investor presentation july10

TRANSCRIPT

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 1/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 2/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 3/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 4/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 5/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 6/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 7/36

7

Mobile Services Telemedia Services Enterprise Services

Segment contribution…Rev, EBITDA and Investment

REVENUE

82%8%

21%9% 2%

Mobile Services Telemedia ServicesEnterprise Services Passive Infrastructure Services

Others

EBITDA

63%

10%26%

12% -8%

Mobile Services Telemedia ServicesEnterprise Services Passive Infrastructure ServicesOthers

Note: (1) Revenue and EBITDA is gross of inter segment eliminations.

INVESTMENTS

51%

11%14%

22%3%

Mobile Services Telemedia ServicesEnterprise Services Passive Infrastructure ServicesOthers

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 8/36

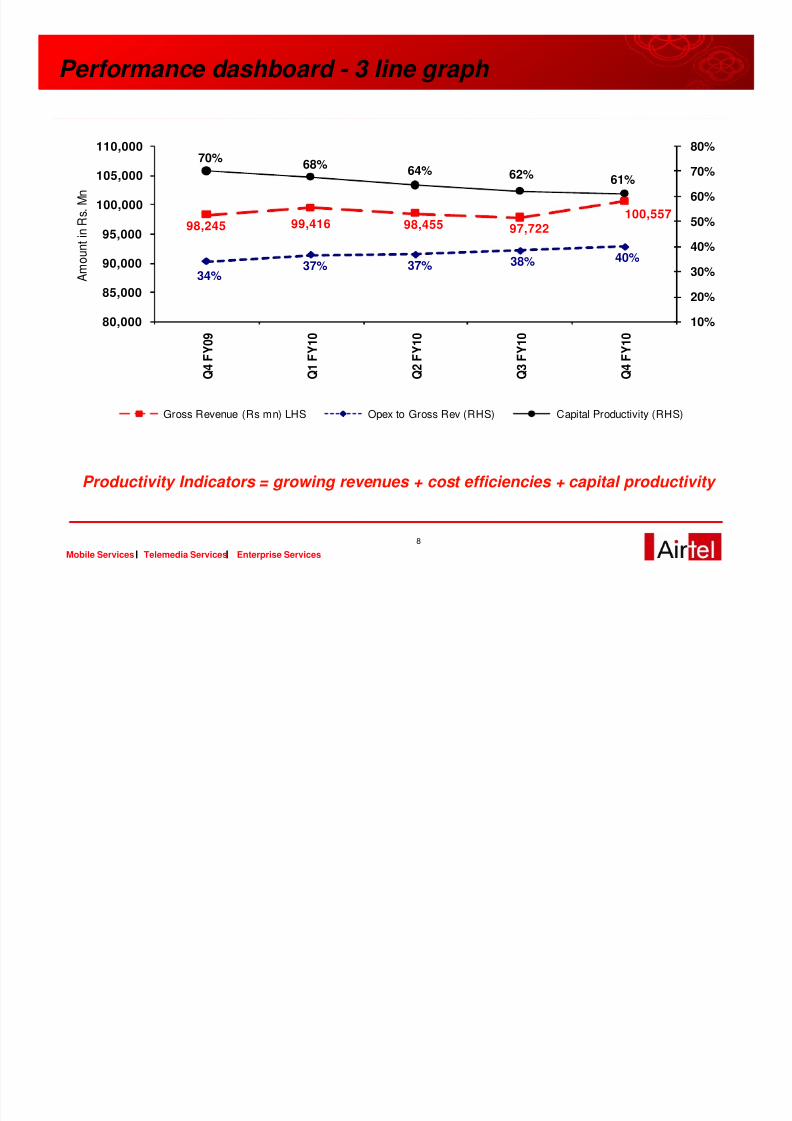

8

Mobile Services Telemedia Services Enterprise Services

Performance dashboard - 3 line graph

Productivity Indicators = growing revenues + cost efficiencies + capital productivity

98,245 99,416 98,455 97,722100,557

34%37% 37% 38% 40%

70% 68% 64% 62% 61%

10%

20%

30%

40%

50%

60%

70%

80%

80,000

85,000

90,000

95,000

100,000

105,000

110,000

Q 4 F Y 0 9

Q 1 F Y 1 0

Q 2 F Y 1 0

Q 3 F Y 1 0

Q 4 F Y 1 0

A m o u

n t i n R s

. M n

Gross Revenue (Rs mn) LHS Opex to Gross Rev (RHS) Capital Productivity (RHS)

