2018pronicaragua.gob.ni/media/ckeditor/2018/01/26/doing-business-in... · general Álvaro baltodano...

TRANSCRIPT

Guía del Inversionista 2018

1

Guía del Inversionista 2018Doing Business in Nicaragua 2018

2 3

NICARAGUALaw firm of the year

8VO AÑO

nt cargo

Guía del Inversionista 2018Doing Business in Nicaragua 2018

4 5

I.

VI.

VII.

VIII.

II.

V.

III.

IV.

Perfil País / Country Profile

Derecho Laboral / Labor law

Obteniendo una residencia en Nicaragua /Obtaining a residency in Nicaragua

Recomendaciones para una inversión exitosa /Recommendations for a Successful Investment

Oportunidades de Inversión / Investment Opportunities

Sistema Fiscal / Fiscal System

Estableciendo una Empresa en Nicaragua / Set Up a Company in Nicaragua

La importación en Nicaragua / Imports in Nicaragua

Ventajas Competitivas / Competitive AdvantagesFácil Conectividad / Easy ConnectivityExcelente Desempeño Económico / Excellent Economic PerformanceTalento Abundante y Calificado / Abundant Human CapitalSólido Marco Legal / Solid Legal FrameworkGenerosos Incentivos Fiscales / Generous Fiscal IncentivesAltos Niveles de Seguridad / High Security LevelsCostos Laborales / Labor Costs

Residente con Contrato de Trabajo / Resident with Employment ContractResidente Empresario / Institutional ResidentResidente Trabajador Independiente / Independent ResidentResidente Retirado o Residente Rentista / Retiree ResidentPermiso de Trabajo / Work Permit

Manufactura Ligera / Light ManufacturingManufactura de Partes Automotrices / Manufacturing of Automotive ComponentsManufactura de Calzado / Footwear ManufacturingOtros Tipos de Manufactura / Other light manufacturing processesAgroindustria / AgribusinessProducción Agroexportable / Agro-Exportable ProductionProcesamiento de Alimentos / Food ProcessingPlantaciones Forestales / Forestry PlantationsProducción de Biocombustibles / Biofuels Production Externalización de Servicios / OutsourcingExternalización de Procesos de Conocimiento (KPO) / Knowledge Process Outsourcing (KPO)Externalización de Tecnologías de la Información (ITO) / Share Services CentersExternalización de Procesos de Negocios (BPO) / Business Process Outsourcing (BPO)Energía Renovable / Renewable EnergyMinas / Exploration and exploitation of minesTurismo / TourismContrataciones Administrativas del Estado / State Procurement and Contracting

Impuesto sobre la Renta / Income TaxImpuesto al Valor Agregado / Value Added TaxImpuesto Selectivo de Consumo / Selective Consumption TaxRégimen de Cuota Fija / Regime of Fixed FeeImpuesto de Bienes Inmuebles / Real Estate Tax Impuesto Municipal sobre Ingresos / Municipal Income TaxImpuesto de Matrícula / Municipal Registration Tax

consejo consultivo

general Álvaro Baltodano (Pronicaragua)Lic. orlando Solórzano Delgadillo (MIFIc)Ing. Álvaro rodríguez Zapata (aMcHaM)Lic. carlos Zarruk castillo (Pronicaragua) Lic. Erick Méndez Mejía (MIFIc)

coordinadores

Danilo antonio núñez Baltodano (MIFIc)Jeanette López r. (MIFIc)Margarita rojas (aMcHaM)Marielos gonzález (aMcHaM)avíl ramírez Valdivia (aMcHaM)Engelsberth gómez (Pronicaragua)Pablo Escorcia (Pronicaragua)norman amoretty (Pronicaragua)Juan carvajal (Pronicaragua)

Editores adjuntos

María asunción Moreno (central Law)claraliz oviedo (alvarado y asociados)róger Pérez (arias)rodrigo Ibarra (arias)Juan carlos cortez (Deloitte)Eduardo J. gutiérrez (Latinalliance) alonso Porras (Pacheco coto)Federico gurdián (garcía & Bodán)Blanca Buitrago (garcía & Bodán)Melvin Estrada (garcía & Bodán)Darina navarrete (garcía & Bodán)

Publicidad y Mercadeo

Marielos gonzález (aMcHaM)Paula Herrera (aMcHaM)

Diseño gráfico

carlos Balladares (Publideas)

Index

Contenido Index

Guía del Inversionista 2018Doing Business in Nicaragua 2018

6 7

Lic. Orlando SolórzanoMinister

Development, Industry and trade

Gral. Álvaro BaltodanoMinister - Presidential Delegate for

Investment Promotion and trade Facilitation

Ing. Roberto Sansón C.President

american chamber of commerce of nicaragua

Estimados inversionistas:

El Ministerio de Fomento, Industria y Comercio (MIFIC), la Agencia Oficial de Promoción de Inversiones del Gobierno de Nicaragua (PRONicaragua) y la Cámara de Comercio Americana de Nicaragua (AMCHAM), le invitan a conocer Nicaragua por medio de la presentación de la edición 2017 – 2018 de la Guía del Inversionista – Doing Business in Nicaragua, como uno de los países más cautivadores de Centroamérica para inversionistas que desean incrementar y optimizar sus operaciones.

Nicaragua, el país más grande de América Central, se ha destacado como un destino atractivo para la inversión, esto es dado por su favorable clima de negocios, su crecimiento económico sostenido como resultado del manejo disciplinado de sus políticas fiscales, financieras, monetarias y cambiarias, además de los esfuerzos que el Gobierno de Nicaragua, el sector privado e instituciones afines han realizado para mejorar diferentes políticas macroeconómicas. En el 2016, Nicaragua se consolidó como el país más seguro de Centroamérica, con la tasa de homicidio más baja de la región.

Además de ser un país con grandes oportunidades de negocios, Nicaragua también ofrece muchas facilidades para

Dear Investors:

The Ministry of Development, Industry and Trade (MIFIC, for its acronym in Spanish), the Official Investment Promotion Agency (PRONicaragua) and the American Chamber of Commerce of Nicaragua (AMCHAM), invite you to get to know Nicaragua, through the new edition of the Doing Business in Nicaragua 2017 – 2018 Investor Guideline, as one of the most captivating countries in Central America for investors that wish to optimize and increase their operations.

Nicaragua has become a country of international attraction; this is due to the favorable conditions offered to ease investment; the sustained economic growth that resulted from disciplined management of fiscal, financial and monetary policies; the constant efforts of the Nicaraguan Government, the private sector, and the help of related institutions that have worked on improving different macroeconomic policies. In 2016, Nicaragua consolidated itself as the safest country in Central America, with the lowest homicide rate in the region.

In addition to being a country with great business opportunities, Nicaragua also offers

los ejecutivos extranjeros, que gozan de un alto nivel de vida, lo que hace que se convierta en un destino perfecto para la inversión extranjera. Para el 2016, el PIB del país creció un 4.7 por ciento, alcanzando los US$13,230.1 millones. Igualmente, las exportaciones totales sumaron US$4,839.2 millones, y la inversión extranjera directa totalizó los US$1,442.0 millones.

El principal objetivo de esta guía, es presentarles los datos más actualizados del país, las ventajas competitivas, las oportunidades de inversión en sectores clave, sólido marco legal, incentivos para la inversión, además de información general relevante del país. Confiamos que la información sea de suma utilidad y los esperamos pronto en Nicaragua.

Manifestamos nuestro agradecimiento a todos los colaboradores y patrocinadores por hacer posible esta edición del Doing Business in Nicaragua 2017 – 2018, que confiamos será de gran utilidad para explorar las nuevas oportunidades de negocio e inversión que nuestro país ofrece.

Atentamente,

many facilities for foreign executives that like to enjoy high lifestyle levels, which makes it a perfect destiny for foreign investment. In 2016, GDP grew by 4.7 percent, reaching US$13.23 billion. Similarly, total exports accounted for US$4.84 billion, and the influx of foreign direct investment totaled US$1.44 billion.

The main objective of this guide is to present the country´s latest data, competitive advantage, investment opportunities in key sectors, solid legal framework, investment incentives, and general relevant information. We are confident that the information provided will be useful and we hope to see you in Nicaragua soon.

We thank all the contributors and sponsors for making possible this 2017 – 2018 edition of the Doing Business in Nicaragua – Investor’s Guide, which we trust will be useful to explore the new business and investment opportunities that our country offers.

Sincerely,

Lic. Orlando SolórzanoMinistro

MIFIc

Gral. Álvaro BaltodanoMinistro - Delegado Presidencial para la

Promoción de Inversiones

Ing. Álvaro Rodríguez ZapataPresidenteaMcHaM

Carta de Presentación Welcome Letter

Guía del Inversionista 2018Doing Business in Nicaragua 2018

8 9

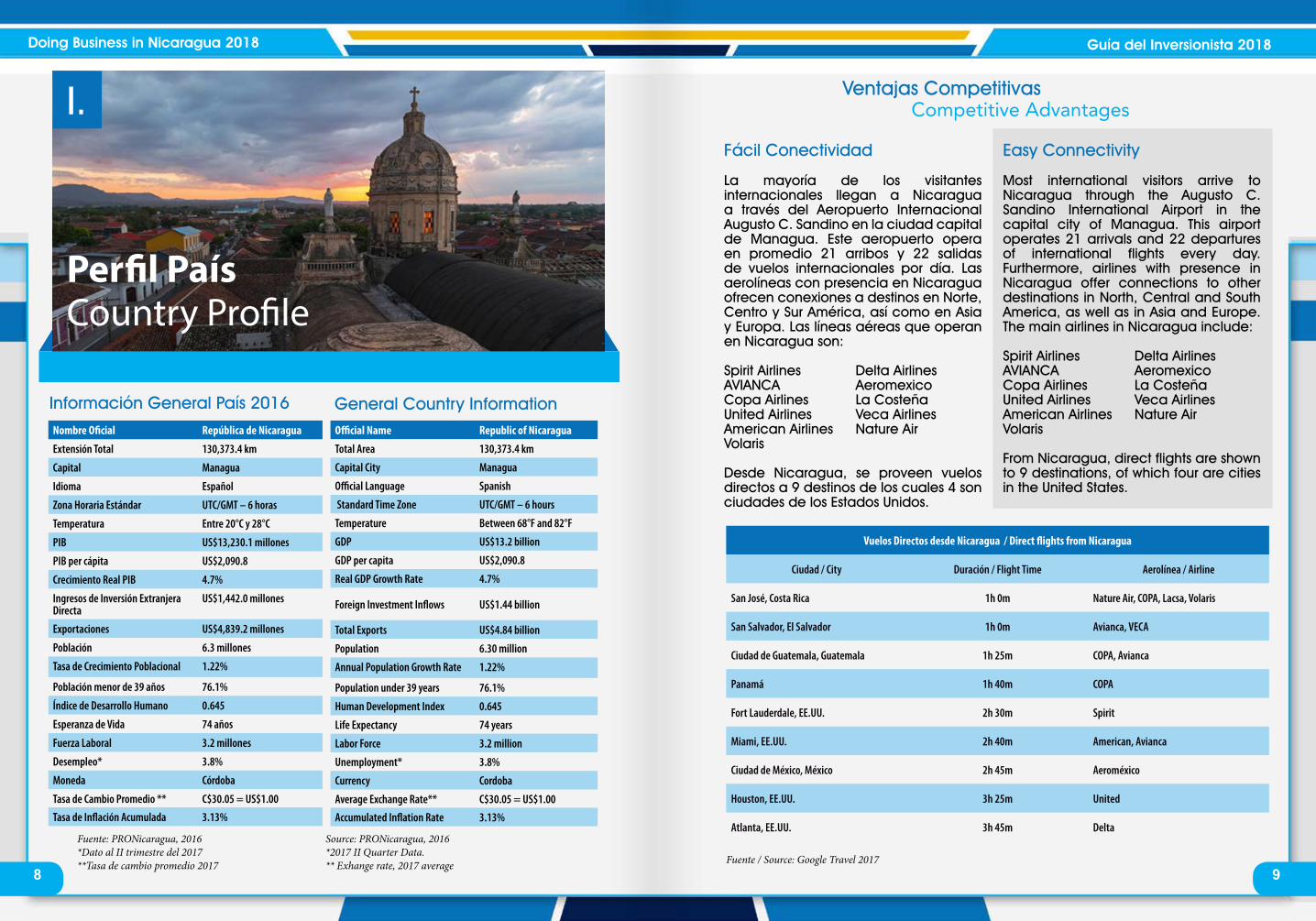

Fácil Conectividad

La mayoría de los visitantes internacionales llegan a Nicaragua a través del Aeropuerto Internacional Augusto C. Sandino en la ciudad capital de Managua. Este aeropuerto opera en promedio 21 arribos y 22 salidas de vuelos internacionales por día. Las aerolíneas con presencia en Nicaragua ofrecen conexiones a destinos en Norte, Centro y Sur América, así como en Asia y Europa. Las líneas aéreas que operan en Nicaragua son: Spirit Airlines Delta AirlinesAVIANCA AeromexicoCopa Airlines La CosteñaUnited Airlines Veca AirlinesAmerican Airlines Nature AirVolaris

Desde Nicaragua, se proveen vuelos directos a 9 destinos de los cuales 4 son ciudades de los Estados Unidos.

