Renewable Energy Asia 2015

3rd June 2015BITEC

The Future of Renewable Energy

in Thailand

Opportunities and Challenges

Dr. Praipol Koomsup

1

Contents

Current Energy Situation in Thailand

Renewable Energy Policy in Thailand

Challenges for RE Project Development

Way forward for future RE Development

1.

2.

3.

4.

The Future of Renewable Energy in ThailandOpportunities and Challenges

2

1. Current Energy Situation in Thailand

3

2

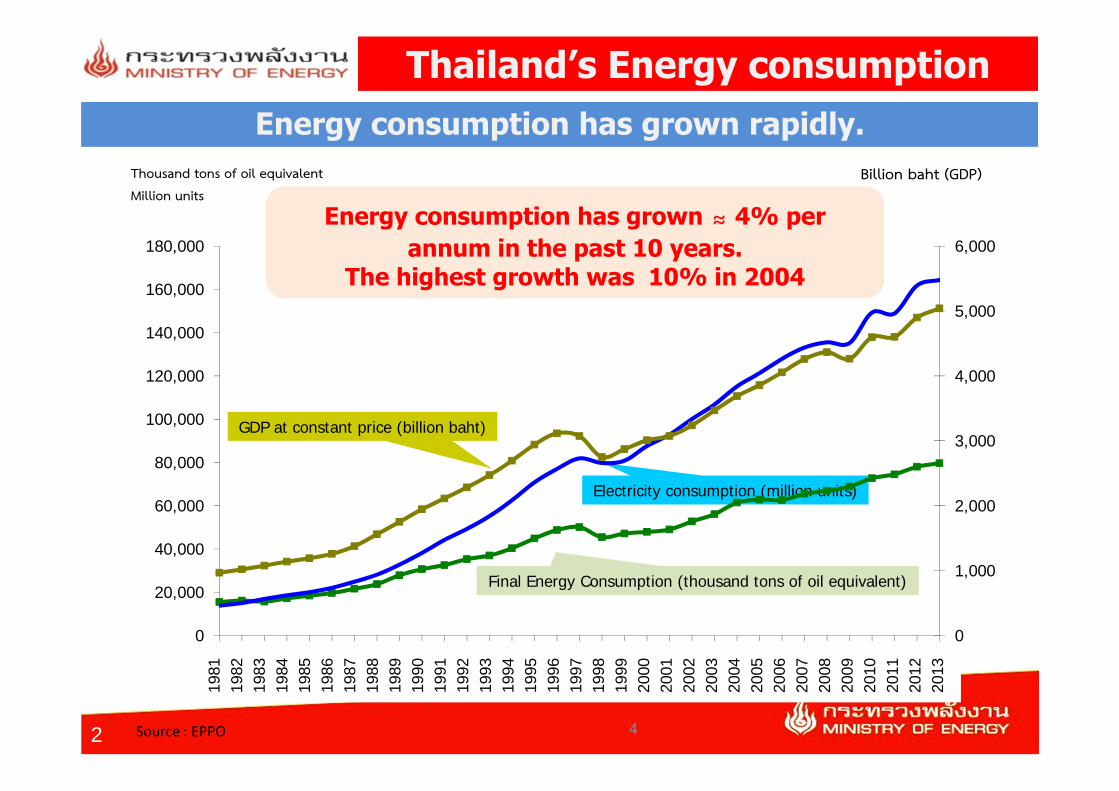

Thailand’s Energy consumptionEnergy consumption has grown rapidly.

Final Energy Consumption (thousand tons of oil equivalent)

Thousand tons of oil equivalent

Million unitsBillion baht (GDP)

GDP at constant price (billion baht)

Electricity consumption (million units)

Source : EPPO

Energy consumption has grown ≈ 4% per annum in the past 10 years.