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 9/36

9

Mobile Services Telemedia Services Enterprise Services

Wireless Services

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 10/36

10

Mobile Services Telemedia Services Enterprise Services

Sub Base : 635.51 mn → second largest market

Wireless Penetration: 53.77% → lowest in the world

HHI Index: very high → one of the most competitive market

Prepaid Base: 96% → one of the highest in the world

Usage per sub per month:

Minutes: 381→ one of the highest

ARPU: ~ US$ 4.08 → one of the lowest

Rate per minute: ~ US$ 0.01→ one of the lowest in the world

VAS: ~ 11.8% → One of the lowest

Indian Wireless Market…KPIs

MUM

HP

DELHI

AP

CHN

MADHYA PRADESH`

TNKER

PB

DEL

UP(W)

MP

RAJUP(E)

KK

OR

HAR

JK

BH

WBGUJ

MAH

AS

NE

Metros

A Cat.

B Cat.

C Cat.

MUM

HP

DELHI

AP

CHN

MADHYA PRADESH`

TNKER

PB

DEL

UP(W)

MP

RAJUP(E)

KK

OR

HAR

JK

BH

WBGUJ

MAH

AS

NE

Metros

A Cat.

B Cat.

C Cat.

MUM

HP

DELHI

AP

CHN

MADHYA PRADESH`

TNKER

PB

DEL

UP(W)

MP

RAJUP(E)

KK

OR

HAR

JK

BH

WBGUJ

MAH

AS

NE

Metros

A Cat.

B Cat.

C Cat.

Metros

A Cat.

B Cat.

C Cat.

Kol

Note: (1) Subscriber numbers and wireless penetration numbers as on June 30, 2010 are as per TRAI release (2) Other indicators on the slide are based on Global Wireless Matrix 2Q10 dated 9 th July 10 by Merrill Lynch, and reflective of Industry numbers.

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 11/36

11

Mobile Services Telemedia Services Enterprise Services

Net Adds in Jun 18.0 Mn…greater than over last 2 months average run rate of 16.6 Mn S-curve triggered

Rapidly Growing Wireless Market

Note: (1) Actual Data as per Industry Association Releases and Industry Estimates.

Fastest Growing Market in the World

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

-

100

200300

400

500

600

700800

-2468

10121416182022

Series2 Series1

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 12/36

12

Mobile Services Telemedia Services Enterprise Services

Wireless Market Structure

• Airtel continuously consolidating its market leadership position despite intense competition

• Airtel current monthly net adds at 3.04 million vs. 2.86 million a year ago• Airtel ranks 1& 2 in 17 circles in terms of number of subscribers• Over 59% of net adds coming from B&C circles (rural India)

Airtel Continues to lead on Revenue Market Share

Subscriber Trends Customer Market Share – CMS (%)

110.81 109.06

77.9168.89 72.53

59.69

34.25 31.19 32.6118.94 26.12

35.42 29.69

136.62

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

A i r t e l

R e l i a n c e

V o d a f o n e

B S N L +

M T N L

I d e a

T a t a

O t h e r s

( m n )

Jun-10 Jun-09 Net adds during the year

21.5%

17.4%

12.3%11.4%

9.4%

10.8%

17.2%

24.0%

18.6%17.9%

13.8%

10.0%8.7%

7.0%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

23.0%

25.0%

A i r t e l

R e l i a n c e

V o d a f o n e

B S N L +

M T N L

I d e a

T a t a

O t h e

r s

CMS(Jun'10) CMS(Jun'09)