Ventajas CompetitivasCompetitive Advantages

Nombre Oficial República de Nicaragua

Extensión Total 130,373.4 km

Capital Managua

Idioma Español

Zona Horaria Estándar UTC/GMT – 6 horas

Temperatura Entre 20°C y 28°C

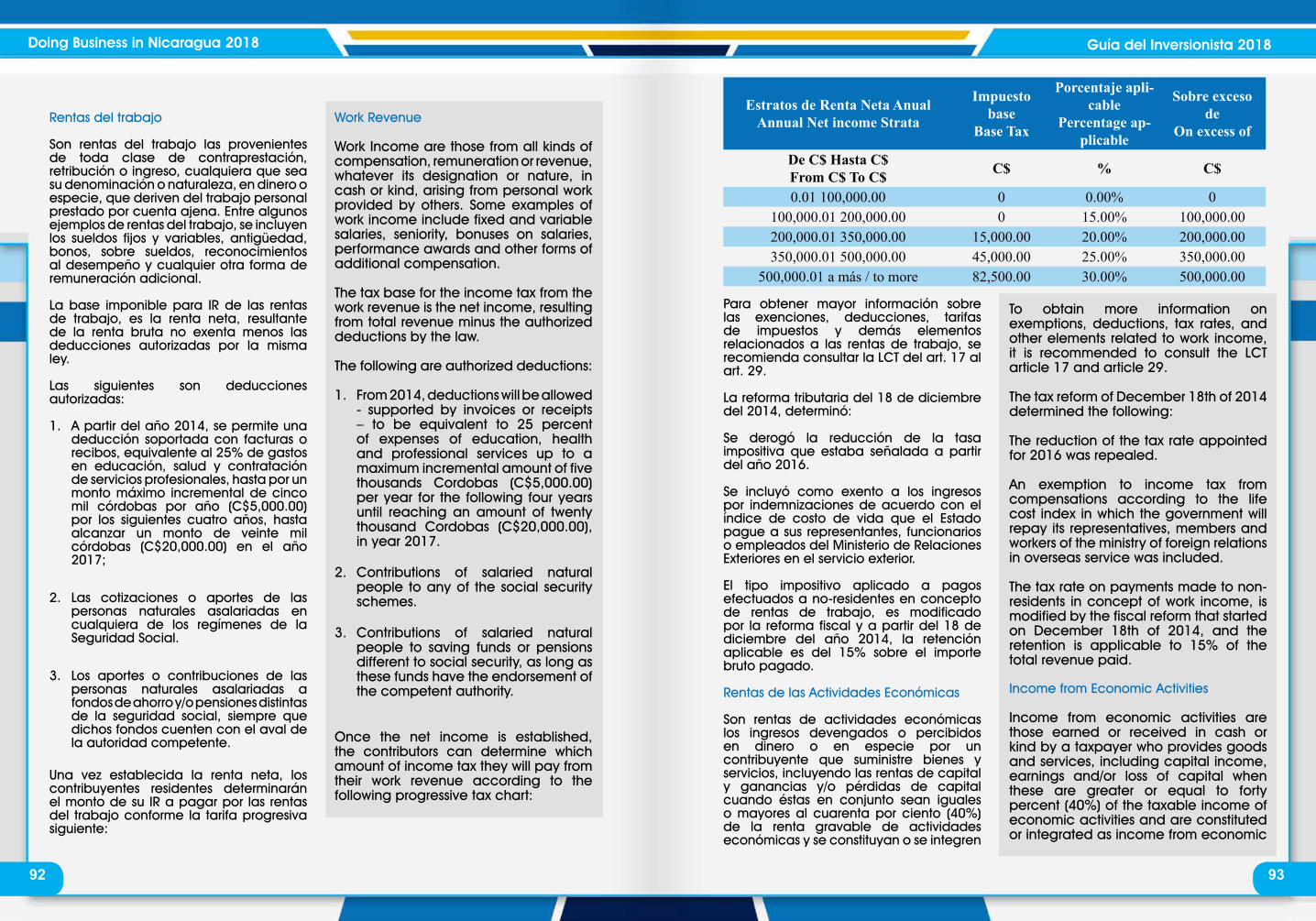

PIB US$13,230.1 millones

PIB per cápita US$2,090.8

Crecimiento Real PIB 4.7%

Ingresos de Inversión Extranjera Directa

US$1,442.0 millones

Exportaciones US$4,839.2 millones

Población 6.3 millones

Tasa de Crecimiento Poblacional 1.22%

Población menor de 39 años 76.1%

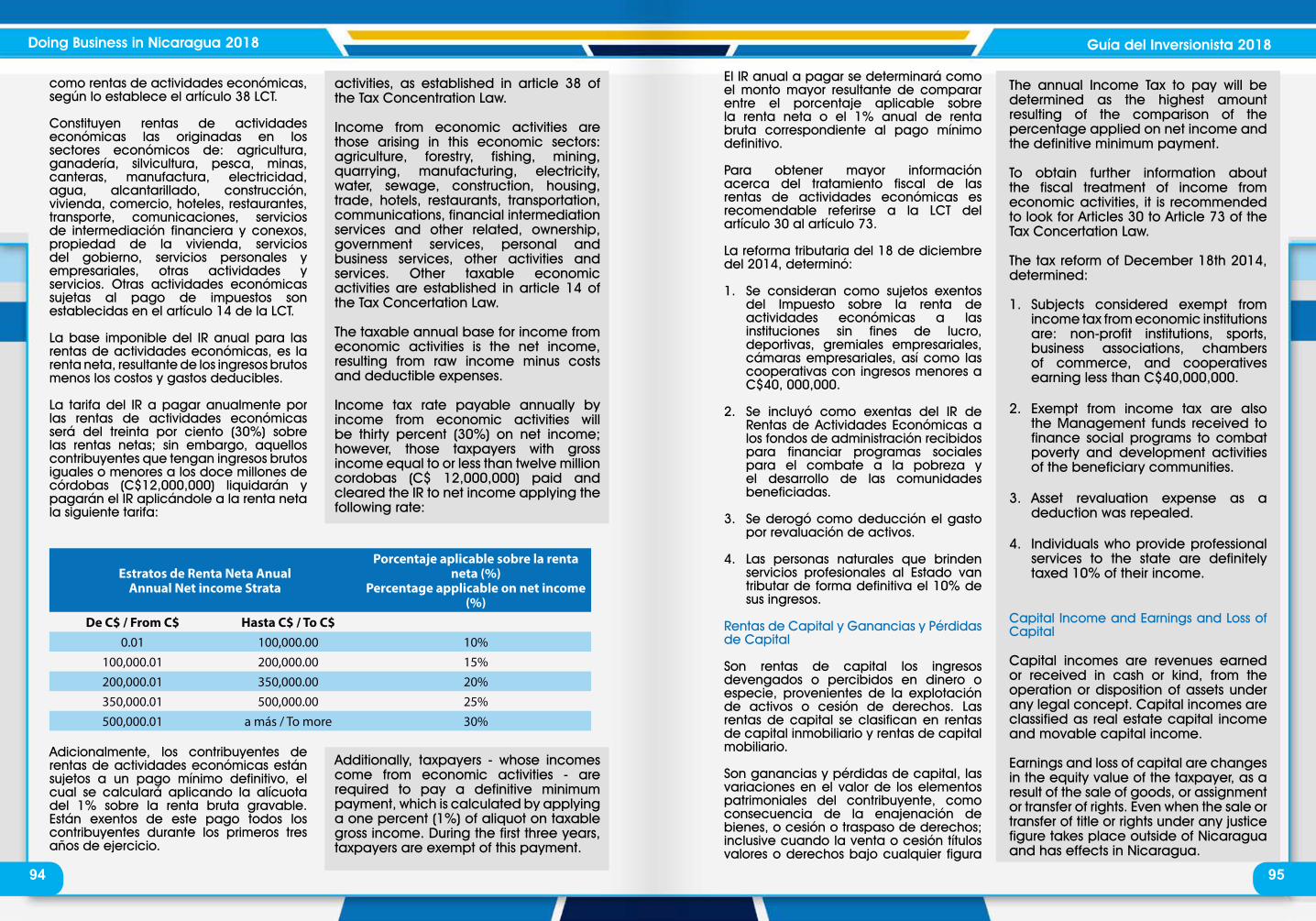

Índice de Desarrollo Humano 0.645

Esperanza de Vida 74 años

Fuerza Laboral 3.2 millones

Desempleo* 3.8%

Moneda Córdoba

Tasa de Cambio Promedio ** C$30.05 = US$1.00Tasa de Inflación Acumulada 3.13%

Official Name Republic of Nicaragua

Total Area 130,373.4 km

Capital City Managua

Official Language Spanish

Standard Time Zone UTC/GMT – 6 hours

Temperature Between 68°F and 82°F

GDP US$13.2 billion

GDP per capita US$2,090.8

Real GDP Growth Rate 4.7%

Foreign Investment Inflows US$1.44 billion

Total Exports US$4.84 billion

Population 6.30 million

Annual Population Growth Rate 1.22%

Population under 39 years 76.1%

Human Development Index 0.645

Life Expectancy 74 years

Labor Force 3.2 million

Unemployment* 3.8%

Currency Cordoba

Average Exchange Rate** C$30.05 = US$1.00Accumulated Inflation Rate 3.13%

Información General País 2016

Fuente: PRONicaragua, 2016*Dato al II trimestre del 2017**Tasa de cambio promedio 2017

Source: PRONicaragua, 2016*2017 II Quarter Data.** Exhange rate, 2017 average

Perfil Paíscountry Profile

I.

Vuelos Directos desde Nicaragua / Direct flights from Nicaragua

Ciudad / City Duración / Flight Time Aerolínea / Airline

San José, Costa Rica 1h 0m Nature Air, COPA, Lacsa, Volaris

San Salvador, El Salvador 1h 0m Avianca, VECA

Ciudad de Guatemala, Guatemala 1h 25m COPA, Avianca

Panamá 1h 40m COPA

Fort Lauderdale, EE.UU. 2h 30m Spirit

Miami, EE.UU. 2h 40m American, Avianca

Ciudad de México, México 2h 45m Aeroméxico

Houston, EE.UU. 3h 25m United

Atlanta, EE.UU. 3h 45m Delta

Fuente / Source: Google Travel 2017

Easy Connectivity

Most international visitors arrive to Nicaragua through the Augusto C. Sandino International Airport in the capital city of Managua. This airport operates 21 arrivals and 22 departures of international flights every day. Furthermore, airlines with presence in Nicaragua offer connections to other destinations in North, Central and South America, as well as in Asia and Europe. The main airlines in Nicaragua include:

Spirit Airlines Delta AirlinesAVIANCA AeromexicoCopa Airlines La CosteñaUnited Airlines Veca AirlinesAmerican Airlines Nature AirVolaris

From Nicaragua, direct flights are shown to 9 destinations, of which four are cities in the United States.

General Country Information

Guía del Inversionista 2018Doing Business in Nicaragua 2018

10 11

Excelente Desempeño Económico

Nicaragua ha experimentado un crecimiento económico sostenido como resultado del manejo disciplinado de sus políticas fiscales, financieras, monetarias y cambiarias. La legislación y procedimientos administrativos pro negocios han contribuido a un fuerte ingreso de inversión extranjera en los últimos años.

Producto Interno Bruto

En el 2016, Nicaragua alcanzó un producto interno bruto (PIB) de US$13,230.1 millones, lo cual representó un crecimiento del 4.7 por ciento en relación al 2015. A su vez, el PIB per cápita ascendió a US$2,090.8.

Las actividades económicas que comprendieron el PIB de Nicaragua en el 2016 fueron:

Actividad EconómicaEconomic Activity

Relación al PIB 2016% of GDP 2016

Comercio, hoteles y restaurantesTrade, hotels and restaurants 14.61%

Industrias manufacturerasManufacturing 14.23%

Agricultura, ganadería, silvicultura y pescaAgriculture, forestry and fishing 13.71%

Impuestos netosNet taxes 10.13%

Otros serviciosOther services 10.11%

Transporte y comunicacionesTransport and communication 8.32%

Propiedad de viviendaHousing 6.60%

Fuente: Banco Central de Nicaragua

Actividad EconómicaEconomic Activity

Relación al PIB 2016% of GDP 2016

Administración pública y defensaGeneral government services 5.78%

EducaciónEducation 3.82%

Servicios de intermediación financieraFinancial intermediation services 3.80%

ConstrucciónConstruction 2.90%

Electricidad, agua y alcantarilladoElectricity, gas and water supply 2.33%

SaludHealth 2.19%

Explotación de minas y canterasMining and quarrying 1.47%

Source: Central Bank of Nicaragua.

Excellent Economic Performance

Nicaragua has experienced sustained economic growth as a result of the disciplined management of its fiscal, financial, monetary and exchange policies. Pro-business legislations and administrative procedures have contributed to a strong inflow of foreign investment in recent years.

Gross Domestic Product

In 2016, Nicaragua reached a gross domestic product (GDP) of US$13.23 billion, which represents a growth of 4.7 percent in relation to 2015. In turn, GDP per capita reached US$2,090.8.

