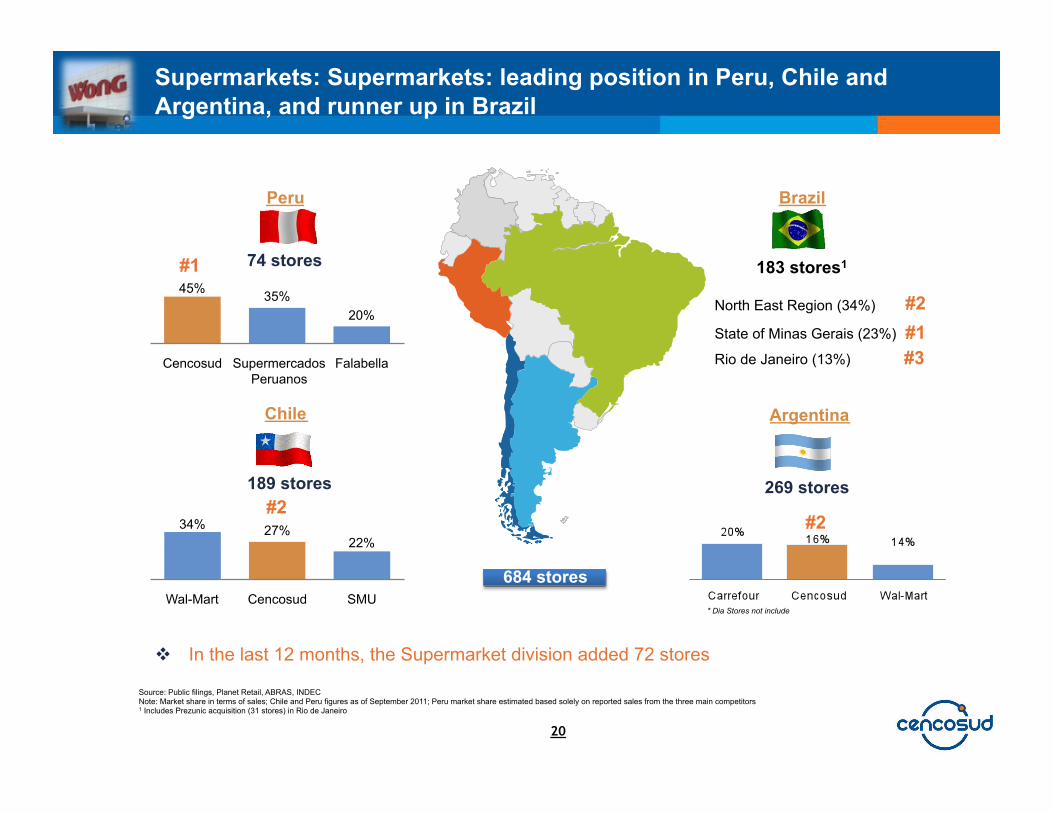

Source: Public filings, Planet Retail, ABRAS, INDEC Note: Market share in terms of sales; Chile and Peru figures as of September 2011; Peru market share estimated based solely on reported sales from the three main competitors 1 Includes Prezunic acquisition (31 stores) in Rio de Janeiro

269 stores

183 stores1

#2

North East Region (34%)

State of Minas Gerais (23%)

Rio de Janeiro (13%) #3

684 stores

74 stores #1

189 stores #2

* Dia Stores not include

#1

In the last 12 months, the Supermarket division added 72 stores

#2

Supermarkets: Supermarkets: leading position in Peru, Chile and Argentina, and runner up in Brazil