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 13/36

13

Mobile Services Telemedia Services Enterprise Services

Company Highlights on Wireless Services

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 14/36

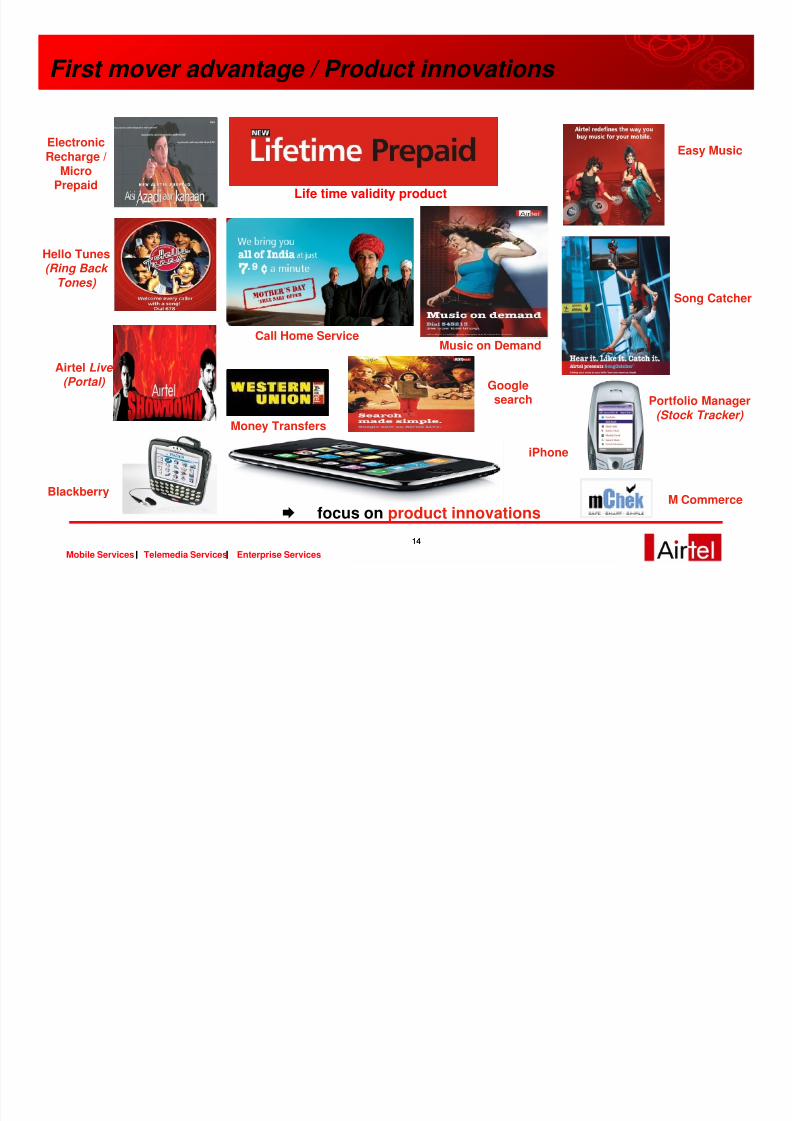

14

Mobile Services Telemedia Services Enterprise Services14

Hello Tunes(Ring Back

Tones)

Portfolio Manager(Stock Tracker)

Blackberry

Airtel Live (Portal)

First mover advantage / Product innovations

Life time validity product

ElectronicRecharge /

MicroPrepaid

focus on product innovations

Easy Music

Song Catcher

Call Home Service

Money Transfers

Music on Demand

Googlesearch

M Commerce

iPhone

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 15/36

15

Mobile Services Telemedia Services Enterprise Services

Performance Indicators - Financial

EBITDA (INR mn) & Margin (%) Revenues (INR mn)

23,969

21,218

24,178

25,860

27,183

22,009

24,963

25,860

20,000

21,000

22,000

23,000

24,000

25,000

26,000

27,000

28,000

Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

30.7 30.2 31.4 31.5 33.0 31.9 30.4 29.2

81,97579,618

64,201

69,150 72,843

79,39282,216 82,285

80,994

50,000

55,000

60,000

65,000

70,000

75,000

80,000

85,000

Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 16/36

16

Mobile Services Telemedia Services Enterprise Services

Performance Indicators - Operational

95.8%95.3%95.2%94.7%94.2%93.5%92.9%92.3%

91.6%91.0%

97.5%100 .4%

101.1%

100 .8%99.6%

98.4%95.4%96.3%

97.9%

101.70%

85%

90 %

95%

100 %

105%

Q308 Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

Prepaid Subs Prepaid Net Adds

Customers & Market Share Prepaid/Postpaid

MoU/Sub/Month & MON ARPU & RPM

474 505507 534 526 485 478 450 446 468

123,626

115,834

105,21789,058

73,840

130,669140,713

143,680153,241

172,797

370

40 0

43 0

46 0

49 0

520

550

Q3 08 Q4 08 Q109 Q20 9 Q30 9 Q4 09 Q110 Q2 10 Q310 Q4 100

40,000

80,000

120,000

160,000

200,000

MoU/Sub (Min) Total minutes on Netw ork (Mn Min)

127.6118.969.462.0 77.5 85.7 93.9 102.4 110.5

24.0%

24.2%23.7%

23.4%

24.6%24.7%

24.0%

22.6%

21.80%

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q41020.0%

21.0%

22.0%

23.0%

24.0%

25.0%

26.0%

27.0%

28.0%

Customers (Mn) CMS (%)