The top sectors that composed the GDP of Nicaragua in 2016 were:

Guía del Inversionista 2018Doing Business in Nicaragua 2018

12 13

Durante los últimos cinco años, el PIB se ha comportado de la siguiente manera:

2012 2013 2014 2015 2016

PIB (US$ Millones)gDP (US$ Million) 10,532 10,983 11,880 12,748 13,230

crecimiento PIBgDP real growth 6.5% 4.9% 4.8% 4.9% 4.7%

Fuente: Banco Central de Nicaragua.

Este alto crecimiento ha sido impulsado por la estabilidad social y económica de los últimos 5 años y por un buen manejo gubernamental durante el periodo.

Exportaciones

En 2016, las exportaciones totales de Nicaragua alcanzaron la cifra total de US$4,839.2 millones. Adicionalmente, la cifra de exportaciones ha mostrado una tasa de crecimiento compuesto anual de 8 por ciento durante el periodo 2007 – 2016.

Fuente: Banco Central de Nicaragua (BCN).

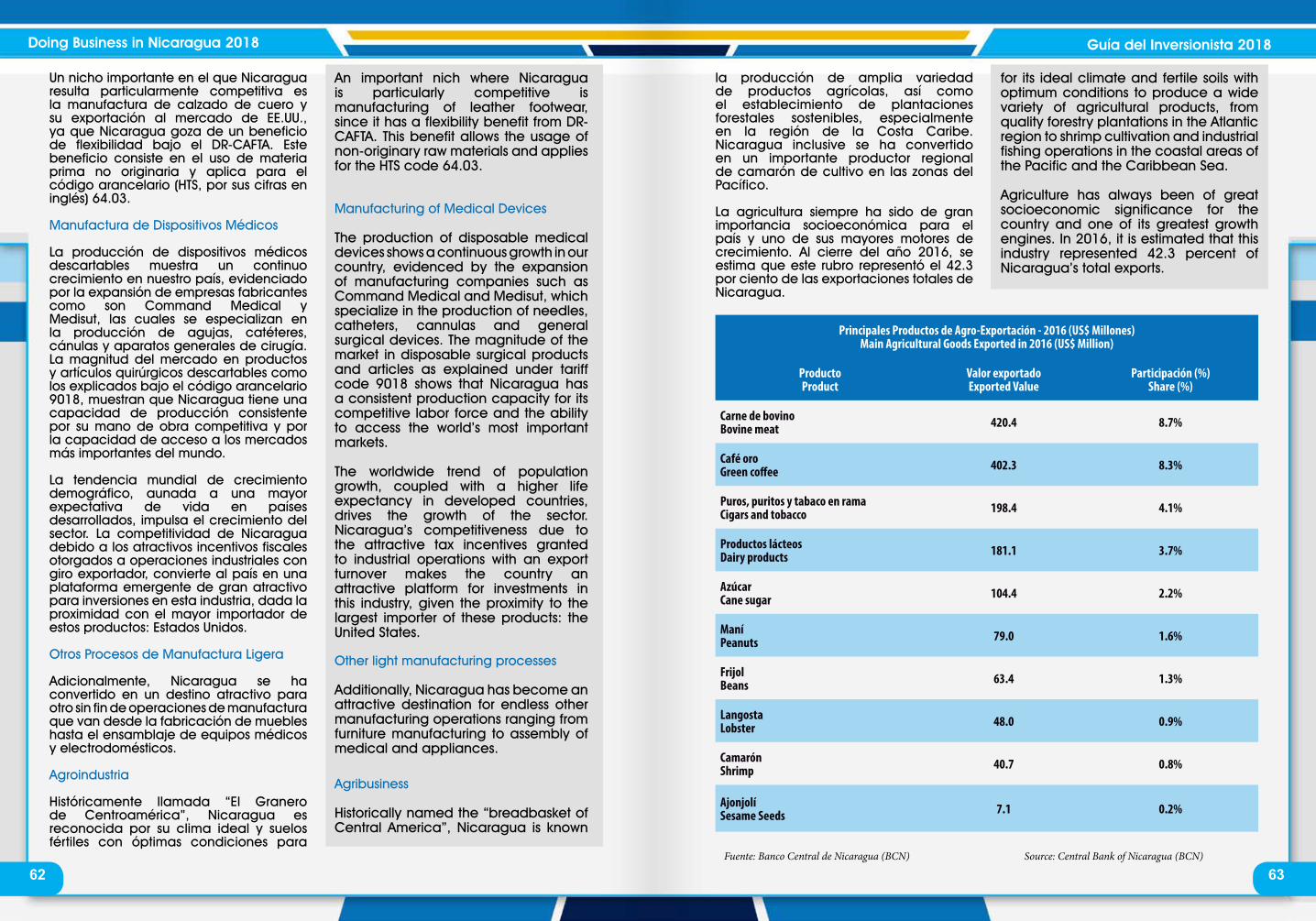

Los 10 principales productos de exportación de Nicaragua para el 2016 fueron: textil y confección (31.6%); arneses automotrices (13.7%), carne de bovino (8.7%), café (8.3%), oro (7.4%), puros y tabaco (4.1%), lácteos (3.7%), azúcar (2.2%), maní (1.6%), y frijoles (1.3%).

Ingresos de Inversión Extranjera Directa

Para el 2016, se estima que los ingresos de inversión extranjera directa alcancen los US$1,442 millones, lo cual representa un aumento del 4.1 por ciento comparado con el 2015. Los ingresos de IED hacia Nicaragua registraron una tasa de crecimiento promedio anual de 16 por ciento durante el periodo 2007-2016. Estos resultados reflejan la existencia de un clima de estabilidad y seguridad, respaldado por un marco legal para las inversiones.

Los cinco principales destinos de la inversión por sector económico fueron Industria (36%), Telecomunicaciones (18%), Comercio y Servicios (13%), Financiero (13%), y Energía (11%), los cuales comprendieron el 91 por ciento del total de los ingresos de inversión extranjera directa en el 2016.

GDP during the last five years has behaved as follows:

Source: Central Bank of Nicaragua.

This higher growth was driven by economic and social stability in recent 5 years and as a result of good government management.

Exports

In 2016, total exports of Nicaragua reached US$4.84 billion. In addition, total exports have shown a compound annual growth rate of 8 percent during the period 2007 – 2016.

Source: Central Bank of Nicaragua (BCN).

The top 10 export products of 2016 were textile and apparel (31.6%), automotive harnesses (13.7%), bovine meat (8.7%), coffee (8.3%), gold (7.4%), cigars and tobacco (4.1%), dairy products (3.7%), sugar (2.2%), peanut (1.6%), and beans (1.3%).

Foreign Direct Investment

Foreign Direct Investment Inflows in Nicaragua are estimated at US$1.44 billion for 2016. Nicaragua’s FDI Inflows registered a compound annual growth rate of 16 percent between 2007 and 2016; that supports the country’s secure and stable business climate and solid legal framework.

The top five sectors were Industry (36%), Telecommunications (18%), Commerce and Services (13%), Financial (13%), and Energy (11%), which comprised 91 percent of total foreign direct investment inflows in 2016.

Fuente: MIFIC, BCN y PRONicaragua Source: MIFIC, BCN and PRONicaragua.

Ingresos de Inversión Extranjera DirectaTasa de crecimiento compuesto anual 16%

Mill

one

s US

$ M

illio

ns U

S$

Foreign Direct Investment Inflows16% compound annual growth rate

Exportaciones TotalesTasa de crecimiento compuesta anual 8%

Total Exports8% compound annual growth rate

Mill

one

s US

$ M

illio

ns U

S$

Guía del Inversionista 2018Doing Business in Nicaragua 2018

14 15

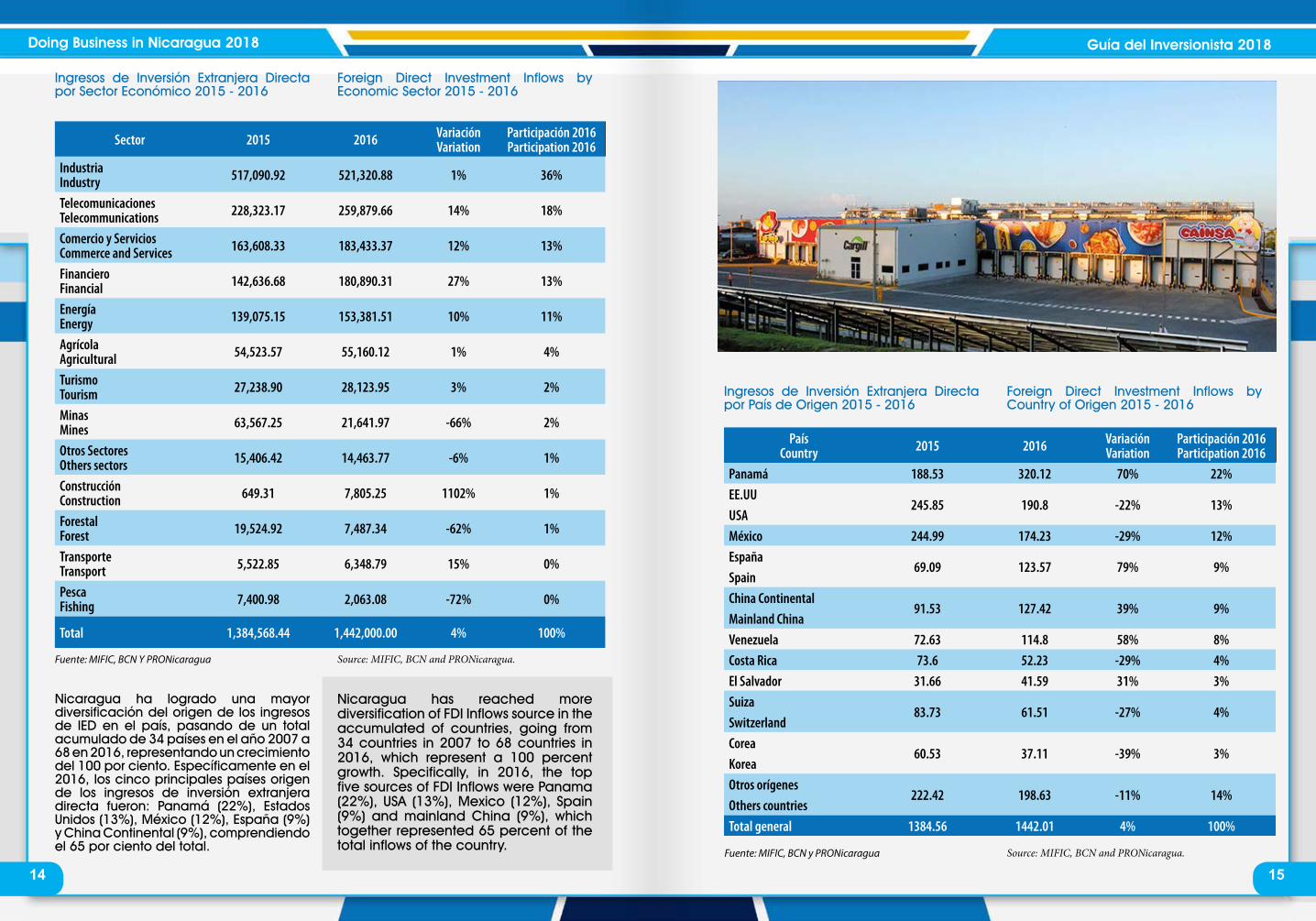

Ingresos de Inversión Extranjera Directa por Sector Económico 2015 - 2016

Sector 2015 2016 VariaciónVariation

Participación 2016Participation 2016

IndustriaIndustry 517,090.92 521,320.88 1% 36%

TelecomunicacionesTelecommunications 228,323.17 259,879.66 14% 18%

Comercio y ServiciosCommerce and Services 163,608.33 183,433.37 12% 13%

FinancieroFinancial 142,636.68 180,890.31 27% 13%

EnergíaEnergy 139,075.15 153,381.51 10% 11%

AgrícolaAgricultural 54,523.57 55,160.12 1% 4%

TurismoTourism 27,238.90 28,123.95 3% 2%

MinasMines 63,567.25 21,641.97 -66% 2%

Otros SectoresOthers sectors 15,406.42 14,463.77 -6% 1%

ConstrucciónConstruction 649.31 7,805.25 1102% 1%

ForestalForest 19,524.92 7,487.34 -62% 1%

TransporteTransport 5,522.85 6,348.79 15% 0%

PescaFishing 7,400.98 2,063.08 -72% 0%

Total 1,384,568.44 1,442,000.00 4% 100%

Nicaragua ha logrado una mayor diversificación del origen de los ingresos de IED en el país, pasando de un total acumulado de 34 países en el año 2007 a 68 en 2016, representando un crecimiento del 100 por ciento. Específicamente en el 2016, los cinco principales países origen de los ingresos de inversión extranjera directa fueron: Panamá (22%), Estados Unidos (13%), México (12%), España (9%) y China Continental (9%), comprendiendo el 65 por ciento del total.