The highest growth was 10% in 2004

0

1,000

2,000

3,000

4,000

5,000

6,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,00025

2425

2525

2625

2725

2825

2925

3025

3125

3225

3325

3425

3525

3625

3725

3825

3925

4025

4125

4225

4325

4425

4525

4625

4725

4825

4925

5025

5125

5225

5325

5425

5525

56

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

4

5SOURCE: Energy in Thailand – Facts and Figures

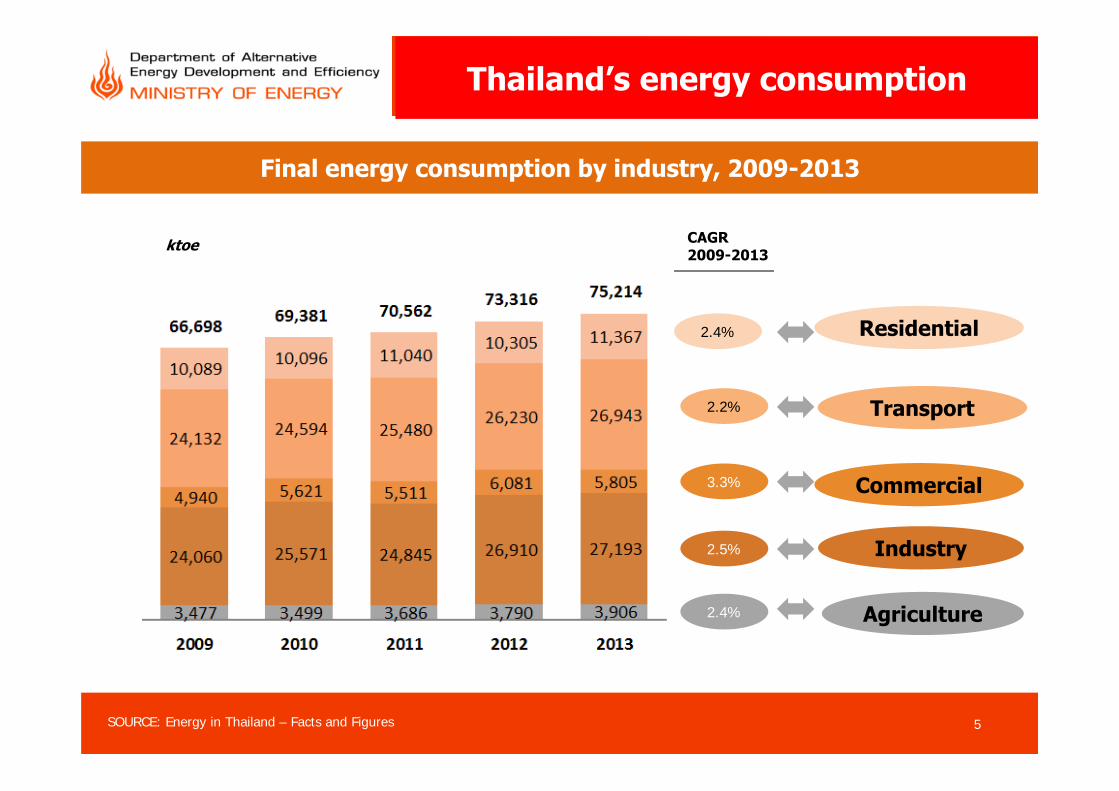

Final energy consumption by industry, 2009-2013

CAGR 2009-2013

2.4%

2.2%

3.3%

2.5%

2.4% Agriculture

Industry

Commercial

Transport

Residential

ktoe

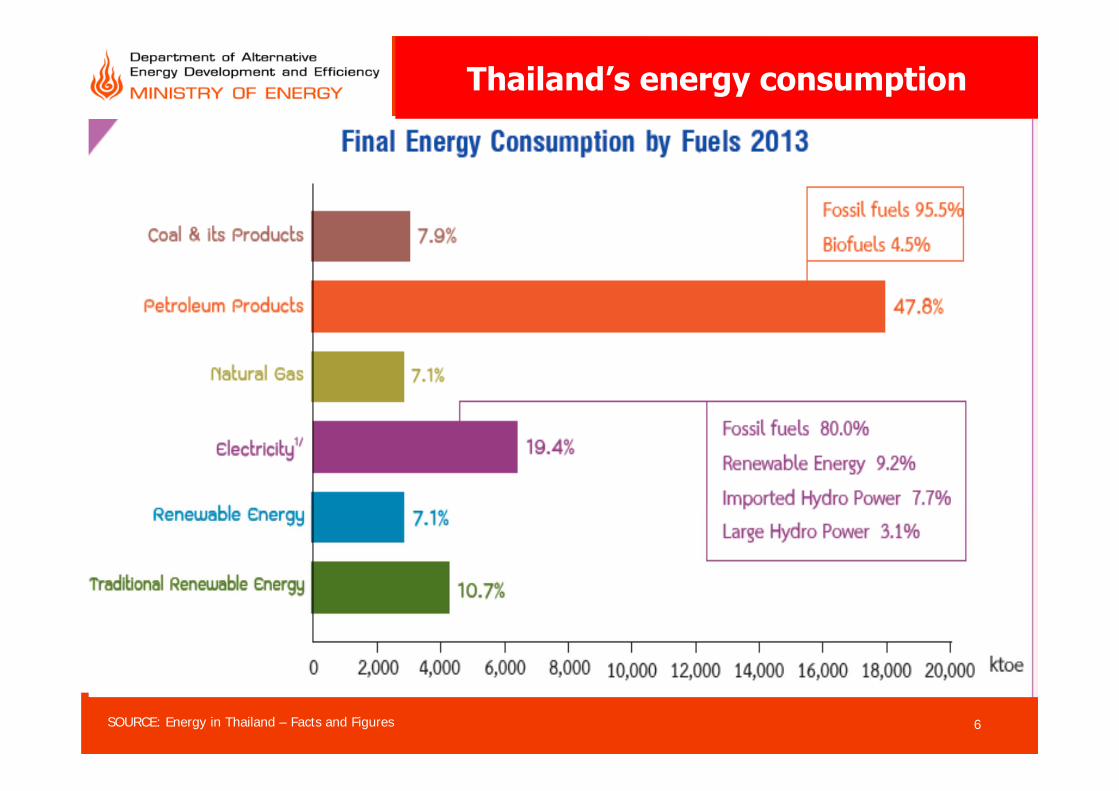

Thailand’s energy consumption

6SOURCE: Energy in Thailand – Facts and Figures

Thailand’s energy consumption

7SOURCE: Energy in Thailand – Facts and Figures

Thailand’s energy supply

• Thailand relies heavily on imported energy

–Import over 90% of crude oil, 80% from the

middle east

–Import 30% of natural gas

–2/3 of commercial energy is imported

2

Electricity Generation

Year GWhChange

GWh (%)