0.63 0 .580.630.64 0.560.650.700.76 0.52 0.47

3 58 3 573 50

331 324

30 5

278

252

23 0

22 0

-

0.25

0.50

0.75

1.0 0

1.2 5

1.50

Q308 Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q41020 0

23 0

26 0

29 0

32 0

350

38 0

RPM (Rs.) ARPU (INR)

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 17/36

17

Mobile Services Telemedia Services Enterprise Services

Current positioning and way forward…

Brand

Distribution

Churn lower than industry

Spectrum Mix (900/1800 MHz)

Improving cost efficiencies

Lowest cost GSM network

Revenue size ($ 9 Bn)

Revenue MarketShare

Increasing the usage through U&R drive

Wallet share

Driven by rural strategy

Changing face ofgrowth through M-Com,M-entertainment & 3G

Leadership Positioning Growth strategy and plans

Revenue

Non financial vitals

Cost

New Revenue Streams

Net Adds

Maximizing usage

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 18/36

18

Mobile Services Telemedia Services Enterprise Services

Telemedia Services

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 19/36

19

Mobile Services Telemedia Services Enterprise Services

A snapshot

Largest private operator having presence in the voice , broadband , IPTV and data.

Focus on SMB segment & Broadband at Homes

Key Performance Indicators

1. Voice (wire-line) and Data (DSL) Presence in 89 top cities of India.

2. Target Segment : Retail and Small and Medium Enterprises.

3. Customer base: 3.15 million (end June2010)

4. Broadband (DSL with speeds>256 kbps) penetration at 43.2% of customer base.

5. Average ARPU for Quarter ended Mar’10 $ 20.8 per month.

6. Segment contributing to 8% of overall revenues of the company.

7. EBITDA margin of over 43.5%.

Broadband revolution to follow wireless revolution in India

SMB opportunity across ICT stream

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 20/36

20

Mobile Services Telemedia Services Enterprise Services20

Telemedia Services

Business Units SMBs Homes

Products

• Voice• Data• Mobile Services• Applications

•SaaS

• Broadband• Voice• IPTV

Goal One-Stop Shop for All Airtel Servicesand Solutions to SMBs

Dominant Broadband & Fixed Voiceshare of the affluent in targeted 95cities

Strategies

• Data Products: Internet, MPLS etc.• Integrated Solutions to drive share of

wallet like hosted e mail, onlinedesktop etc.

• Strategic Alliances• Indirect Channel to Drive Penetration

• Deeper & Not Wider: 95 Cities• Enhancing Broadband experience :

Speed on Demand, Games onDemand & VAS

• Vertical & Not Horizontal: Hi-Rise• Drive Triple Play• Drive Higher spends for better