Ingresos de Inversión Extranjera Directa por País de Origen 2015 - 2016

PaísCountry 2015 2016 Variación

VariationParticipación 2016Participation 2016

Panamá 188.53 320.12 70% 22%EE.UUUSA

245.85 190.8 -22% 13%

México 244.99 174.23 -29% 12%EspañaSpain

69.09 123.57 79% 9%

China ContinentalMainland China

91.53 127.42 39% 9%

Venezuela 72.63 114.8 58% 8%Costa Rica 73.6 52.23 -29% 4%El Salvador 31.66 41.59 31% 3%SuizaSwitzerland

83.73 61.51 -27% 4%

CoreaKorea

60.53 37.11 -39% 3%

Otros orígenesOthers countries

222.42 198.63 -11% 14%

Total general 1384.56 1442.01 4% 100%

Foreign Direct Investment Inflows by Economic Sector 2015 - 2016

Fuente: MIFIC, BCN Y PRONicaragua

Fuente: MIFIC, BCN y PRONicaragua

Nicaragua has reached more diversification of FDI Inflows source in the accumulated of countries, going from 34 countries in 2007 to 68 countries in 2016, which represent a 100 percent growth. Specifically, in 2016, the top five sources of FDI Inflows were Panama (22%), USA (13%), Mexico (12%), Spain (9%) and mainland China (9%), which together represented 65 percent of the total inflows of the country.

Source: MIFIC, BCN and PRONicaragua.

Source: MIFIC, BCN and PRONicaragua.

Foreign Direct Investment Inflows by Country of Origen 2015 - 2016

Guía del Inversionista 2018Doing Business in Nicaragua 2018

16 17

Talento Abundante y Calificado

Educación

El Gobierno de Nicaragua cree firmemente que la educación es la base del desarrollo económico de un país, por lo que asigna una cantidad significativa del presupuesto nacional para invertir en la educación primaria, secundaria y superior. Los gastos de educación incluyendo las universidades públicas, ascienden aproximadamente al 22% del presupuesto total del Gobierno.

Educación Superior y Técnica

En el país, había 50 universidades reconocidas por el Consejo Nacional de Universidades (CNU) para el año 2016, en donde 48 de ellas cuentan con aproximadamente 175,405 estudiantes inscritos, de acuerdo con un estudio independiente llevado a cabo por PRONicaragua. Además, el país posee una universidad acreditada en los Estados Unidos de América y tres programas universitarios bilingües.

Para el 2016, de los 175,405 estudiantes inscritos en universidades establecidas por el CNU, había unos 48,508 estudiantes inscritos en el área de economía y negocios, más de 41,250 en áreas de ingeniería y arquitectura, más de 13,940 en áreas de ciencias políticas y jurídicas, más de 20,947 en el área de ciencias médicas, más de 12,130 en el área agropecuaria y más de 39,410 en otras áreas de estudio.

INCAE Business School, prestigioso instituto regional de negocios afiliado a la Universidad de Harvard, se encuentra localizado en las afueras de Managua (Campus Francisco de Sola). Dicho instituto se cataloga como número uno en toda América Latina y entrena a expertos en gerencia internacional listos para ofrecer sus servicios.

Habilidades en inglés

Aunque el idioma oficial de Nicaragua es el español, el inglés es cada vez más popular. Las instituciones educativas privadas y públicas han comenzado a proveer muchas más clases en inglés

Abundant Human Capital

Education

The Nicaraguan Government firmly believes that education is the foundation of a country’s economic development, and has thus allocated a significant amount of the national budget to invest in primary, secondary and higher education. Education expenditures, including public Universities, amount to approximately 22 percent of the GDP.

Higher and Technical Education

In the country, there were 50 higher education institutions recognized by the National Council of universities (CNU, for its Spanish acronym) by 2016, which 48 of them has an estimated total enrollment of over 175,405 students, according to an independent study carried out by PRONicaragua. Additionally, there is a university certified by the United States of America and three bilingual university programs.

By 2016, out of the 175,405 students enrolled in the already stablished universities by the National Council of universities, there were 48,508 students enrolled in the areas of business and economics, more than 41,251 in engineering and architecture, more than 13,940 in the areas of politics and law, more than 20,158 in medicinal sciences, more than 12,131 in agriculture, and more than 39,410 in other areas of studies.

INCAE Business School, a prestigious regional business school affiliated with Harvard University, is located on the out skirts of Managua. The institute is ranked as number one in Latin America and trains experts in international management, ready to offer its services to world-class companies.

English Skills

Although the official language of Nicaragua is Spanish, English is increasingly popular. Public and private academic institutions have started to provide more

ABOGADOS / ATTORNEYS-AT-LAW

Fernando P. Midence-Mantilla - Managing Partner Nicaragua+505-2223-1017 | [email protected]

www.lexincorp.com

Central American Law Firm of the Year

When good service is recognized

Guía del Inversionista 2018Doing Business in Nicaragua 2018

18 19

dada la gran demanda del idioma. Se ha hecho evidente el gran valor agregado que el idioma inglés provee en el ámbito laboral, por lo que el número de cursos ha aumentado en academias privadas. Además, La demanda del inglés ha crecido en el mercado laboral de servicios externalizados para estudiantes egresados con esta importante habilidad.

De acuerdo con un estudio realizado por PRONicaragua sobre el número de personas que habla inglés y español, se pudo determinar que el interés de los nicaragüenses en tener el inglés como segunda lengua está creciendo rápidamente. Los resultados del estudio muestran que, en el 2016, había más de 22,558 estudiantes aprendiendo inglés en centros de idiomas públicos y privados; además más 4,844 estudiantes egresaron con éxito del programa de estudio. Entre los ya egresados se encuentran 319 estudiantes de escuelas bilingües, 3,157 estudiantes de centros de idiomas y 1,387 estudiantes de universidades nacionales.

Fuerza Laboral

La población de Nicaragua se caracteriza por ser flexible, con buenos hábitos laborales, con una curva de aprendizaje rápida y bajas tasas de absentismo y rotación. Estas cualificaciones han permitido que Nicaragua se posicione como una de las más competitivas y productivas de la región en términos de capital humano. De acuerdo con cifras de Banco Central de Nicaragua, la fuerza laboral del país se sitúa en 3.2 millones.

Según estadísticas del Instituto Nicaragüense de Seguridad Social (INSS), el número de asegurados activos afiliados, ha incrementado sustancialmente en los últimos años, pasando de 471,856 en el 2007 a 857,219 en el 2016; lo cual representa un incremento del 81.6 por ciento.

Acceso Preferencial a Mercados Internacionales

Nicaragua otorga preferencias arancelarias en virtud de los Tratados de Libre Comercio y Acuerdos que ha suscrito de forma bilateral, regional o como parte del Mercado Común Centroamericano, (MCCA), cuyo objetivo

es estimular la expansión y diversificación del comercio entre las partes; eliminar los obstáculos al comercio y facilitar la circulación transfronteriza de mercancías; promover condiciones de competencia leal; y aumentar sustancialmente las oportunidades de inversión, entre otros beneficios.

Tratados Países

Tratados de Libre ComercioFree Trade Agreements

EE.UU., México, Panamá, China Taiwán, República Dominica-na, Chile y Unión Europea.

U.S.A., Mexico, Panama, Taiwan, Dominican Republic, Chile, and European Union.

Mercado Común CentroamericanoCentral America Common Market

Nicaragua, Guatemala, El Salvador, Honduras, Costa Rica y Panamá. Adicionalmente, libre movilidad de capital, servicios y recursos humanos entre los países CA-4.

Nicaragua, Guatemala, El Salvador, Honduras, Costa Rica and Panana. Additionally, free movements of capital, services and human resources between the CA-4 countries.

Sistema Generalizado de PreferenciasGeneralized System of Preference

Japón (SGP), Noruega (SGP), Canadá (SGP), Federación de Ru-sia (SGP) y Suiza (SGP).

Japan (SGP), Norway (SGP), Canada (SGP), Russian Federation (SGP), and Switzerland (SGP).

Acuerdo de Alcance Parcial Partial Scope Agreement Ecuador, Cuba, Venezuela, Colombia.

Acuerdos en Negociación

Acuerdo de Libre Comercio en Proceso de Ratificación

Free Trade Agreement in Ratification Process

República de Corea del Sur.South Korea

Alianza Bolivariana para los Pueblos de Nuestra América (ALBA)

Bolivarian Alliance for the Peoples of Ours America (ALBA)

Venezuela, Ecuador, Bolivia, Cuba, Antigua & Barbuda, Domi-nica & St. Vicente y Granadinas.

Venezuela, Ecuador, Bolivia, Cuba, Antigua and Barbuda, Dominica, Saint Vincent and the Grenadines.

Asociación Latinoamericana de Integración (ALADI)

Latin American Integration Association (LAIA)

Argentina, Bolivia, Brasil, Chile, Colombia, Ecuador, México, Paraguay, Perú, Uruguay, Venezuela, Cuba.

classes in English, given the high demand of this language. It has become evident the great benefit that the English language provides in the workplace, reason why the number of courses has increased in private academies. In addition, demand for English has grown in the outsourced services labor market for students graduating with this important skill.

According to a study carried out by PRONicaragua about the Spanish and English speaking population, the interest of the Nicaraguan population in speaking English as a second language is growing fast. The results of the study showed that in 2016, there were almost 22,558 students learning English in public and private language centers; furthermore, almost 4,844 students successfully completed the study program. In addition to the population in public and private language centers, there were 319 students enrolled in bilingual secondary schools, 3,157 students from language centers and 1,387 students from national universities.

Workforce

Nicaragua’s population is characterized as flexible, with good work habits, fast learners and low rates of absenteeism and turn over. This has allowed Nicaragua to be one of the most competitive and productive nations of the region in terms of human capital. According to the Nicaragua Central Bank figures, the country’s labor force is stood in 3.2 million.

According to the Social Security Institute of Nicaragua (INSS for its Spanish acronym), the number of active insured members before INSS has increased substantially in recent years, from 471,856 in 2007 to 857,219 in 2016, an increase of 81.6 percent.

Preferential Access to International Markets

Nicaragua grants tariff preferences under Free Trade Agreements and bilateral, regional or part of the Central America Common Market (CACM)

signed agreements its objectives are to encourage expansion and diversification of trade between the parties; to eliminate trade barriers and to facilitate the cross-border movement of goods; to promote fair competition conditions; and substantially increase investment opportunities, among other benefits.

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Source: Ministry of Development, Industry and Trade (MIFIC)

Guía del Inversionista 2018Doing Business in Nicaragua 2018

20 21

Sistema de Integración Económica Centroamericana

El Tratado General de Integración Económica Centroamericana, suscrito el 13 de diciembre de 1960, entre Nicaragua, Guatemala, El Salvador, Honduras y Costa Rica con el objetivo de establecer entre ellos un Mercado Común Centroamericano (MCCA), comprometiéndose a perfeccionar una zona de Libre Comercio, la adopción de un arancel externo común, y constituir una Unión Aduanera entre sus territorios. El 29 de junio del 2012, Panamá suscribe el Protocolo de Incorporación al Subsistema de Integración Económica Centroamericana, el cual entró en vigencia el 6 de mayo del 2013.

En Centroamérica se ha establecido el régimen de Libre Comercio para todos los productos originarios de sus respectivos territorios, con algunas excepciones, lo que significa que los productos originarios están exentos del pago de los Derechos Arancelarios a la Importación (DAI) y Exportación, los Derechos Consulares y demás impuestos.

Centroamérica se encuentra en el proceso de negociación para el perfeccionamiento de la Unión Aduanera Centroamericana, con el objetivo de facilitar el comercio en la región. Las actividades más importantes que estamos desarrollando son: la implementación de la Estrategia Centroamericana de

Central America Economic Integration System

The General Treaty on Central American Economic Integration signed on December 13, 1960 between Nicaragua, Guatemala, El Salvador, Honduras and Costa Rica, with the objective of establishing among them a Central American Common Market (CACM), pledging to perfect a Free Zone Trade, the adoption of a common external tariff and to establish a Customs Union between their territories. On June 29, 2012, Panama signs the Protocol of Incorporation to the Subsystem of Central American Economic Integration, which entered into force on May 6, 2013.

In Central America, the Free Trade regime has been established for all products originating in their respective territories, with some exceptions, which means that the originating products are exempt from the payment of Import Tariff Rights (DAI) and Exportation, Rights Consular and other taxes.

Central America is in the negotiation process for the improvement of the Central American Customs Union, with the aim of facilitating trade in the region. The most important activities we are developing are: the implementation of the Central American Strategy for Trade Facilitation

25AÑOS

Compromiso. Resultados. Excelencia.

ALVARADO Y ASOCIADOS

Guía del Inversionista 2018Doing Business in Nicaragua 2018

22 23

Facilitación de Comercio y Competitividad con énfasis en Gestión Coordinada en Fronteras; el desarrollo de una Plataforma Digital Centroamericana; la armonización de Reglamentos Técnicos, la armonización de procedimientos aduaneros; y completar el proceso de incorporación de Panamá al Subsistema de Integración Económica Centroamericana.

Acuerdos Comerciales

El Ministerio de Fomento Industria y Comercio (MIFIC) es la Institución a cargo de la Administración y Negociación de los Tratados de Libre Comercio suscritos por Nicaragua, promoción de las exportaciones y definición de la Política Comercial interna y externa del país pretendiendo la inserción de Nicaragua en el comercio internacional en condiciones más justas y equitativas, que permitan nuevas y mejores oportunidades de negocios.