2009 148,358 137 0.1

2010 163,668 15,310 10.3

2011 162,343 -1,325 -0.8

2012 176,973 14,630 9.0

2013 177,398 425 0.2

2014p 180,919 3,520 2.0

p: Preliminary

67%19%

0.1%3% 11%

Natural gasCoal/Lignite

Import and other

HydroOil

Electricity Generation Fuel Mix*

8

2

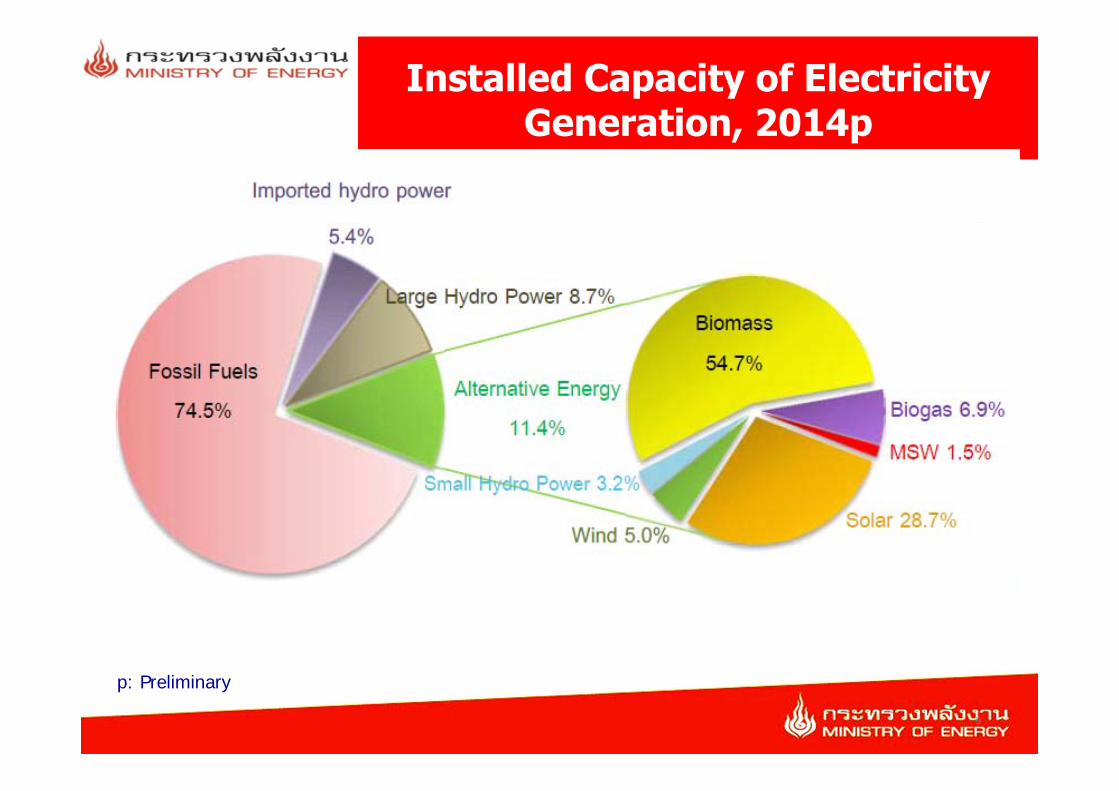

Installed Capacity of Electricity Generation, 2014p

p: Preliminary

9

2

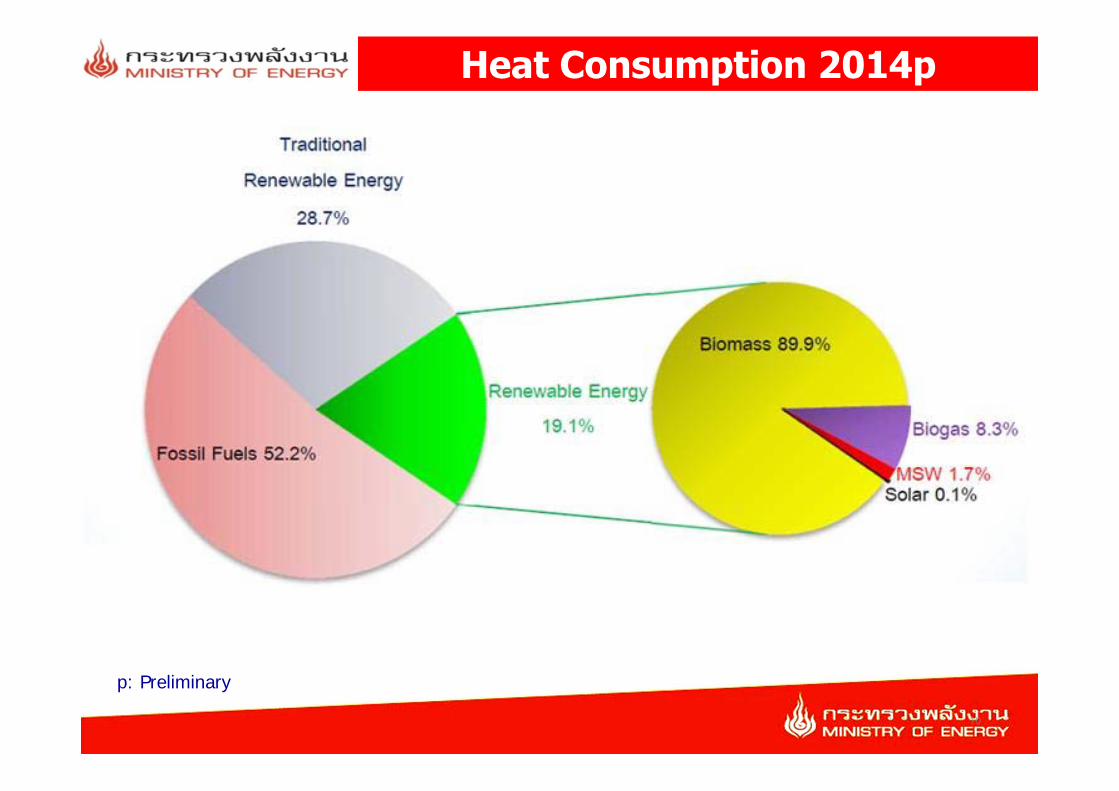

Heat Consumption 2014p

p: Preliminary

10

2. Energy and Renewable Energy Policy in Thailand

11

2

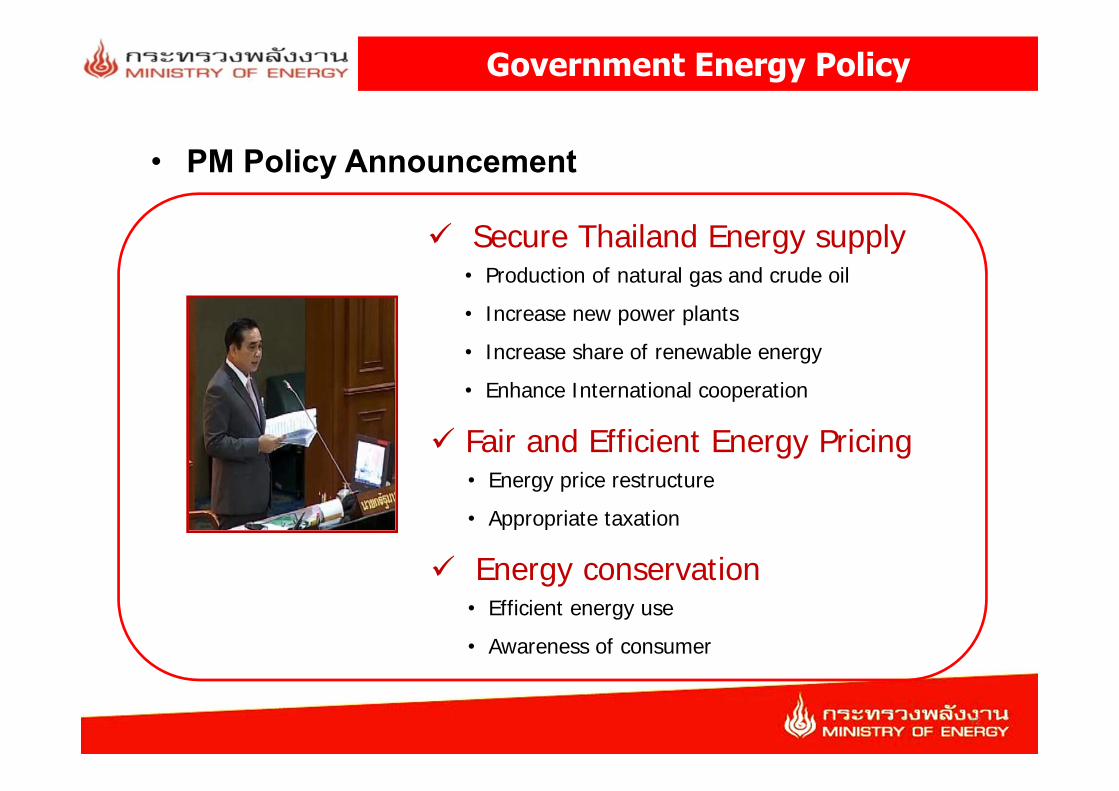

Government Energy Policy

• PM Policy Announcement

Secure Thailand Energy supply• Production of natural gas and crude oil• Increase new power plants• Increase share of renewable energy • Enhance International cooperation