customer experience

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 21/36

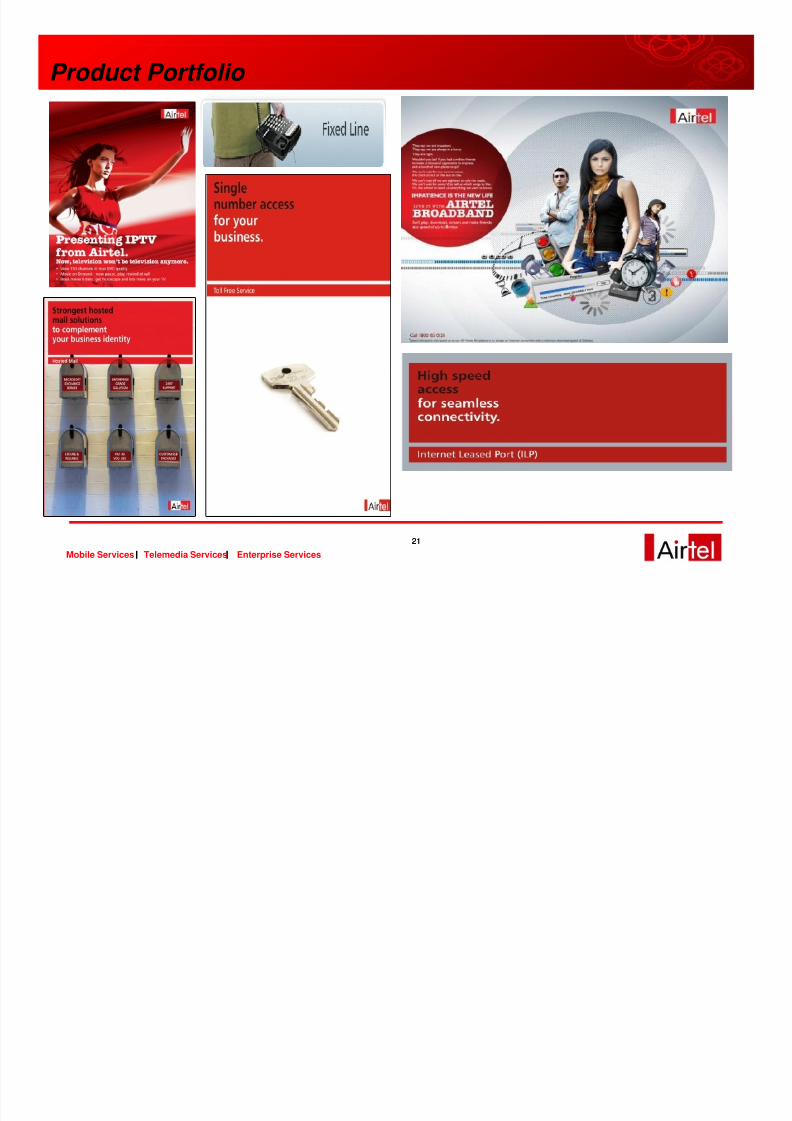

21

Mobile Services Telemedia Services Enterprise Services21

Product Portfolio

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 22/36

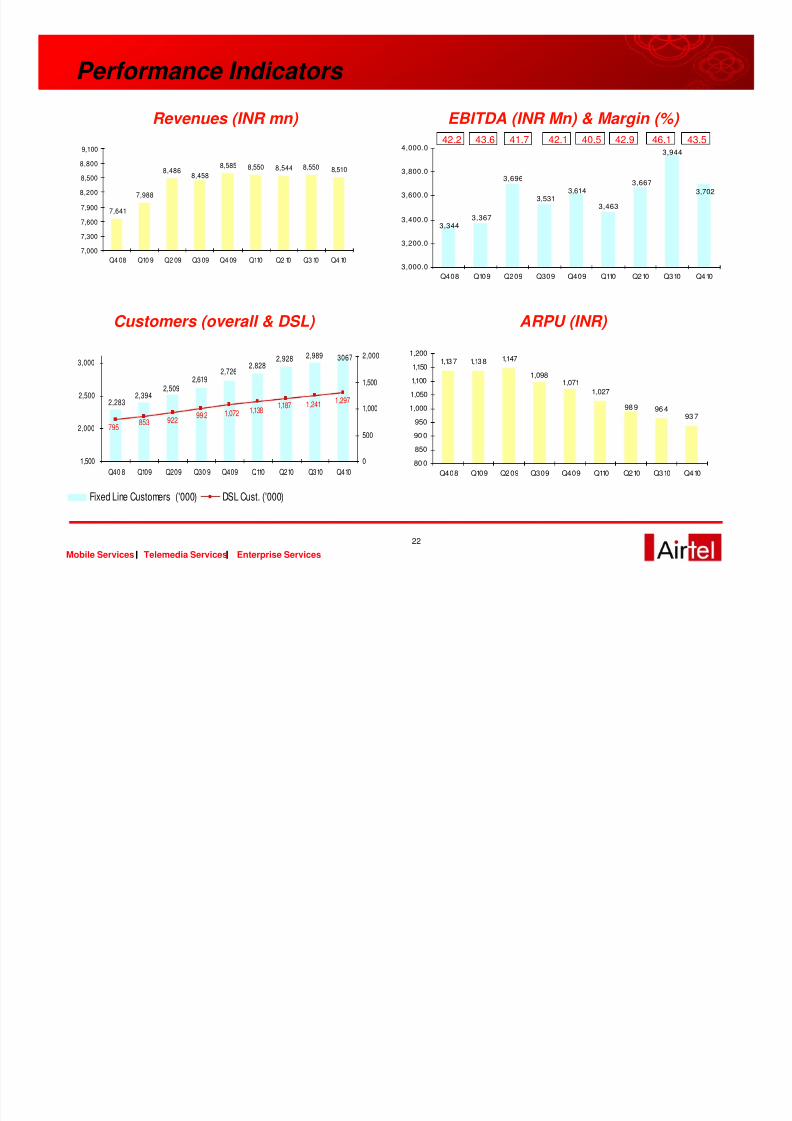

22Mobile Services Telemedia Services Enterprise Services

Performance Indicators

30672,9892,9282,828

2,3942,509

2,6192,726

2,283 1,2971,2411,1871,1381,072992922853795

1,500

2,000

2,500

3,000

Q40 8 Q109 Q209 Q30 9 Q409 Q110 Q210 Q310 Q4100

500

1,000

1,500

2,000

Fixed Line Customers ('000) DSL Cust. ('000)