Peru

Chile

Brazil

Argentina

45% 35% 20%

Cencosud Supermercados Peruanos

Falabella

20

34% 27% 22%

Wal-Mart Cencosud SMU

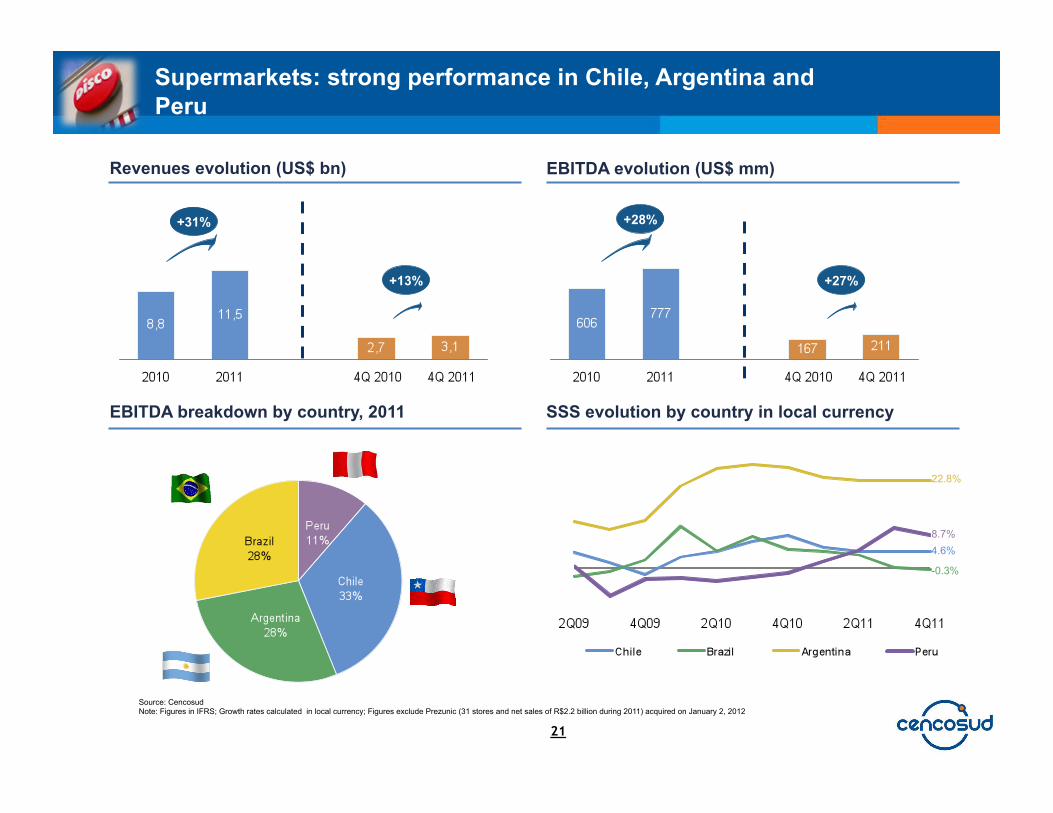

EBITDA breakdown by country, 2011

Revenues evolution (US$ bn) EBITDA evolution (US$ mm)

Source: Cencosud Note: Figures in IFRS; Growth rates calculated in local currency; Figures exclude Prezunic (31 stores and net sales of R$2.2 billion during 2011) acquired on January 2, 2012

SSS evolution by country in local currency

Supermarkets: strong performance in Chile, Argentina and Peru

21

+31%

+13% +27%

+28%

4.6%

-0.3%

8.7%

22.8%

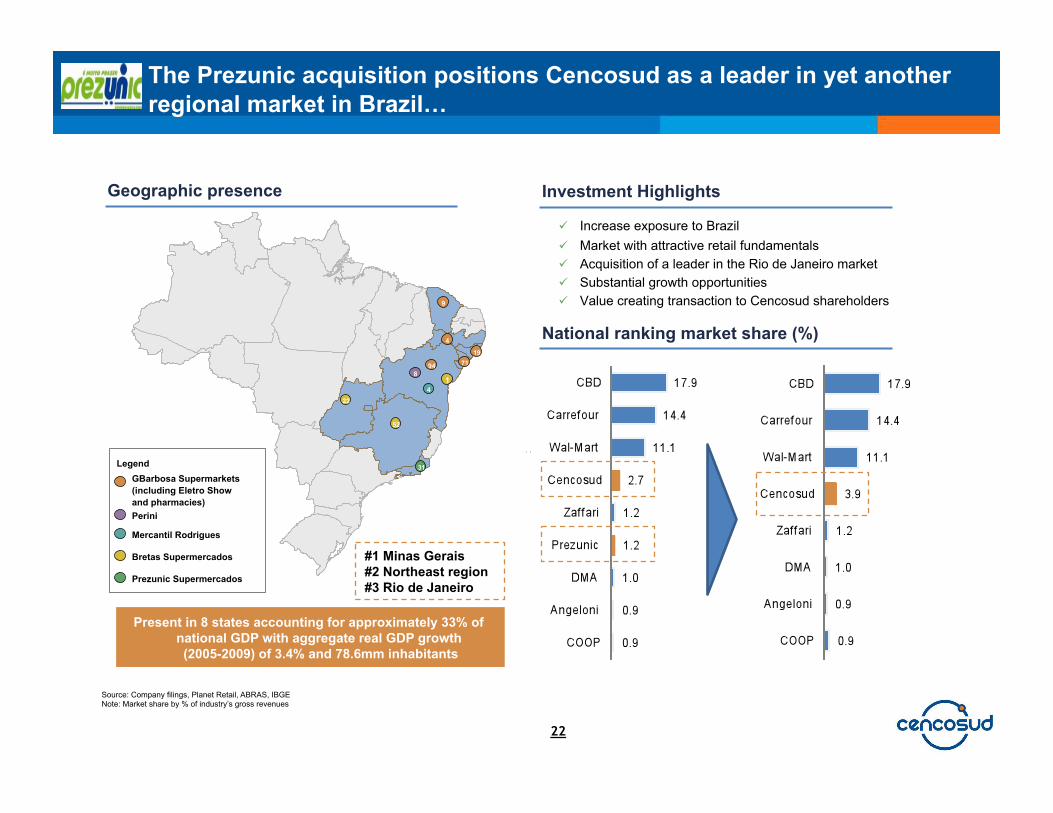

The Prezunic acquisition positions Cencosud as a leader in yet another regional market in Brazil…