Fair and Efficient Energy Pricing• Energy price restructure• Appropriate taxation

Energy conservation• Efficient energy use• Awareness of consumer

12

Ministry of Energy Strategy for RE

Goal : Security, Affordability, and Sustainability Goal : Security, Affordability, and Sustainability in Energy

• Efficient energy consumption• Increase use of renewable energy

• Energy efficiency development• Education and participation campaign/network• Research and Development of RE technologies• Promote people awareness at community level

13

2

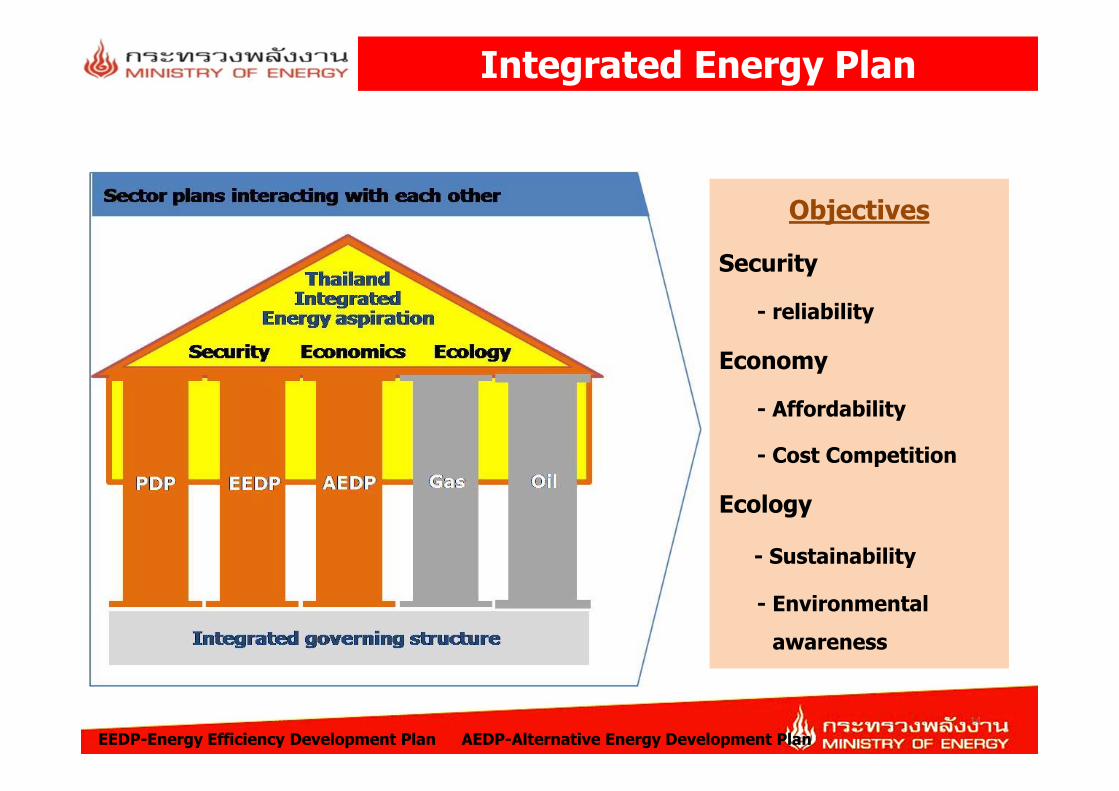

Integrated Energy Plan

Objectives

Security

- reliability

Economy

- Affordability

- Cost Competition

Ecology

- Sustainability

- Environmental awareness

EEDP-Energy Efficiency Development Plan AEDP-Alternative Energy Development Plan 14