Adhesión de Nicaragua a la Asociación Latinoamericana de Integración (ALADI): Está formada por Argentina, Bolivia, Brasil, Chile, Colombia, Cuba, Ecuador, México, Paraguay, Perú, Panamá, Uruguay y Venezuela. El Consejo de Ministros de Relaciones Exteriores de ALADI aprobó el 11 de agosto del 2011, la adhesión de Nicaragua al Tratado de Montevideo de 1980. Para afectos de la incorporación plena de Nicaragua a este foro, está pendiente la finalización de las Nóminas de Apertura de Mercados con Paraguay y Colombia.

DR-CAFTA – Tratado de Libre Comercio entre Centroamérica, República Dominicana y Estados Unidos de América. Durante los 12 años de vigencia del CAFTA DR, en el año 2016 EEUU sigue siendo el principal destino de las exportaciones nicaragüenses registrando una participación del 52.9%, incluyendo las Zonas Francas.

Las divisas generadas por Nicaragua en concepto de exportaciones hacia los EEUU fueron por el orden de los USD 2,531.7 millones, los USD2,507.0 millones exportados en el 2015. En términos de volumen crecieron de 502.7 T.M. en 2015 a 569.6 T.M. en 2016, para un crecimiento porcentual de 13.4%.

Nicaragua exportó a los EEUU bienes como prendas y complementos de vestir, de punto; prendas y complementos de vestir, excepto de punto; oro en bruto; café oro; carne de bovino; puros y puritos de tabaco; hilos, cables y demás conductores eléctricos; azúcar de caña; bananos; langostas; artículos de tapicería; pescado entero; quesos; camarones; calzado de cuero; frijoles rojos; moluscos y otros invertebrados; melaza de caña; artículos de joyería; plátanos; plantas vivas; jeringas, agujas y catéteres y similares; manufacturas de cuero; entre otros.

and Competitiveness with emphasis on Coordinated Border Management; The development of a Central American Digital Platform; Harmonization of technical regulations, harmonization of customs procedures; And to complete the process of incorporation of Panama into the Subsystem of Central American Economic Integration.

Commercial Agreements

The Ministry of Development, Industry and Trade (MIFIC) is the institution in charge of the administration and negotiation of free trade agreements subscribed by Nicaragua, exports´ promotion, and the defining of external and internal commercial policies pretending Nicaragua´s insertion into international markets in just and equal conditions, that allow new and better business opportunities.

Adhesion of Nicaragua to the Latin American Integration Association (LAIA)Formed by Argentina, Bolivia, Brazil, Chile, Colombia, Cuba, Ecuador, Mexico, Paraguay, Peru, Panama, Uruguay, and Venezuela. The Council of Ministers of Foreign Affairs of LAIA approved on August 11th, 2011, Nicaragua’s adhesion to the 1980 Montevideo Treaty. For the full insertion of Nicaragua to this forum, the completion of the lists of markets opening with Paraguay and Colombia is still pending.

Free Trade Agreement between Nicaragua, United States and Dominican Republic (DR- CAFTA)

During the 12 years of DR CAFTA, in 2016 the United States continues to be the main destination of Nicaraguan exports, registering a participation of 52.9%, including the Free Zones.

The foreign exchange generated by Nicaragua for exports to the US was in the order of USD 2,531.7 million compared to the USD2, 507.0 million exported in 2015. In terms of volume grew from 502.7 T.M. in 2015 to 569.6 T.M. in 2016, for a percentage growth of 13.4%.

Nicaragua exported goods to the US as knitted garments and accessories; garments and clothing accessories, other than knitted or crocheted; raw gold; gold coffee; beef; cigars and cigarillos; cables, wire and other electrical conductors; cane sugar; bananas; lobsters; upholstery articles; whole fish; cheeses; prawns; leather footwear; red beans; mollusks, and other invertebrates; cane molasses; jewelry items; bananas; live plants; syringes, needles and catheters and the like; manufactures of leather; among others.

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Source: Ministry of Development, Industry and Trade (MIFIC)

Nicaragua: Exportaciones totales hacia los Estados UnidosNicaragua: Total exports to the United States

Mill

one

s US

$ M

illio

ns U

S$

Guía del Inversionista 2018Doing Business in Nicaragua 2018

24 25

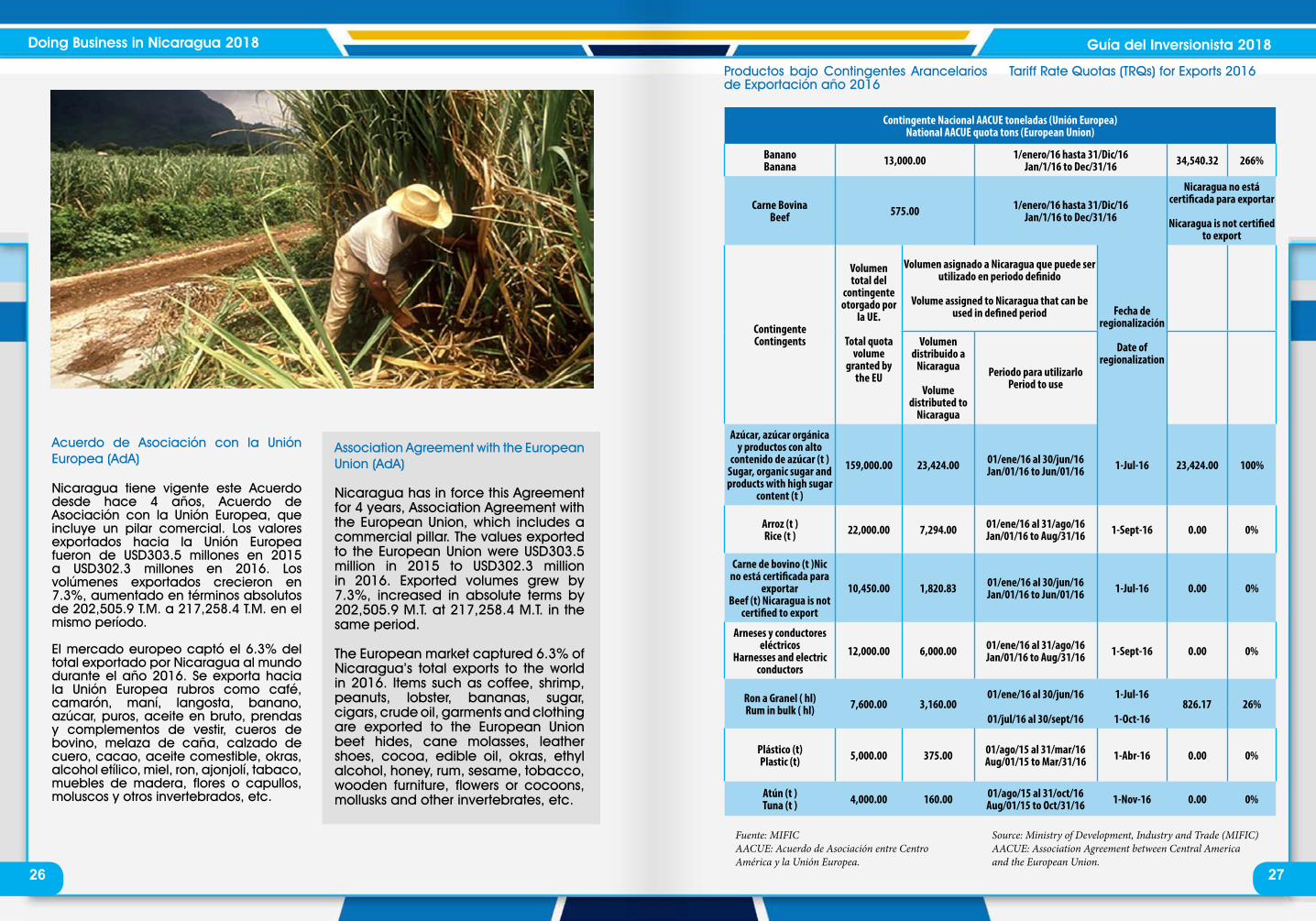

Productos bajo Contingentes Arancelarios de Exportación año 2016

ContingenteContingents

Volumen total del

contingente

Total Volume of Tariff Quota

Vigencia del contingente 1/

Validation Period

Volumen exportado del contingente

Exported Volume

Porcentaje de

Utilización

Utilization Rate

CAFTA- DR Estados Unidos de América T.M. United States of America CAFTA- DR M.T

Carne bovina (T.M) 15,500.00

Estados Unidos pone a disposición este contingente, una vez agotada la cuota de carne bovina que establece en la OMC y que puede ser utilizada por “otros países” incluyendo Nicaragua.

The United States puts into disposition this contingent, once the beef quota established by the WTO is reached and can be used by “other countries” including Nicaragua.

Azúcar (T.M) Sugar (M.T) 26,400

1/ene/16 hasta 31/

dic/16

From Jan/1/16 to Dec/31/16

26,400.00 100.00%

Maníes (T.M) Peanut (M.T) 16,000 0.00 0%

Mantequilla de maní (T.M)Peanut butter (M.T) 560 0.00 0%

Queso (T.M) Cheese (M.T) 1,018 1,018.00 100%

Queso (T.M) Cheese (M.T) 407 407.00 100%

Otros productos lácteos (T.M)Other dairy products (M.T) 163 0.00 0%

Helados (litros)Ice cream (M.T) 434,897 0.00 0%

Leche y crema fresca fluida y natilla (litros)

Milk and fresh cream and custard (liters)

414,819 0.00 0%

CAFTA-DR República Dominicana t.m United States of America DR-CAFTA M.T

Pechuga de Pollo Chicken breast 443.00 1/ ene/16

hasta el 31/dic/16

From Jan/1/16 to Dec/31/16

0.00 0%

Cebollas y Chalotes Onions and Shallots 375.00 0.00 0%

Frijoles Beans 1,800.00 0.00 0%

Contingentes OMC (Estados Unidos) Contingents WTO (United States)

Azúcar cruda (T.M) Raw sugar (M.T) 27,019.00 1-Oct-15 hasta 30-Sept-16 27,019.00 100%

Azúcar cruda (T.M)Raw sugar (M.T) 22,114.00 1-Oct-16 hasta 30-Sept-17 11,619.29 53%

Tariff Rate Quotas (TRQs) for Exports 2016

THE POWER OF BEING UNDERSTOOD

THE POWER OF BEING UNDERSTOODAUDIT | TAX | CONSULTING

E: [email protected] W: www.rsm.ni T: +505 2254 7801 Intl:+1 (786) 245 8921

As one of the largest Audit, Tax and Consulting networks in the world, we are committed to quality and excellence in business.

RSM Nicaragua

RSM - el destino global para sus necesidades en Auditoría, Impuestos y Consultoría.

Auditoría de Estados FinancierosContabilidades y Cumplimiento FiscalAsesoría en ImpuestosAuditoría Fiscal PreventivaPrecios de TransferenciaServicios en Modalidad de OutsourcingDebidas DiligenciasContabilidad de FideicomisosAdministración de Líneas de DenunciasAuditoría InternaImplementación de ERP’sTI Continuidad del NegocioHackeo ÉticoNIIF Integrales y para PYMEs

RSM - the Global Destination for your Audit, Tax and Consulting needs.

Audit of Financial StatementsAccounting and Tax ComplianceTax AdvisoryPreventive Tax AuditTransfer PricingOutsourcing (Invoicing, Payroll, Payments)Due DiligencesTrusts AccountingLETICA Hot Line Report’s ManagementInternal Audit ERP’s ImplementationIT Business ContinuityEthical HackingIFRS in full and for SMEs

C: [email protected] Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Source: Ministry of Development, Industry and Trade (MIFIC)

Guía del Inversionista 2018Doing Business in Nicaragua 2018

26 27

Acuerdo de Asociación con la Unión Europea (AdA)

Nicaragua tiene vigente este Acuerdo desde hace 4 años, Acuerdo de Asociación con la Unión Europea, que incluye un pilar comercial. Los valores exportados hacia la Unión Europea fueron de USD303.5 millones en 2015 a USD302.3 millones en 2016. Los volúmenes exportados crecieron en 7.3%, aumentado en términos absolutos de 202,505.9 T.M. a 217,258.4 T.M. en el mismo período.

El mercado europeo captó el 6.3% del total exportado por Nicaragua al mundo durante el año 2016. Se exporta hacia la Unión Europea rubros como café, camarón, maní, langosta, banano, azúcar, puros, aceite en bruto, prendas y complementos de vestir, cueros de bovino, melaza de caña, calzado de cuero, cacao, aceite comestible, okras, alcohol etílico, miel, ron, ajonjolí, tabaco, muebles de madera, flores o capullos, moluscos y otros invertebrados, etc.

Productos bajo Contingentes Arancelarios de Exportación año 2016

Contingente Nacional AACUE toneladas (Unión Europea)National AACUE quota tons (European Union)

BananoBanana 13,000.00 1/enero/16 hasta 31/Dic/16

Jan/1/16 to Dec/31/16 34,540.32 266%

Carne Bovina Beef 575.00 1/enero/16 hasta 31/Dic/16

Jan/1/16 to Dec/31/16

Nicaragua no está certificada para exportar

Nicaragua is not certified to export

ContingenteContingents

Volumen total del

contingente otorgado por

la UE.

