illuminatel3c_solartaxequity_non-profit (1)

TRANSCRIPT

Non-Profits and Solar Tax Equity 101Most business owners nationwide don’t realize that they can benefit

from NGO Solar Tax Credits

Illuminate already has numerous non-profit organizations waiting to take advantage of Illuminate’s partners in energy efficiency and conservation technology as well as transition from fossil fuel energy to clean renewable (solar, wind, geothermal) energy. Illuminate L3C provides the necessary funding to: create a customized energy study to determine the facilities energy opportunity; fund the renewable energy solution while maximizing incentives (Federal, State and local). This provides the non-profit a no cost solution to putting a finite life on its utility expenses. The non-profit pays their utility bill to Illuminate until paid off then the solar system is donated to the non-profit.

Partnering with Illuminate L3C

The IRS has clearly defined who can benefit from these tax and depreciation benefits. It has limited the field of tax equity partners into two main categories: C-corporations and individuals with passive income and tax liability. The tax benefits from the solar partnership are generated from a passive activity, which can only be used to offset income from other passive activities. This means that the tax and depreciation credits cannot be used to offset active or investment income, but only passive income. Passive income is income from a business in which the taxpayer does not materially participate or net rental income. The tax and accounting rules are extremely complex. You should not proceed with any tax equity investment without consulting a qualified tax attorney and accountant.

Eligible Participants

Owners of renewable energy systems are able to benefit from federal and state incentives. Unfortunatly non-profit orga-nizations are unable to benefit from these incentives as most don’t have tax liability. However, business owners with tax liability can step in and assist the non-profits in monetizing these incentives. There are three main federal incentives that come from investing in renewable energy systesm that non-profits need partnering businesses: Federal Investment Tax Credit, Bonus Depreciation and Accelerated Depreciation.

These benefits have value because they reduce the amount of taxes a business would otherwise pay.

• Federal Investment Tax Credit: Owners of the renewable energy system can take a tax credit equal to 30% of the system basis.• Bonus Depreciation: Owners of the solar system are eligible to depreciate 50% of the basis in the first year.• Accelerated Depreciation: Businesses can depreciate the solar system using a 5 year schedule even though the useful life is 30-35 years

Solar Tax Equity

LEARN MORE For more information, contact: Will Overly at 785-760-6117 or email [email protected] ILLUMINATEL3C.COM

• Federal Investment Tax Credit: Owners of the renewable energy system can take a tax credit equal to 30% of the system basis.• Bonus Depreciation: Owners of the solar system are eligible to depreciate 50% of the basis in the first year.• Accelerated Depreciation: Businesses can depreciate the solar system using a 5 year schedule even though the useful life is 30-35 years

A low-profit limited liability company (L3C) is a legal form of business entity in the United States that was created to bridge the gap between non-profit and for-profit investing by providing a structure that facilitates investments in socially beneficial ventures. In line with of Illuminate’s driving social mission, a portion of the revenues are directed toward installing solar pv in develop-ing countries. Illuminate has partnered with inter-national NGOs to find eligible recipient candi-dates of micro-loans to educate, teach, train, local nationals to install solar pv systems. There are numerous tangible benefits including electric-ity, education, local jobs, community develop-ment, security, as well as opening the door for life giving opportunities.

Watt-to-Watt

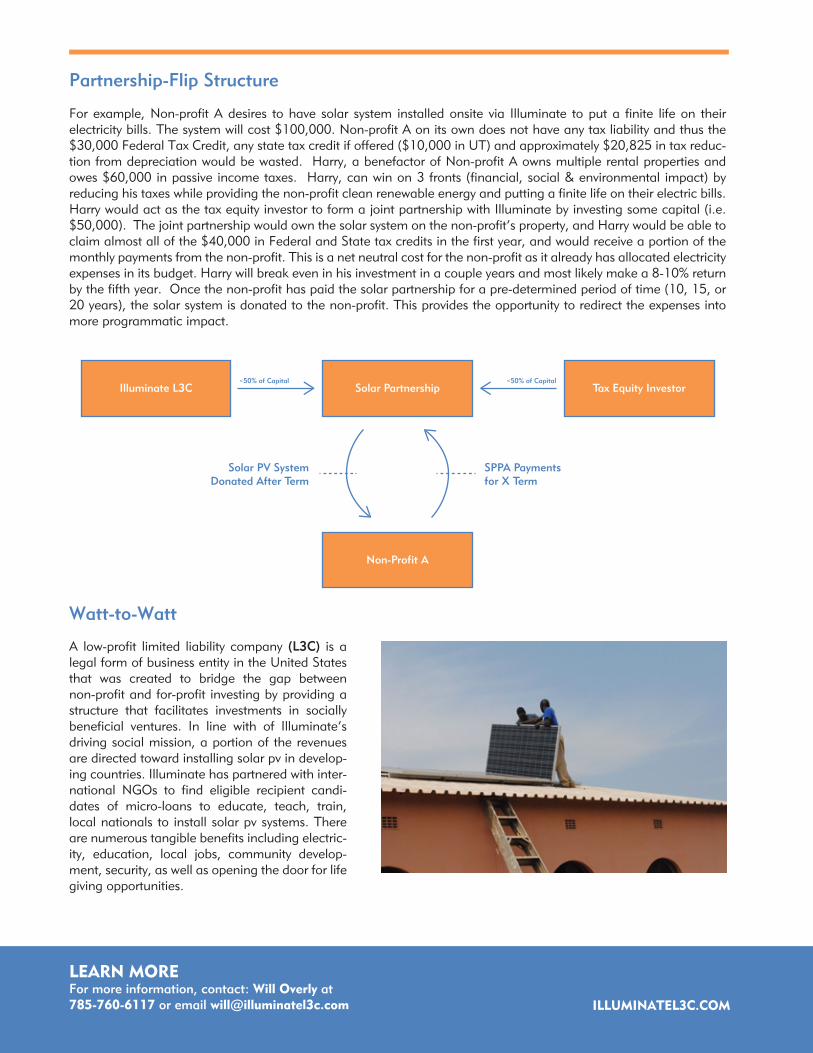

Partnership-Flip Structure

For example, Non-profit A desires to have solar system installed onsite via Illuminate to put a finite life on their electricity bills. The system will cost $100,000. Non-profit A on its own does not have any tax liability and thus the $30,000 Federal Tax Credit, any state tax credit if offered ($10,000 in UT) and approximately $20,825 in tax reduc-tion from depreciation would be wasted. Harry, a benefactor of Non-profit A owns multiple rental properties and owes $60,000 in passive income taxes. Harry, can win on 3 fronts (financial, social & environmental impact) by reducing his taxes while providing the non-profit clean renewable energy and putting a finite life on their electric bills. Harry would act as the tax equity investor to form a joint partnership with Illuminate by investing some capital (i.e. $50,000). The joint partnership would own the solar system on the non-profit’s property, and Harry would be able to claim almost all of the $40,000 in Federal and State tax credits in the first year, and would receive a portion of the monthly payments from the non-profit. This is a net neutral cost for the non-profit as it already has allocated electricity expenses in its budget. Harry will break even in his investment in a couple years and most likely make a 8-10% return by the fifth year. Once the non-profit has paid the solar partnership for a pre-determined period of time (10, 15, or 20 years), the solar system is donated to the non-profit. This provides the opportunity to redirect the expenses into more programmatic impact.

Illuminate L3C Solar Partnership

SPPA Payments for X Term

Solar PV SystemDonated After Term

<50% of Capital <50% of CapitalTax Equity Investor

Non-Profit A