Geographic presence

22

National ranking market share (%)

Source: Company filings, Planet Retail, ABRAS, IBGE Note: Market share by % of industry’s gross revenues

9

4

19

8 94

4 1

22

52

31

71

GBarbosa Supermarkets (including Eletro Show and pharmacies) Perini

Legend

Mercantil Rodrigues

Bretas Supermercados

Prezunic Supermercados

#1 Minas Gerais #2 Northeast region #3 Rio de Janeiro

Increase exposure to Brazil Market with attractive retail fundamentals Acquisition of a leader in the Rio de Janeiro market Substantial growth opportunities Value creating transaction to Cencosud shareholders

Investment Highlights

Present in 8 states accounting for approximately 33% of national GDP with aggregate real GDP growth (2005-2009) of 3.4% and 78.6mm inhabitants

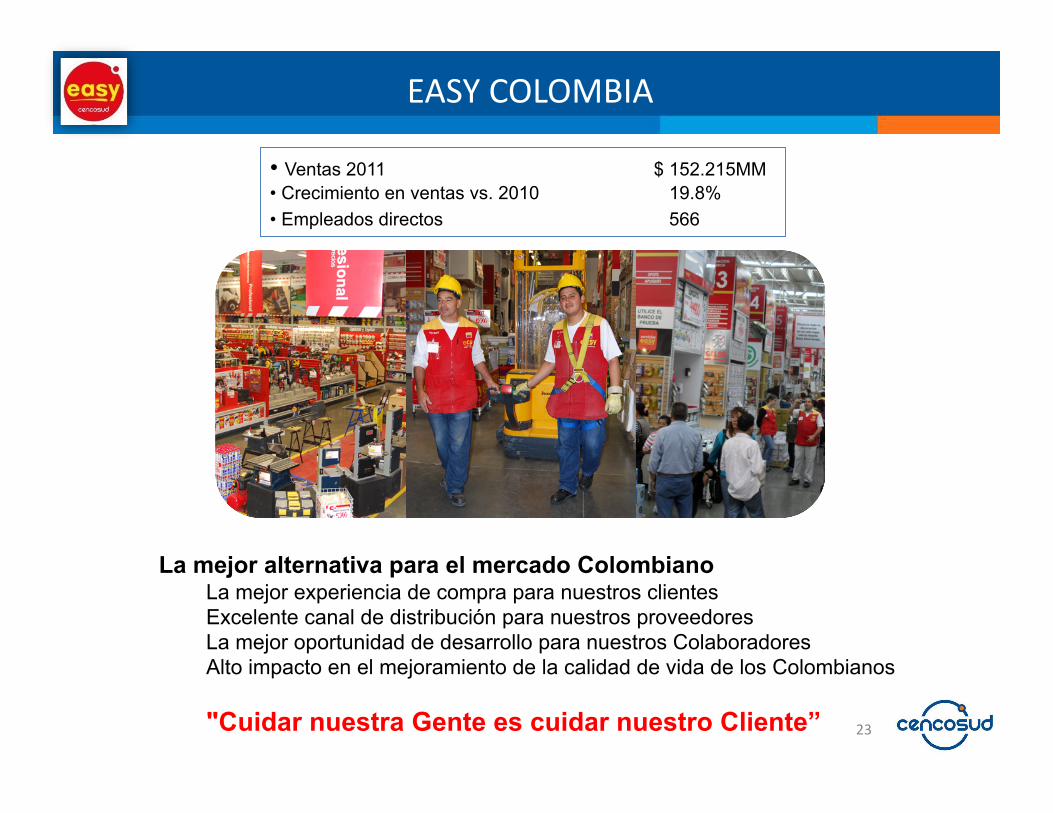

EASYCOLOMBIA

23

• Ventas 2011 $ 152.215MM • Crecimiento en ventas vs. 2010 19.8% • Empleados directos 566

La mejor alternativa para el mercado Colombiano La mejor experiencia de compra para nuestros clientes Excelente canal de distribución para nuestros proveedores La mejor oportunidad de desarrollo para nuestros Colaboradores Alto impacto en el mejoramiento de la calidad de vida de los Colombianos

"Cuidar nuestra Gente es cuidar nuestro Cliente”