Power Development Plan (PDP) 2015

2

GWh

Renewable Energy

Power Generation, classified by fuel type

18 %

2 %

15 %

37 %

17 %

6 %5 %

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

Domestic Hydropower

Imported Hydropower

Natural Gas

Imported CoalLignite

15

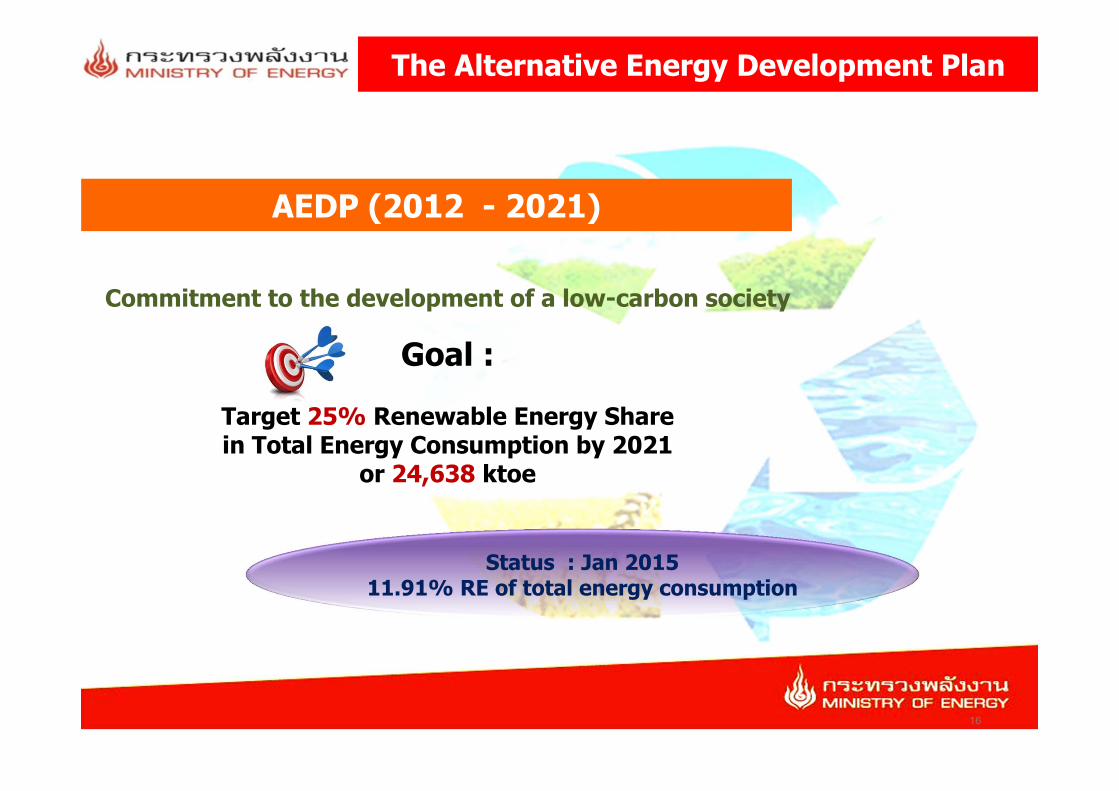

The Alternative Energy Development Plan

Commitment to the development of a low-carbon society

Goal :

Target 25% Renewable Energy Share in Total Energy Consumption by 2021

or 24,638 ktoe

AEDP (2012 - 2021)