1,13 7 1,13 8 1,147

1,027

96 493 7

1,0981,071

98 9

80 0

850

90 0

950

1,000

1,050

1,100

1,150

1,200

Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

3,702

3,344 3,367

3,696

3,5313,614

3,463

3,667

3,944

3,000.0

3,200.0

3,400.0

3,600.0

3,800.0

4,000.0

Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

42.2 43.6 41.7 42.1 40.5 42.9 46.1 43.5

Customers (overall & DSL) ARPU (INR)

Revenues (INR mn) EBITDA (INR Mn) & Margin (%)

7,641

7,988

8,4868,585 8,550 8,544 8,550 8,510

8,458

7,000

7,300

7,600

7,900

8,200

8,500

8,800

9,100

Q4 08 Q10 9 Q2 09 Q3 09 Q4 09 Q110 Q2 10 Q3 10 Q4 10

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 23/36

23Mobile Services Telemedia Services Enterprise Services

Enterprise Services

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 24/36

24Mobile Services Telemedia Services Enterprise Services

A snapshot

Enterprise Services provides a broad portfolio of services to large Enterprise and Carrier customers

Corporates: Single point of contact for all telecommunication needs for Top 2500 corporate

customers, providing full suite of voice, data, and managed communications solutions

Carriers: Wholesale voice and data services to over 130 domestic and 450 international telecommunications carriers, as well as ILD and NLD carriage for Airtel’s own customers

Extensive national and international infrastructure

Pan-India network with 126,357 Route kms of optical fiber, over 4,150 MPLS and SDH POPs

Access network (terrestrial) in 89 cities, Wimax network in 143 cities, and over 1,500 local POIs

International network with 225,000 Route Kms, connecting over 50 countries.

Key Performance Indicators (Q4 ‘10)

NLD Minutes Carried: 15.9 Billion ; ILD Minutes Carried: 3.2 Billion Revenue: Rs.20,738 Million (21 % Segment Contribution Share)

EBITDA: Rs. 9,846 Million (47.5% EBITA Margin)

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 25/36

25Mobile Services Telemedia Services Enterprise Services

Highlights

# 1 Operator in India in terms of:

NLD Revenue (Voice & Data)ILD Revenue (Voice & Data)

Corporate Fixed Line Operator

Corporate Internet Provider

Corporate Mobility Provider

VSAT Provider (installed base)

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 26/36

26Mobile Services Telemedia Services Enterprise Services

Domestic Network

Fiber commissioned for over 126,357

Kms

Transmission Network (14,000+ SDH nodes)

High resilience via ring structure &

automatic switching

Tier-1 MPLS network (across 120

Cities)

Internet backbone capacity > 60 Gbps

Proactive 24 x 7 x 365 NOC 304 LDCAs & 1680 SDCAs covered

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 27/36

27Mobile Services Telemedia Services Enterprise Services

International Network 27

Infrastructure NGN with 4 Global Media Gateways

100% Ownership of i2i Cable system and landing station

Ownership of Sea Me We 4 cable and landing station

IRU capacity on TAT-14, Apollo, EAC, APCN2, JUCN, etc.

Trans- Pacific Connectivity Boost through Unity & AAG

Terrestrial connectivity to Nepal, Pakistan and Bhutan

Consortium partner in major cable systems under construction: IMEWE, EIG,AAG, Unity, EASSy

Coverage

TDM and IP Voice traffic termination in 230+ countries

5 Major International PoPs for carrier interconnect at Los Angeles, New York,

London, Hong Kong & Singapore

8 additional PoP’s under development in cl. Colombo, Tokyo, Paris, Bangkok and Kaula Lumpur

Far-East and Middle-East Connect Platform to cater to high growth markets

across Asia and the Pacific

Extensive MPLS Coverage across the globe - more than 70 countries, 700+

PoPs via carrier-grade NNI’s

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 28/36

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 29/36

29Mobile Services Telemedia Services Enterprise Services

Performance Indicators – Enterprise Services

Voice Minutes on Network

Revenues (INR mn) EBITDA (INR mn) & Margin (%)