Total quota volume

granted by the EU

Volumen asignado a Nicaragua que puede ser utilizado en periodo definido

Volume assigned to Nicaragua that can be used in defined period Fecha de

regionalización

Date of regionalization

Volumen distribuido a

Nicaragua

Volume distributed to

Nicaragua

Periodo para utilizarlo Period to use

Azúcar, azúcar orgánica y productos con alto

contenido de azúcar (t ) Sugar, organic sugar and products with high sugar

content (t )

159,000.00 23,424.00 01/ene/16 al 30/jun/16Jan/01/16 to Jun/01/16 1-Jul-16 23,424.00 100%

Arroz (t )Rice (t ) 22,000.00 7,294.00 01/ene/16 al 31/ago/16

Jan/01/16 to Aug/31/16 1-Sept-16 0.00 0%

Carne de bovino (t )Nic no está certificada para

exportarBeef (t) Nicaragua is not

certified to export

10,450.00 1,820.83 01/ene/16 al 30/jun/16Jan/01/16 to Jun/01/16 1-Jul-16 0.00 0%

Arneses y conductores eléctricos

Harnesses and electric conductors

12,000.00 6,000.00 01/ene/16 al 31/ago/16Jan/01/16 to Aug/31/16 1-Sept-16 0.00 0%

Ron a Granel ( hl) Rum in bulk ( hl) 7,600.00 3,160.00

01/ene/16 al 30/jun/16 1-Jul-16826.17 26%

01/jul/16 al 30/sept/16 1-Oct-16

Plástico (t) Plastic (t) 5,000.00 375.00 01/ago/15 al 31/mar/16

Aug/01/15 to Mar/31/16 1-Abr-16 0.00 0%

Atún (t )Tuna (t ) 4,000.00 160.00 01/ago/15 al 31/oct/16

Aug/01/15 to Oct/31/16 1-Nov-16 0.00 0%

Association Agreement with the European Union (AdA)

Nicaragua has in force this Agreement for 4 years, Association Agreement with the European Union, which includes a commercial pillar. The values exported to the European Union were USD303.5 million in 2015 to USD302.3 million in 2016. Exported volumes grew by 7.3%, increased in absolute terms by 202,505.9 M.T. at 217,258.4 M.T. in the same period.

The European market captured 6.3% of Nicaragua’s total exports to the world in 2016. Items such as coffee, shrimp, peanuts, lobster, bananas, sugar, cigars, crude oil, garments and clothing are exported to the European Union beet hides, cane molasses, leather shoes, cocoa, edible oil, okras, ethyl alcohol, honey, rum, sesame, tobacco, wooden furniture, flowers or cocoons, mollusks and other invertebrates, etc.

Tariff Rate Quotas (TRQs) for Exports 2016

Fuente: MIFICAACUE: Acuerdo de Asociación entre Centro América y la Unión Europea.

Source: Ministry of Development, Industry and Trade (MIFIC)AACUE: Association Agreement between Central America and the European Union.

Guía del Inversionista 2018Doing Business in Nicaragua 2018

28 29

Tratado de Libre Comercio Taiwán

Desde la entrada en vigencia del Tratado de Libre Comercio entre Nicaragua y Taiwán hace 9 años, las exportaciones de Nicaragua han presentado un comportamiento positivo. El mercado taiwanés es de importancia para la oferta exportable de Nicaragua, ocupando en el 2016 la sexta posición como destino de las exportaciones nicaragüenses.

Al finalizar el año 2016 los valores exportados hacia Taiwán alcanzaron los USD74.9 millones, en el 2015 se exportaron USD83.8 millones.

Entre los productos que Nicaragua ha exportado hacia Taiwán aparecen camarones, carne de bovino, azúcar de caña, café oro, langostas, despojos de bovino, moluscos y otros invertebrados, desechos de hierro o acero, tripas y estómagos de bovino, desechos de cobre, crustáceos y moluscos preparados o conservados, melaza de caña, maní sin cocer, observándose gran potencia para otros bienes.

TLC Taiwán - Nicaragua t.m FTA Taiwan - Nicaragua m.t

Maní (cacahuates) (T.M)Peanuts (M.T) 250.00

1/enero/16 hasta 31/Dic/16

Jan/01/16 to Dec/31/16

199.87 80%

Azúcar refinada (T.M)Refined sugar (M.T) 21,067.00 12,600.00 60%

Azúcar cruda (T.M)Raw sugar (M.T) 10,379.00 0.00 0%

Exportaciones hacia países de Centroamérica y Panamá

Las exportaciones hacia la región centroamericana: el valor exportado fue de USD$695.8 millones en el año 2016 y USD$712.4 en el año 2015, Centroamérica en el 2016 siguió siendo el segundo mercado en importancia para la oferta exportable de Nicaragua con una participación del 14.6% en 2016.

A nivel regional el principal comprador de productos nicaragüenses durante 2016 fue El Salvador con USD261.7 millones (37.6%); seguido de Honduras, USD150.1

Free Trade Agreement between Nicaragua and Taiwan

Since the entry into force of the Free Trade Agreement between Nicaragua and Taiwan 9 years ago, Nicaraguan exports have shown a positive behavior. The Taiwanese market is of importance for the exportable supply of Nicaragua, occupying in 2016 the sixth position as destination of Nicaraguan exports.

At the end of 2016, the values exported to Taiwan reached USD74.9 million, in 2015 USD83.8 million were exported.

Among the products that Nicaragua has exported to Taiwan are shrimp, beef, cane sugar, gold coffee, lobsters, offal of bovine animals, mollusks and other invertebrates, waste of iron or steel, guts and stomachs of cattle, copper waste, crustaceans and mollusks prepared or preserved, cane molasses, uncooked peanuts, observing great power for other goods.

Exports to countries of Central America and Panama

Exports to the Central American region: the value exported was USD$695.8 million in 2016 and USD$712.4 in 2015, Central America in 2016 remained the second largest market for Nicaragua’s exportable supply with a share of 14.6% in 2016.

At the regional level, the main purchaser of Nicaraguan products during 2016 was El Salvador with USD261.7 million (37.6%);

Source: Ministry of Development, Industry and Trade (MIFIC)

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Guía del Inversionista 2018Doing Business in Nicaragua 2018

30 31

millones (21.6%); Costa Rica, USD145.6 millones (20.9%); Guatemala, USD96.4 millones (13.9%); y Panamá, USD42.0 millones (6.0%).

Nicaragua exporta hacia Centroamérica carne de bovino; quesos; prendas y complementos de vestir; frijoles rojos; leche en polvo; café instantáneo; ganado bovino; preparaciones para la alimentación infantil; maní sin cocer; residuos para alimentos de animales; agua, incluida la mineral y la gaseada; tabaco en rama; productos de panadería, pastelería o galletería; puros y puritos de tabaco; loza sanitaria; ron; solventes minerales; camarones; leche fluida; harina de trigo; entre otros.

tLc Panamá - nicaragua t.m / Fta Panama - nicaragua

carne bovino Beef

2,130.00

1/enero/16 hasta 31/Dic/16Jan/01/16 to Dec/31/16

2,130.00 100%

carne de cerdo Pork

15.00 0.00 0%

cebollas y chalotes onions and Shallots

248.00 0.00 0%

café Instantáneo Instant coffee

60.00 0.00 0%

Salsa de tomate Sauce

450.00 0.00 0%

Ketchup 50.00 0.00 0%

Tratado de Libre Comercio entre México y Centroamérica

México es un importante socio comercial para Nicaragua en el marco del Tratado Único de Libre Comercio entre dicho país y Centroamérica. Las exportaciones nicaragüenses hacia el mercado mexicano aumentaron de USD519.1 millones en 2015 a USD 631.3 millones en 2016, creciendo un 21.6%, obteniendo el mismo resultado positivo los volúmenes exportados al crecer en 6.8%.

México en el 2016 se situó como el tercer destino de los envíos de productos nicaragüenses al mercado mundial, con una participación de 13.2%, superado solamente por EEUU y Centroamérica. Sobresale el incremento de las exportaciones de los volúmenes y valores exportados de conductores eléctricos (arneses) en 30.4% y 27.2%, respectivamente, con relación al 2015, siendo el principal producto de exportación hacia el mercado mexicano.

Además de los arneses, Nicaragua exportó a México carne bovina; maní; aceite en bruto; camarón; prendas y complementos de vestir; langosta; tejidos de algodón; ajonjolí; despojos de bovino; preparaciones y conservas de carne; cueros y pieles de bovino; desechos de cobre; filete de pescado; ron; pan y galletas; entre los principales.

followed by Honduras, USD150.1 million (21.6%); Costa Rica, USD145.6 million (20.9%); Guatemala, USD96.4 million (13.9%); and Panama, USD42.0 million (6.0%).

Nicaragua exports bovine meat to Central America; cheeses; clothing and accessories; red beans; milk powder; instant coffee; cattle; preparations for infant feeding; uncooked peanuts; waste for animal feed; water, including mineral and gassed; raw tobacco; bakery, confectionery or biscuit products; cigars and cigarillos; sanitary ware; ron; mineral solvents; prawns; fluid milk; wheat flour; among others.

Tratado de Libre Comercio entre Chile y Centroamérica El Tratado de Libre Comercio entre Chile y Centroamérica que entró en vigencia hace cinco años. Nicaragua ha exportado a Chile durante 2016 un total de USD2.9 millones, creciendo en 8.1% con relación al 2015 cuando se exportaron USD2.7 millones.

Free Trade Agreement between Central America and Mexico

Mexico is an important trade partner for Nicaragua within the framework of the single Free Trade Agreement between that country and Central America. Nicaraguan exports to the Mexican market increased from USD519.1 million in 2015 to USD631.3 million in 2016, growing by 21.6%, with export volumes growing by 6.8%.

In 2016, Mexico was the third destination of shipments of Nicaraguan products to the world market, with a share of 13.2%, surpassed only by the US and Central America. The increase in exports of export volumes and values of electric conductors (harnesses) stands at 30.4% and 27.2%, respectively, in relation to 2015, being the main export product to the Mexican market.

In addition to harnesses, Nicaragua exported to Mexico, beef, peanut, crude oil, shrimp, clothing and accessories, locust, cotton fabrics, sesame, offal of bovine animals, preparations and preserves of meat, hides and skins of bovine animals, copper waste, fish steak, ron, bread and biscuits, among the main.

Free Trade Agreement between Chile and Central America

The Free Trade Agreement between Chile and Central America that came into effect five years ago. Nicaragua has exported to Chile during 2016 a total of USD2.9 million, growing at 8.1% compared to 2015 when USD2.7 million were exported.

Source: Ministry of Development, Industry and Trade (MIFIC)

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Source: Ministry of Development, Industry and Trade (MIFIC)

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Nicaragua: Exportaciones totales hacia MéxicoNicaragua: Total exports to Mexico

Mill

one

s US

$ M

illio

ns U

S$

Guía del Inversionista 2018Doing Business in Nicaragua 2018

32 33

Del total de bienes exportados al mercado chileno en el 2016 sobresale una canasta de 12 productos, los cuales representaron el 97.6% del valor exportado hacia el país sudamericano en este año, destacando los siguientes rubros: materias colorantes; ron; preparaciones utilizadas en fabricación de tintas; calzado y artículos de prendería; polímeros en formas primarias; productos de panadería, pastelería o galletería; prendas y complementos de vestir, excepto de punto; azúcar de caña, café oro, tejidos de algodón.

Chile presenta grandes oportunidades comerciales para los exportadores nicaragüenses al contar con una población mayor a los 18 millones de personas que tiene un alto poder adquisitivo. El sector privado debe realizar mayores acciones encaminadas para aprovechar al máximo el TLC.

Of the total goods exported to the Chilean market in 2016 stands a basket of 12 products, which represented 97.6% of the value exported to the South American country in this year, highlighting the following items: coloring matters, ron, preparations used in the manufacture of inks, footwear and articles of apparel, polymers in primary forms, bakery, confectionery or biscuit products, garments and clothing accessories, other than knitted or crocheted, sugar cane, coffee gold, cotton fabrics.

Chile has great commercial opportunities for Nicaraguan exporters as it has a population of more than 18 million people with a high purchasing power. The private sector must take more action aimed at making the most of the FTA.

Source: Ministry of Development, Industry and Trade (MIFIC)

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Nicaragua: Total exports to ChileNicaragua: Exportaciones totales hacia Chile

Mill

one

s US

$ M

illio

ns U

S$

Guía del Inversionista 2018Doing Business in Nicaragua 2018

34 35

Tratado de Libre Comercio República Dominicana.