Status : Jan 201511.91% RE of total energy consumption

16

2

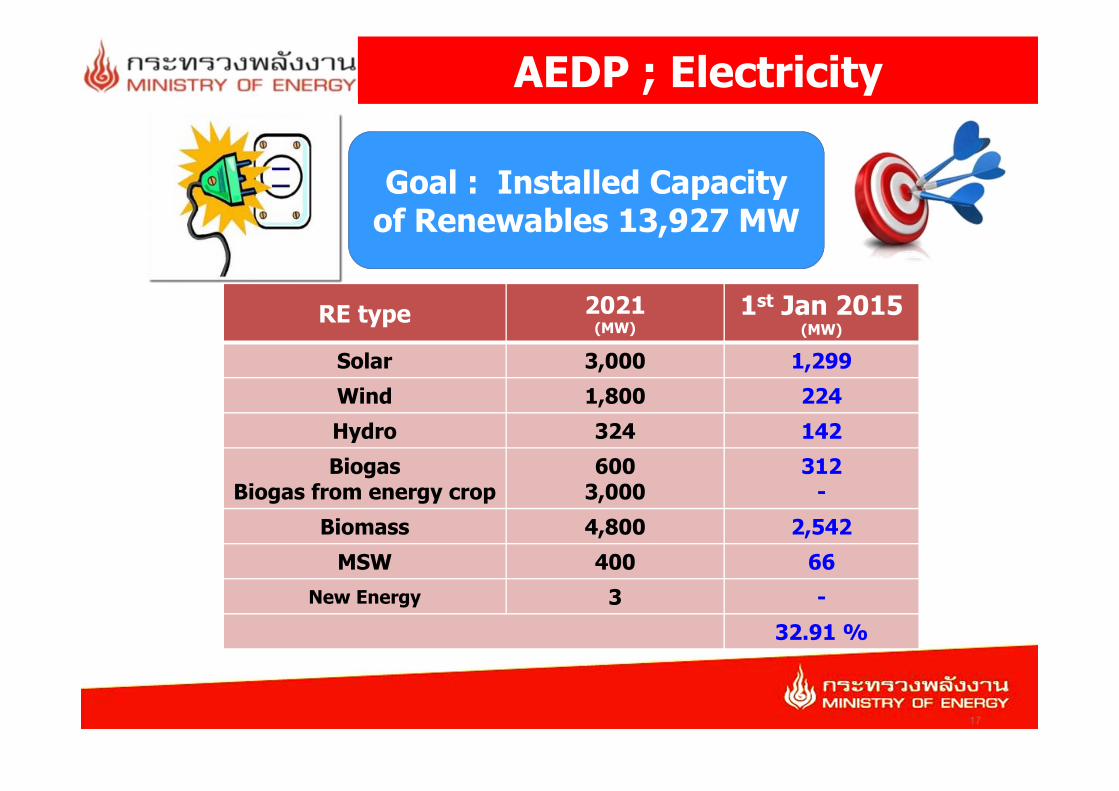

AEDP ; Electricity

Goal : Installed Capacity of Renewables 13,927 MW

RE type 2021 (MW)

1st Jan 2015(MW)

Solar 3,000 1,299Wind 1,800 224Hydro 324 142Biogas

Biogas from energy crop600

3,000312

-Biomass 4,800 2,542

MSW 400 66New Energy 3 -

32.91 %

17

2

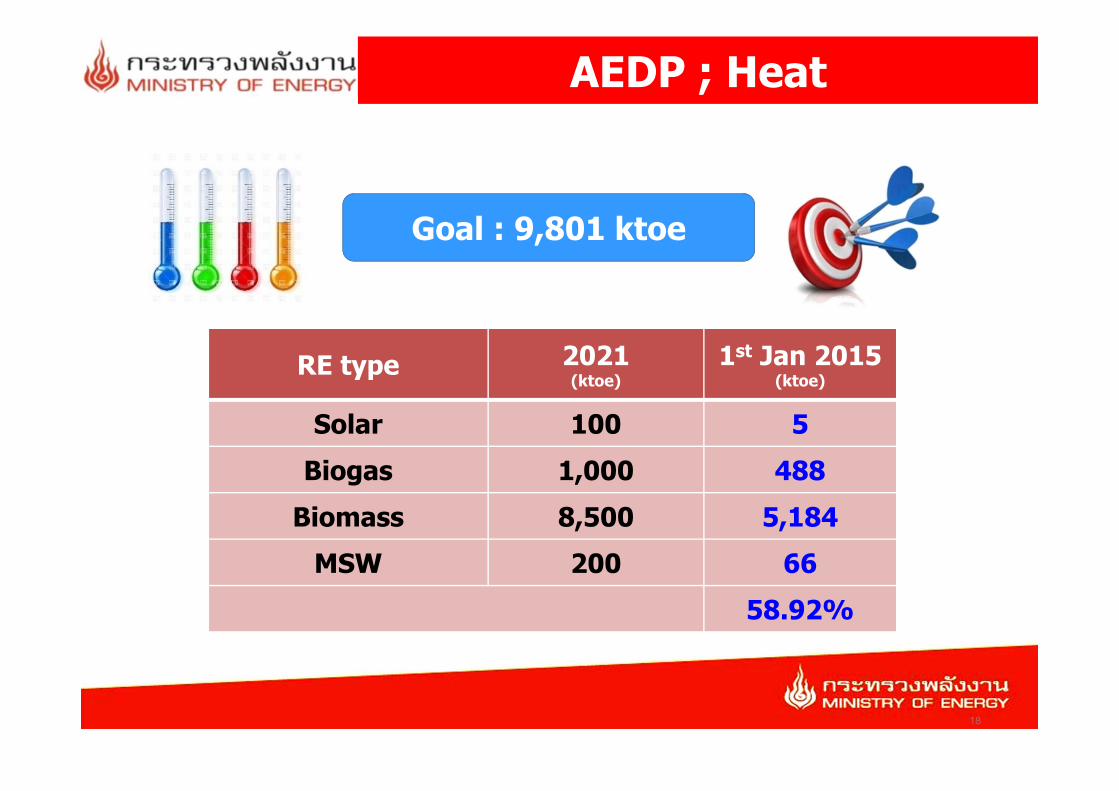

AEDP ; Heat

Goal : 9,801 ktoe

RE type 2021 (ktoe)

1st Jan 2015(ktoe)