16,340

19,572

21,874 21,808 21,62820,982 21,331

20,546 20,738

14,000

15,000

16,000

17,000

18,00019,000

20,000

21,000

22,000

Q4 08 Q10 9 Q2 09 Q3 09 Q4 09 Q110 Q2 10 Q3 10 Q4 10

8,655

9,369 9,7999,920 10,246

11,023

10,0359,846

4,000.0

5,000.0

6,000.0

7,000.0

8,000.0

9,000.0

10,00 0.0

11,000.0

Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

44.2 42.8 44.9 45.9 48.8 51.7 48.8 47.5

10,32 211,349 11,609 11,6 90 11,78 1 12,417

13,94 4

3,100 3173

9,398

15875

3,1812,8692,7722,6032,2842,0481,850

0

2,000

4,000

6,000

8,000

10,00 0

12,00 0

14,00 0

16,00 0

Q4 08 Q10 9 Q2 09 Q3 09 Q4 09 Q110 Q2 10 Q3 10 Q4 10

NLD Minutes (mn) ILD Minutes (mn)

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 30/36

30Mobile Services Telemedia Services Enterprise Services

Passive Infrastructure Services

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 31/36

31Mobile Services Telemedia Services Enterprise Services

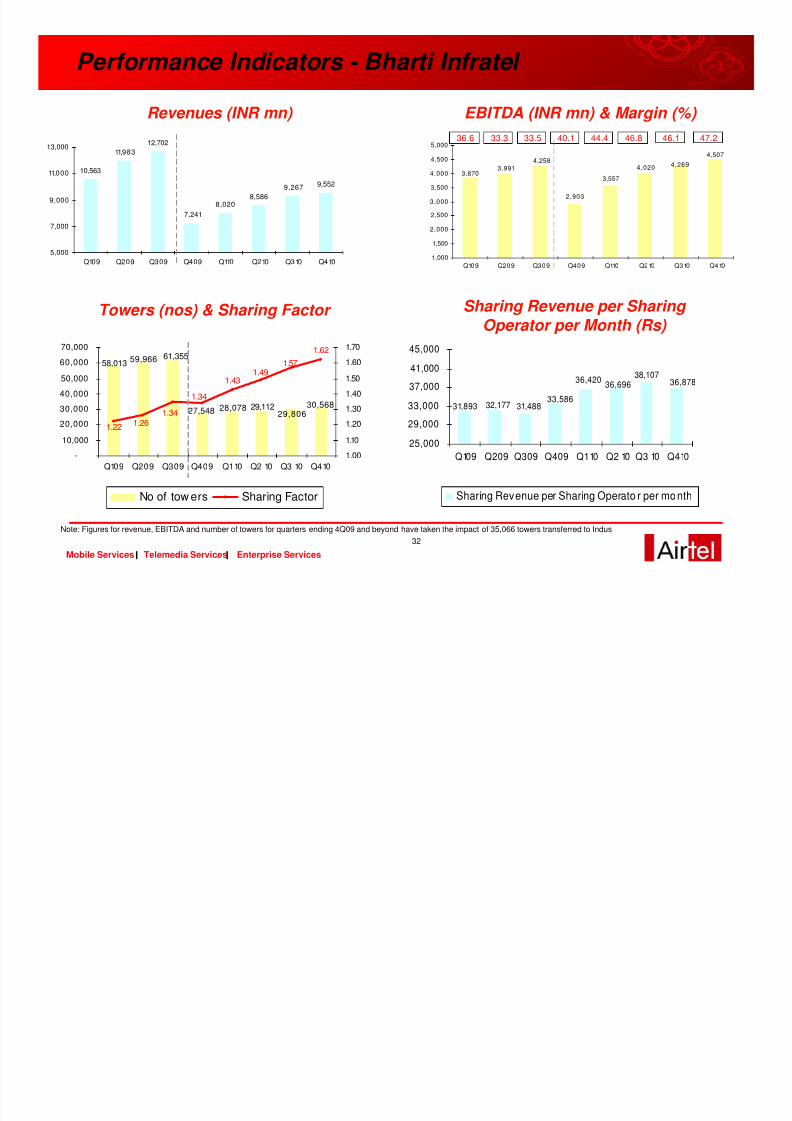

A snapshot

Bharti Infratel operates in 11 circles.Indus Tower operates in 16 circles.Standard Master Services Agreement with competitive rates already in place.Key focus areas:

To increase sharing factor (tenancy) from current levels of 1.62 for Infratel and 1.71 for Indus.Provide energy optimization solutions and other network management services.Evaluate other revenue streams.To reduce sharing revenue per sharing operator through increased sharing factor and efficiencies

Key performance Indicators (Infratel): Total Towers: 30,568 (nos)Sharing Factor: 1.62 Sharing Revenue per sharing operator per month at Rs. 36,878.EBITDA margin: 47.2%

Key performance Indicators (Indus): Total Towers: 102,938 (nos)Sharing Factor: 1.71

Aim to be the preferred choice of vendor for all existing and new operators

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 32/36

32Mobile Services Telemedia Services Enterprise Services

36,87838,107

36,69636,420

33,58632,17731,893 31,488

25,000

29,000

33,000

37,000

41,000

45,000

Q109 Q209 Q309 Q409 Q1 10 Q2 10 Q3 10 Q410

Sharing Revenue per Sharing Operato r per month

58,013 59,966

27,548 28,078 29,11229,806

61,355

30,568

1.22 1.261.34

1.34

1.431.49

1.571.62

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q109 Q209 Q309 Q409 Q1 10 Q2 10 Q3 10 Q4101.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

No of tow ers Sharing Factor

4,5074,269

3,8703,991

4,258

2,903

3,557

4,020

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

36.6 33.3 33.5 40.1 44.4 46.8 46.1 47.2

Performance Indicators - Bharti Infratel

10,563

11,98312,702

7,2418,020

8,5869,267 9,552

5,000

7,000

9,000

11,000

13,000

Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

Revenues (INR mn) EBITDA (INR mn) & Margin (%)

Towers (nos) & Sharing Factor Sharing Revenue per Sharing

Operator per Month (Rs)

Note: Figures for revenue, EBITDA and number of towers for quarters ending 4Q09 and beyond have taken the impact of 35,066 towers transferred to Indus

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 33/36

33Mobile Services Telemedia Services Enterprise Services

Indus Towers

Roof Top Tower

Ground Based TowerFirst of its kind deal…Bharti (42%), Voda (42%) &Idea (16%)

Largest independent tower company in the world

~ 100,000 towers under its management

Benefits from captive tenancy as well as external tenants

Incremental investment in towers to come from new operators / subscriber growth / 3G

102 ,696 102,938

100,728

97,9251.71

1.611.61

1.55

93,000

95,000

97,000

99,000

101,000

103,000

Q110 Q210 Q310 Q4101.40

1.50

1.60

1.70

1.80

1.90

No of towers Sharing Factor

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 34/36

34Mobile Services Telemedia Services Enterprise Services

Recent Honours

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 35/36

35Mobile Services Telemedia Services Enterprise Services

Rated as the ‘ Powerful Brand’ in the Economic Times- Brand

Finance ‘Brand Power (the only corporate brand to be awarded the

AAA rating)

Rated as India's Best Enterprise Services

Provider for 2009 at the annual Users’ Choice Awards

instituted by PC Quest.

Bharti Airtel – Leadership in business Recent Honours

Bharti Airtel won tele.net Telecom Operator awards in 6 out of total

14 categories including Most Admired Company, Best National Mobile operator, Best Internet and

Broadband operator, Best Operator

in Rural Market, Best Enterprise Services

Sunil Bharti Mittal , Chairman & Group CEO •Honorary degree of Doctor of Laws by

University of Leeds (UK) in 2009 •T enth Lal Bahadur Shastri National Award by the Hon’ble President of India in 2009 Akhil Gupta , Deputy Group CEO & MD •CA Business Achiever Award by Institute of Chartered Accountants of

India .Manoj Kohli , CEO( International) &Joint MD

• Telecom Man of the year by Tele.net in Apr’10

Best Cellular Service Provider and Best VSAT &

NLD player Service Provider at the 2009 Voice & Data

100 Awards

Adjudged Wireless Service Provider of the Year 2009 - Frost & Sullivan Asia Pacific

ICT Awards ( in recognition of innovation, vision ,

strategy and profitability)

Best Global Wholesale Carrier for 2009 at the

Telecoms World Awards Middle East.

Voted as the India’s Most Innovative company in a survey conducted by Wall

Street Journal

Adjudged Most Preferred Cellular Service Provider Brand award at the 2010 CNBC Awaaz Consumer Awards

8/8/2019 Investor Presentation July10

http://slidepdf.com/reader/full/investor-presentation-july10 36/36