Nicaragua exportó hacia República Dominicana durante el año 2016 USD28.3 millones, (octavo destino de las exportaciones nicaragüenses). Ambos países están libres de aranceles como parte de lo negociado. Los principales productos exportados hacia la República Dominicana durante el 2016 fueron: tejidos de algodón; tabaco en rama; productos de panadería, pastelería o galletería; azúcar de caña; tabacos y sucedáneos del tabaco; alcohol etílico sin desnaturalizar; medicamentos para uso humano; tintas de imprimir, escribir o pintar; preparaciones utilizadas en fabricación de tintas; frijol negro; madera aserrada; café molino; maní sin cocer; herbicidas; puros y puritos de tabaco; cebolla, pescado, etc.

caFta-Dr república Dominicana t.m / caFta-Dr Dominican republic M.tPechuga de Pollo chicken breast 443.00

1/ ene/16 hasta el 31/dic/16Jan/ 01/16 to Dec/31/16

0.00 0%

cebollas y chalotes onions and Shallots 375.00 0.00 0%

Frijoles Beans 1,800.00 0.00 0%

Venezuela

Venezuela ha venido evolucionando como uno de los principales socios comerciales desde que Nicaragua se adhirió al ALBA en enero del año 2007, convirtiéndose en un mercado alternativo importante para una serie de bienes agropecuarios. Nicaragua envía al mercado venezolano productos como carne de bovino, azúcar, aceite comestible, café, leche fluida, ganado bovino, frijoles negros y bebidas a base de pulpa, principalmente. Durante el año 2016 se exportó USD113.6 millones.

Dominican Republic Free Trade Agreement

Nicaragua exported USD28.3 million to the Dominican Republic in 2016 (eighth destination of Nicaraguan exports). Both countries are duty free as part of the deal. The main products exported to the Dominican Republic during 2016 were: cotton fabrics, raw tobacco, bakery, confectionery or biscuit products, cane sugar, tobacco and tobacco substitutes, undenatured ethyl alcohol, medicinal products for human use, printing, writing or coloring inks, preparations used in the manufacture of inks, black bean, sawn timber, coffee mill, uncooked peanuts, herbicides, cigars and cigarillos, onion, fish, etc.

Venezuela

Venezuela has been evolving as one of the main trading partners since Nicaragua joined ALBA in January 2007, becoming an important alternative market for a number of agricultural goods. Nicaragua sends to the Venezuelan market products such as beef, sugar, edible oil, coffee, fluid milk, cattle, black beans and mainly pulp-based beverages. During 2016, USD113.6 million was exported.

Solid Legal Framework

Within the effective legal framework, there are different legal norms that regulate the county´s investments, within these norms, it is important to point out the Civil Code and the Commercial Code, Article 344 “Foreign Investment Promotion Law”, states that foreign investors will enjoy the same rights and means to exercise their equality in the same conditions as national investors, similarly, exercise their equality in the same conditions as national investors, similarly, the full recognition of use and ownership by foreign investors of related property to his investment without any more limitations as the ones stated by the political constitution, his free access to the purchase and sell of foreign currency available with respect to the conversion and transfer of funds related to his investment, freedom to utility, dividends, and earnings transferability, previous tax payment and liberty for payment and remission to the exterior of payments for debt obtained in the foreign country, interest: royalty, income and technical assistance, and Article 540 “Law of Mediation and Arbitrage” which regulates the alternative methods of solution to any type of controversy that can result from the

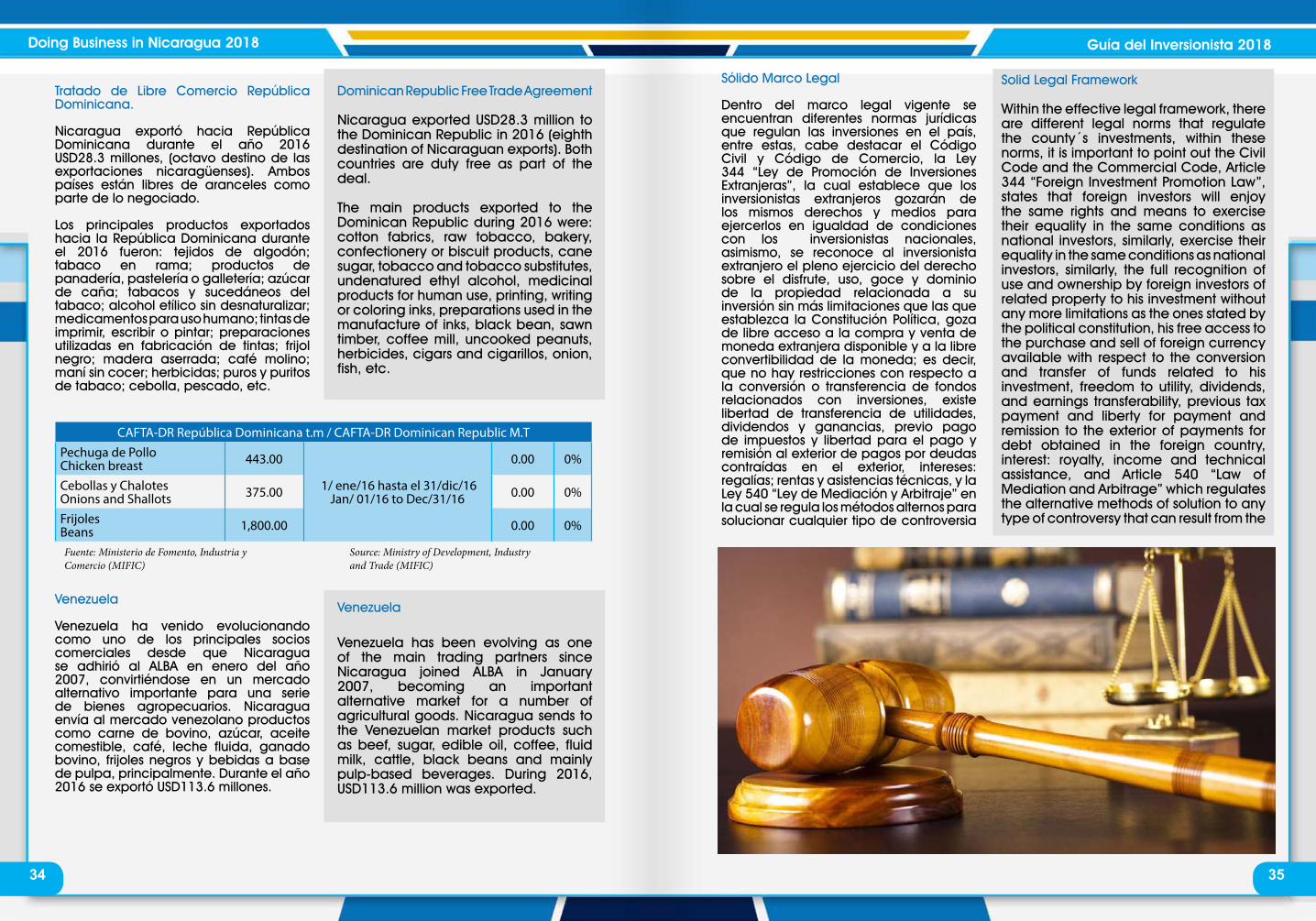

Sólido Marco Legal

Dentro del marco legal vigente se encuentran diferentes normas jurídicas que regulan las inversiones en el país, entre estas, cabe destacar el Código Civil y Código de Comercio, la Ley 344 “Ley de Promoción de Inversiones Extranjeras”, la cual establece que los inversionistas extranjeros gozarán de los mismos derechos y medios para ejercerlos en igualdad de condiciones con los inversionistas nacionales, asimismo, se reconoce al inversionista extranjero el pleno ejercicio del derecho sobre el disfrute, uso, goce y dominio de la propiedad relacionada a su inversión sin más limitaciones que las que establezca la Constitución Política, goza de libre acceso a la compra y venta de moneda extranjera disponible y a la libre convertibilidad de la moneda; es decir, que no hay restricciones con respecto a la conversión o transferencia de fondos relacionados con inversiones, existe libertad de transferencia de utilidades, dividendos y ganancias, previo pago de impuestos y libertad para el pago y remisión al exterior de pagos por deudas contraídas en el exterior, intereses: regalías; rentas y asistencias técnicas, y la Ley 540 “Ley de Mediación y Arbitraje” en la cual se regula los métodos alternos para solucionar cualquier tipo de controversia

Source: Ministry of Development, Industry and Trade (MIFIC)

Fuente: Ministerio de Fomento, Industria y Comercio (MIFIC)

Guía del Inversionista 2018Doing Business in Nicaragua 2018

36 37

que resulte de las relaciones contractuales y su ámbito de aplicación es de carácter nacional e internacional, sin perjuicio de los tratados, convenios, pacto o cualquier otro instrumento de Derecho Internacional del cual Nicaragua sea parte.

El país también ha firmado varios acuerdos bilaterales y multilaterales con distintos países y regiones del mundo, como CAFTA-RD, el Acuerdo de Asociación con la Unión Europea, el Tratado de Libre Comercio de Centroamérica y México, el Tratado de Libre Comercio entre la República de Nicaragua y la República de China (Taiwán), el Tratado de Libre Comercio con Panamá, el Tratado de Libre Comercio entre Centroamérica y Chile, los Acuerdos de Alcance parcial firmados con Colombia, Ecuador y la República Bolivariana de Venezuela y otros que se encuentran en proceso de negociación.

Nicaragua está inserta en el mercado mundial a través de los distintos organismos de los que forma parte como OMC, SICA, COMIECO, SIECA, CAUCA, CEIE y del BCIE. También es parte del CIADI, OMGI, OPIC, CNUDMI, de la Convención de Nueva York y la Convención Interamericana sobre Arbitraje Comercial, y los acuerdos celebrados con el Organismo Multilateral de Garantía de Inversiones del Banco Mundial (MIGA).

Todo este amplio cuerpo normativo internacional regula las relaciones comerciales de Nicaragua con el mundo, constituyéndose en un destino propicio para dirigir las miradas hacia la inversión y el desarrollo económico.

Una nueva Oportunidad de Inversión en Nicaragua: Ley de Asociación Público-Privada

A mediados de octubre del 2016, la Asamblea Nacional de Nicaragua aprobó “Ley de Asociación Público-Privada” (APP), la cual viene a regular la participación de los sectores público y privado en la formulación, contratación, financiación, ejecución, operación y extinción de proyectos en Asociación Pública Privada. Esta ley es un claro ejemplo de las políticas de promoción y estímulo de las inversiones privadas en proyectos de

contractual relationships, its application is of national and international interest, without prejudice of the treaties, pacts or any other instrument of international rights of which Nicaragua is a part of.

Nicaragua has also signed a number of bilateral and multilateral agreements with several countries and regions of the world, such as CAFTA-DR, the Agreement of Association with the European Union, the Free Trade Agreement with Central America and Mexico, the Free Trade Agreement between Nicaragua and the Republic of China (Taiwan), the Free Trade Agreement with Panama, the Free Trade Agreement between Central America and Chile, the Agreement of Partial Reach signed by Colombia, Ecuador, and the Bolivarian Republic of Venezuela, and others which are in negotiating terms.

Nicaragua is immersed in the global market through the different organizations of which it is part of, such as, WTC, SICA, COMIECO, SIECA, CAUCA, CEIE, and BCIE. Nicaragua also forms part of CIADI, OMGI, OPIC, CNUDMI, the New York Convention and the Inter American Convention on Commercial Arbitrage, and the agreements celebrated with the Multilateral Investment Guarantee Agency of the World Bank (MIGA).

All this International normative body regulates the commercial relations between Nicaragua and the world, becoming a favorable destiny to turn the eyes towards investment and the economic development.

A New Investment Opportunity in Nicaragua: Public-Private Partnership Law

In mid-October 2016, the National Assembly of Nicaragua approved the “Public-Private Partnership Law” (APP for its Spanish acronym), which regulates the participation of the public and private sectors in the formulation, contracting, financing, execution, operation and extinction of projects in Public Private Partnership. This law is a clear example of policies to promote and encourage

Guía del Inversionista 2018Doing Business in Nicaragua 2018

38 39

interés nacional, para el desarrollo del país y para el beneficio y satisfacción de las necesidades de la población, sin perjuicio de la soberanía nacional.

Según la Ley APP y su reglamento, todo el que esté interesado en que le sea adjudicado un Contrato de Asociación Público Privada puede competir bajo procedimientos, regulaciones o métodos que fomenten, en condiciones de igualdad, la más amplia, objetiva e imparcial concurrencia y pluralidad de potenciales participantes, que permita escoger al Participante Privado que pueda construir la infraestructura pública, prestar el servicio público o ambos de la forma más eficaz y eficiente.

En este contexto normativo se reconoce la seguridad jurídica como un principio básico en los actos y contratos firmados bajo el esquema del APP. El ente regulador gubernamental de la Ley APP es el “Ministerio de Hacienda y Crédito Público”, a través de su división “Dirección General de Inversiones Públicas” encargado de la elaboración y coordinación de planes, políticas y normas para el desarrollo y buen funcionamiento de la APP, esquema de contratación, y supervisar el cumplimiento de la ley y su Reglamento.

El modelo APP comprende una serie de características como la formulación, financiación, construcción, desarrollo, uso, disfrute, operación, mantenimiento, modernización, ampliación y mejora de las nuevas instalaciones de infraestructura pública, y los equipos asociados, así como la rehabilitación, la modernización, la explotación y el mantenimiento de la ya existente infraestructura pública y la prestación de los servicios públicos, a través de un participante privado que aporta recursos a los bienes del Estado.