Solar 100 5Biogas 1,000 488

Biomass 8,500 5,184MSW 200 66

58.92%

18

2

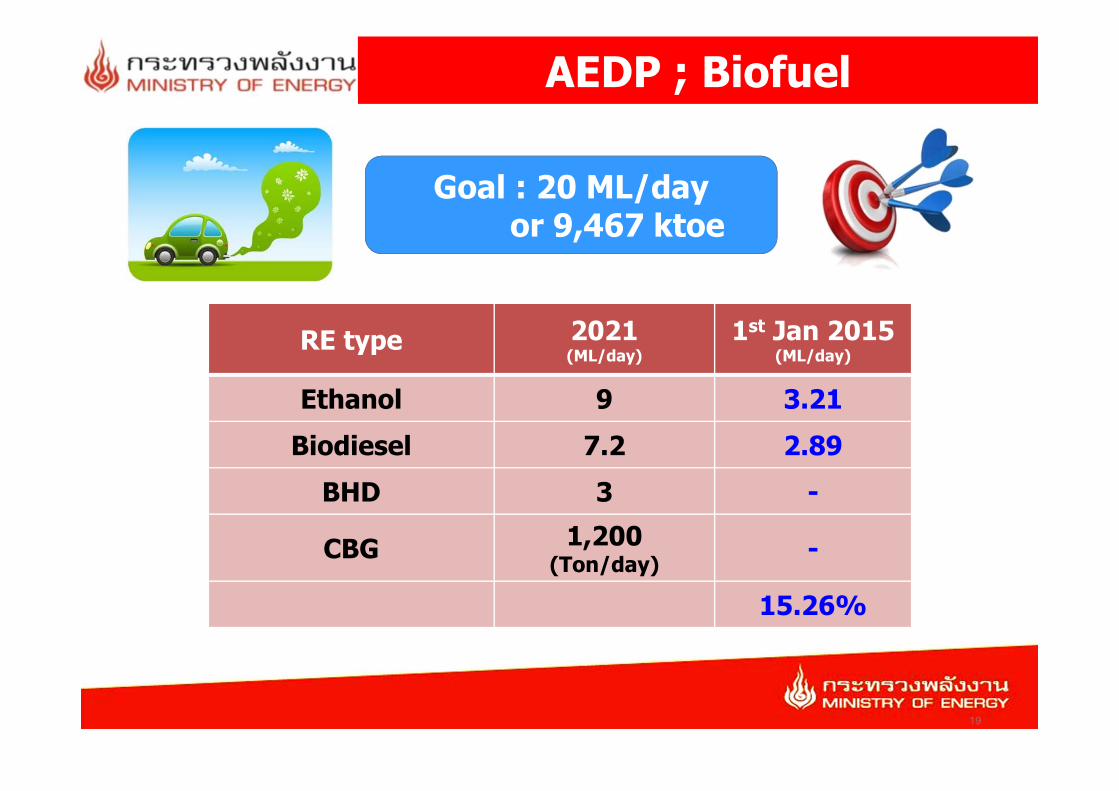

AEDP ; Biofuel

Goal : 20 ML/dayor 9,467 ktoe

RE type 2021 (ML/day)

1st Jan 2015(ML/day)

Ethanol 9 3.21Biodiesel 7.2 2.89

BHD 3 -

CBG 1,200(Ton/day) -

15.26%

19

2

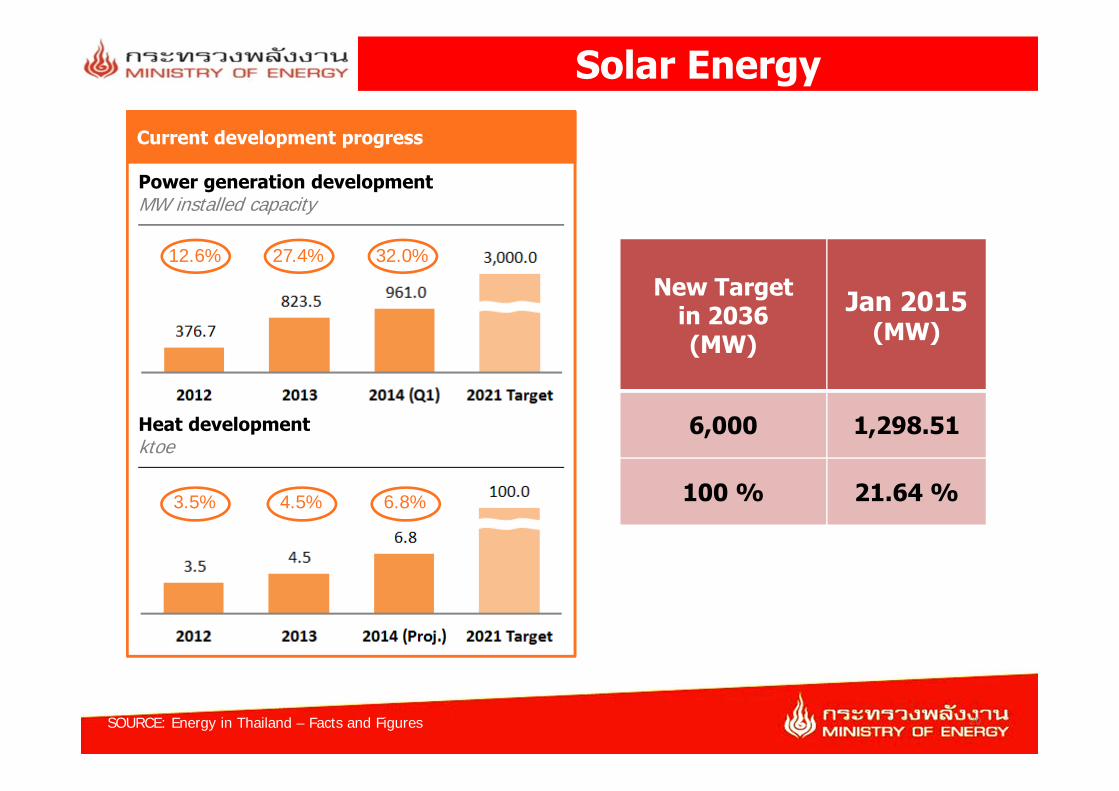

Solar EnergyCurrent development progress

SOURCE: Energy in Thailand – Facts and Figures

Power generation developmentMW installed capacity

Heat developmentktoe

27.4% 32.0%

3.5% 4.5% 6.8%

12.6%New Target

in 2036(MW)

Jan 2015(MW)