De tal forma que, la regulación establecida en la Ley 935 y su Reglamento crean un entorno normativo e institucional apropiado para atraer la inversión privada y para garantizar una adecuada gestión de los proyectos estructurados bajo esta modalidad para materializar con éxito la oportunidad que ofrecen las APP.

Marco Institucional para las Inversiones

En Nicaragua existe un marco institucional destinado a propiciar y facilitar la inversión en el país. PRONicaragua, la Agencia Oficial para la Promoción de las Inversiones del Gobierno de Nicaragua, ofrece al inversionista información sobre las oportunidades de negocio del país, asistencia durante el proceso de inversión, asesoría para inversiones conjuntas, identificación de proveedores y alianzas empresariales, asistencia en la identificación de bienes raíces, servicios posteriores al establecimiento de la empresa, entre otros.

Por otra parte, el Ministerio de Fomento, Industria y Comercio (MIFIC), tiene entre sus funciones la responsabilidad de promover el acceso a mercados externos, negociar y administrar convenios internacionales especialmente en el ámbito del comercio y la inversión, apoyar al sector privado en el aprovechamiento de los mercados internacionales, promover y facilitar la inversión en la economía del país, para ello, ha creado una Ventanilla Única de Inversiones (VUI) especialmente destinada a atender al inversionista en su proceso de formalización y legalización en el país. En esta instancia se otorga atención centralizada para instalar empresas: Registro de la Alcaldía de Managua (ALMA), para obtener la matrícula municipal, el Registro de la (DGI), para obtener el registro único de contribuyentes (RUC) y su cuota como contribuyente, y el Registro Mercantil para inscribir su actividad como comerciante y la adquisición de propiedades.

El Registro Estadístico de Inversiones Extranjeras del MIFIC, para ser declarado como inversionista extranjero en la actividad comercial que desea desarrollar, asegurando la protección a su inversión con la aplicación de las reglas internacionales del comercio, este registro es voluntario. La integración de estas cuatro instancias en una ventanilla única ha reducido significativamente los costos y los tiempos para formalizar una empresa.

Ambas entidades, PRONicaragua y MIFIC, son fundamentales para la promoción de la inversión en el país, junto a ellas existen otras instituciones destinadas a

private investment in projects of national interest, for the development of the country and for the benefit and satisfaction of the needs of the population, without prejudice to national sovereignty.

According to the Law APP and its regulations, anyone interested in being awarded a Public Private Partnership Contract may compete under procedures, regulations or methods that promote, on equal terms, the most comprehensive, objective and impartial concurrence and plurality of potential participants, that allows to choose the Private Participant that can build the public infrastructure, provide the public service or both in the most effective and efficient way.

In this legal context, legal certainty is recognized as a basic principle in acts and contracts signed under the APP scheme. The government regulatory body of the APP is the “Ministry of Finance and Public Credit”, through its division “General Direction of Public Investments” responsible for the preparation and coordination of plans, policies and standards for the development and smooth operation of the APP, contracting scheme, and supervise compliance with the law and its regulations.

The APP model comprises a number of features such as formulation, financing, construction, development, use, enjoyment, operation, maintenance, modernization, expansion and improvement of new public infrastructure facilities, and associated equipment, as well as rehabilitation, modernization, exploitation and maintenance of the existing public infrastructure and the provision of public services, through a private participant who contributes resources to the State’s assets.

Thus, the regulation established in Law 935 and its regulations create an appropriate regulatory and institutional environment to attract private investment and to ensure proper management of projects structured under this modality to successfully materialize the opportunity offered by the APPs.

Institutional Framework for Investments

In Nicaragua there exists an institutional framework destined to propitiate and facilitate investment in the Country. PRONicaragua, the Official Agency of Investment Promotion of the Nicaraguan Government, provides the investor with information on the business opportunities in the country, assistance during the process of investment, legal counseling for conjunct investments, supplier identification and private alliances, assistance in the identification of real estate, after care services to business establishment, and others. Moreover, the Ministry of Development, Industry and Trade (MIFIC), has among its functions, the responsibility to promote access to external markets, negotiating and administering international conventions, especially in the field of trade and investment, support the private sector in the use of international markets, promote and facilitate investment in the country’s economy, for it has created a Unique Window for Investment (VUI, for its Spanish acronym) specially designed to meet the investor in the process of formalization and legalization in the country. In this case, centralized attention is given to install companies: Town Hall Registry in Managua (ALMA) to obtain the municipal solvency, the registry of (DGI) to obtain the unique taxpayer registration (RUC) and its share as a taxpayer, and the Commercial Registry to register their activity as a trader and property acquisition.

The MIFIC Statistical Register of Foreign Investments, to be declared as a foreign investor in the commercial activity that it wishes to develop, ensuring the protection of its investment with the application of the international rules of commerce, this registration is voluntary. The integration of these four instances into a single window has significantly reduced costs and time to formalize a company. Both entities, PRONicaragua and MIFIC, are fundamental for the investment

Guía del Inversionista 2018Doing Business in Nicaragua 2018

40 41

brindar algún tipo de servicio que facilite el desarrollo de la inversión, entre estas podemos destacar el Centro de Trámites de las Exportaciones (CETREX), la Corte Suprema de Justicia a través del Registro Público de la Propiedad Inmueble y Mercantil, la Dirección General de Ingresos (DGI), las Alcaldías Municipales, el Ministerio del Trabajo y el Instituto de Seguridad Social (INSS).

La Comisión Nacional de Promoción de Exportaciones (CNPE), presidida por el Ministro del MIFIC, está integrada por representantes del sector empresarial y del sector público; y está encargada de proponer nuevas medidas de política que contribuyan al desarrollo de las empresas exportadoras. También existe la Comisión Interinstitucional de Facilitación del Comercio (CIFCO) la cual está integrada por 14 representantes de instituciones públicas y privadas: DGA, MIFIC, DGI, el Ministerio de Transporte, la Empresa Nacional de Puertos (ENAP), la Empresa Administradora de Aeropuertos Internacionales (EAAI), el Consejo Superior de la Empresa Privada (COSEP), la Cámara de Industria de Nicaragua (CADIN), la Cámara de Agentes Aduaneros y Almacenadores de Nicaragua (CADAEN), la Cámara de Comercio y Servicios de Nicaragua (CCSN), el Consejo Nicaragüense de la Micro, Pequeña y Mediana Empresa (CONIMIPYME), entre otros.

promotion of the country, next to them, there are other institutions to provide some kind of service to facilitate the development of investment, among these we can highlight the Center for Export Procedures (CETREX) the Supreme Court through the Public Registry of Property and Commerce, the General Directorate of Revenue (DGI), the Municipal Town Hall, the Ministry of Labor and Social Security Institute (INSS). The National Export Promotion Commission (CNPE), chaired by the Minister of MIFIC is composed of different representatives of the private and public sectors, and is responsible for proposing new policy measures that contribute to the development of export enterprises. DGA, MIFIC, DGI, the Ministry of Transport, the National Port Company (ENAP), the Airports Administrator Company: the Interagency Commission on Trade Facilitation (CIFCO) which is composed of 14 representatives of public and private institutions, The enterprise in charge of managing the international airport (EAAI), the Superior Council of Private Enterprise (COSEP), the Chamber of Industry of Nicaragua (CADIN), the Chamber of Customs Brokers and warehouses Nicaragua (CADAEN), the Chamber of Commerce and Services Nicaragua (CNSC), the Nicaraguan Council of Micro, Small and Medium Enterprises (CONIMIPYME), among others.

We are making

in NicaraguaHISTORY

TASTRO CAR ON NICARAGUA 2ND, S.A.

PBX: (505) 2298 5210 / 2298 5211 We reciprocate for your support

supplying quality goods with due punctualityPachino Lee / Managing Director & Gerente General

www.astrocarton.com

Guía del Inversionista 2018Doing Business in Nicaragua 2018

42 43

El pasado 12 de octubre del 2016 entró en vigencia la Ley No. 935, Ley de Asociación Público Privada (“Ley de las APP”), por la cual se crea un novedoso régimen que promueve la participación del sector público con el sector privado en la ejecución de proyectos relacionados con nuevas infraestructuras, mantenimiento de infraestructuras existentes, o la prestación de servicios públicos que sean requeridos por instituciones públicas en Nicaragua.

El país en los últimos diez años ha invertido recursos importantes en energía, en la construcción de carreteras, hemos avanzado bastante en agua potable, en distintas inversiones estratégicas, pero el país merece doblar la cantidad de inversión, es decir, necesitamos hacer más carreteras, construir puertos en el Caribe.

Generosos Incentivos Fiscales

Ley de Concertación Tributaria (Ley 822)

La Ley de Concertación Tributaria (LCT), establece diversos beneficios tributarios a ciertos sectores productivos de la economía con el objetivo de fomentar el crecimiento y/o desarrollo de los mismos. Las exenciones y exoneraciones otorgadas por esta Ley, se establecen sin perjuicio de las otorgadas por las disposiciones legales establecidas en el art. 287 de la misma.

Beneficios Tributarios a la Exportación

A las exportaciones de bienes de producción nacional o servicios prestados al exterior se les aplicará una tasa del 0% de Impuesto al Valor Agregado (IVA). Las exportaciones de bienes están gravadas con 0% del Impuesto Selectivo al Consumo (ISC).

Se puede aplicar un crédito tributario a los anticipos o IR anual con previo aval de la administración tributaria en un monto equivalente al 1.5% del valor FOB de las exportaciones.

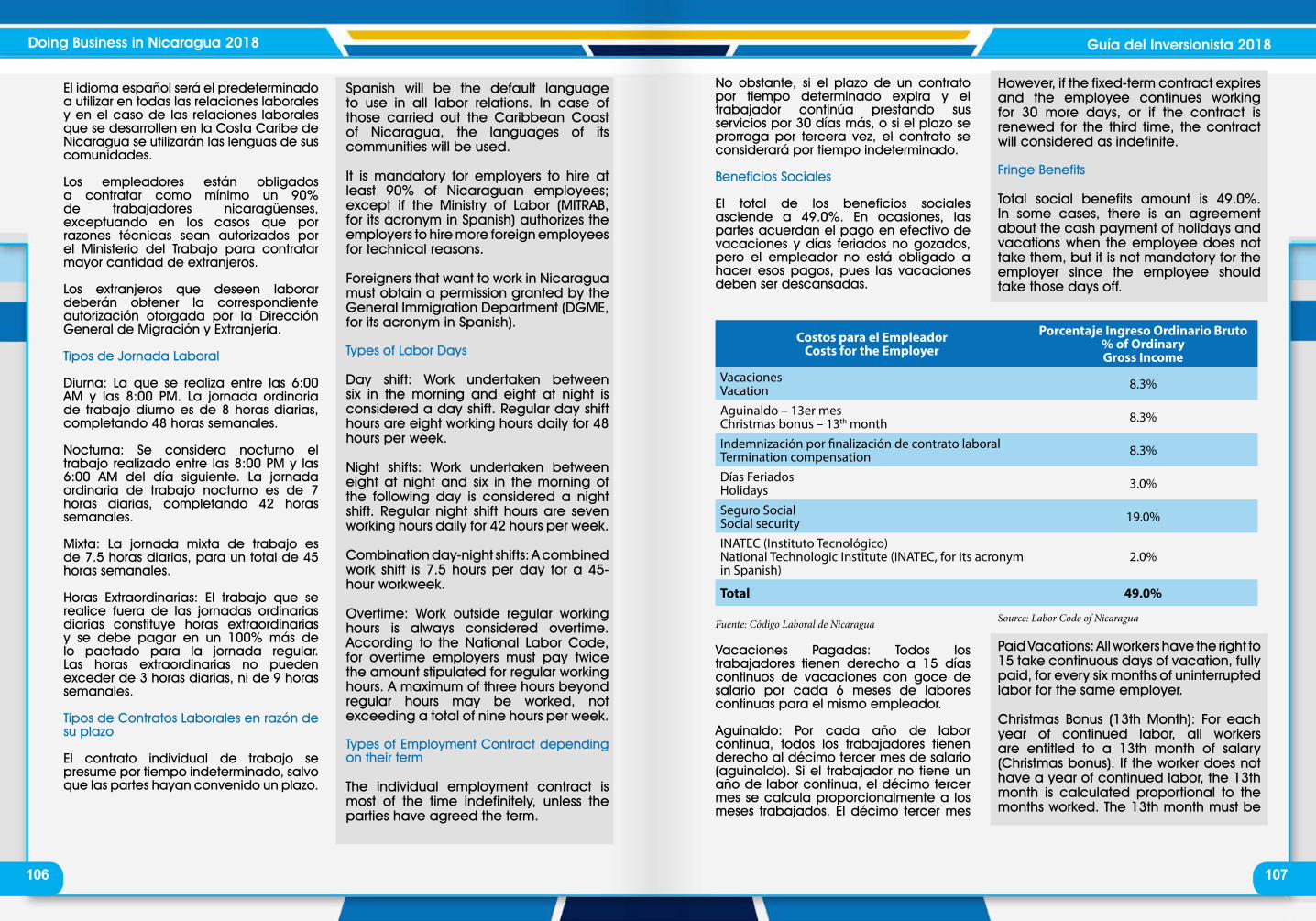

Beneficios Tributarios a los Productores