6,000 1,298.51

100 % 21.64 %

20

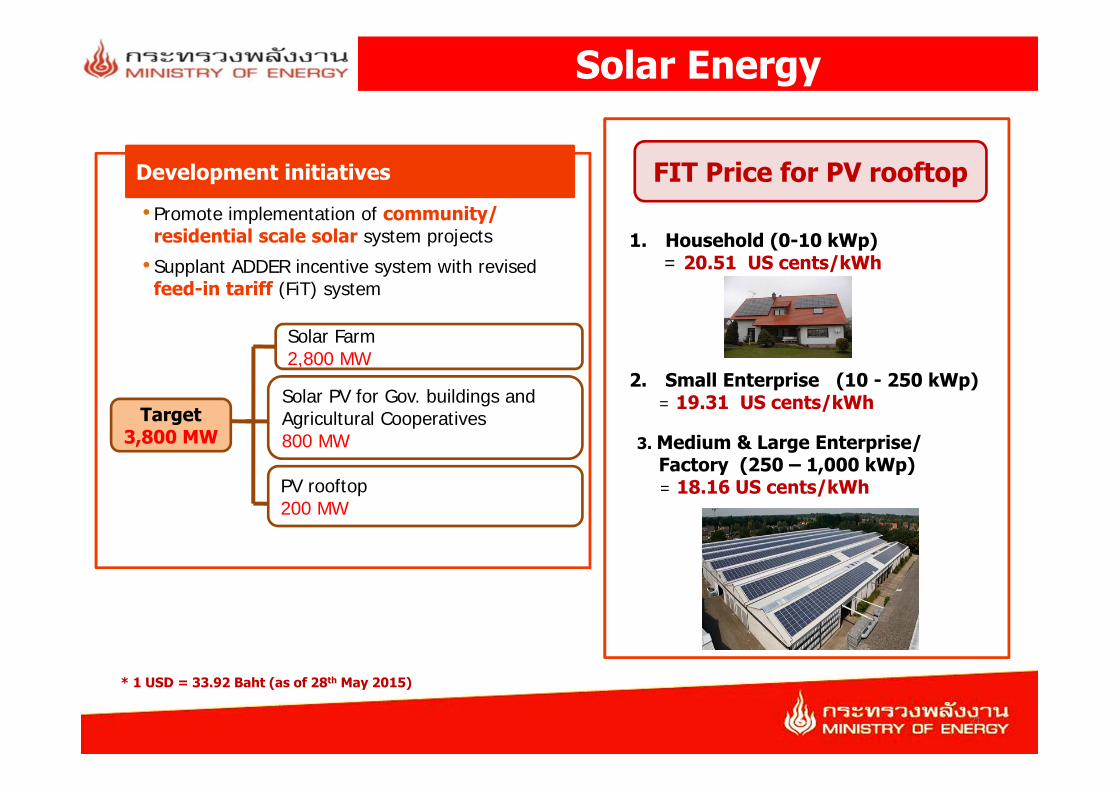

Solar Energy

Development initiatives

• Promote implementation of community/ residential scale solar system projects• Supplant ADDER incentive system with revised

feed-in tariff (FiT) system

Solar Farm2,800 MW

Solar PV for Gov. buildings and Agricultural Cooperatives800 MW

Target3,800 MW

PV rooftop200 MW

FIT Price for PV rooftop

1. Household (0-10 kWp)= 20.51 US cents/kWh

2. Small Enterprise (10 - 250 kWp)= 19.31 US cents/kWh

3. Medium & Large Enterprise/Factory (250 – 1,000 kWp)= 18.16 US cents/kWh

* 1 USD = 33.92 Baht (as of 28th May 2015)

21

2

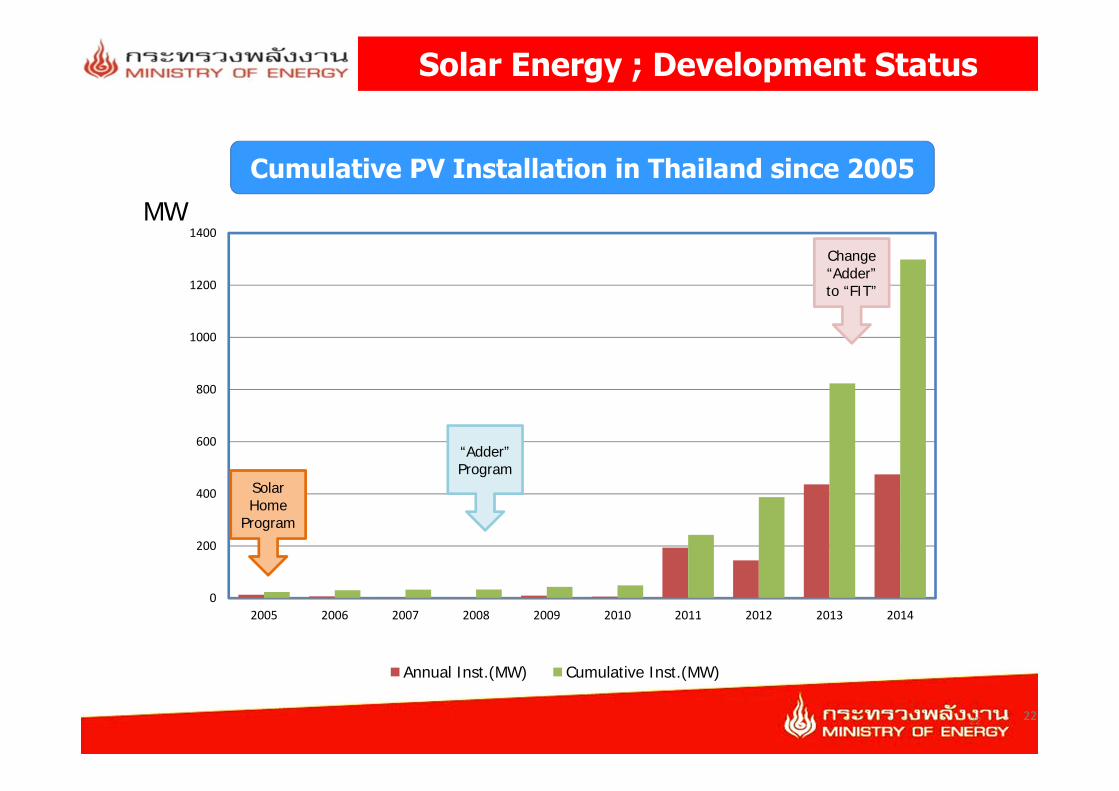

Solar Energy ; Development Status

22

0

200

400

600

800

1000

1200

1400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Annual Inst.(MW) Cumulative Inst.(MW)

Cumulative PV Installation in Thailand since 2005MW

Solar Home

Program

“Adder”Program

Change “Adder”to “FIT”

22

2

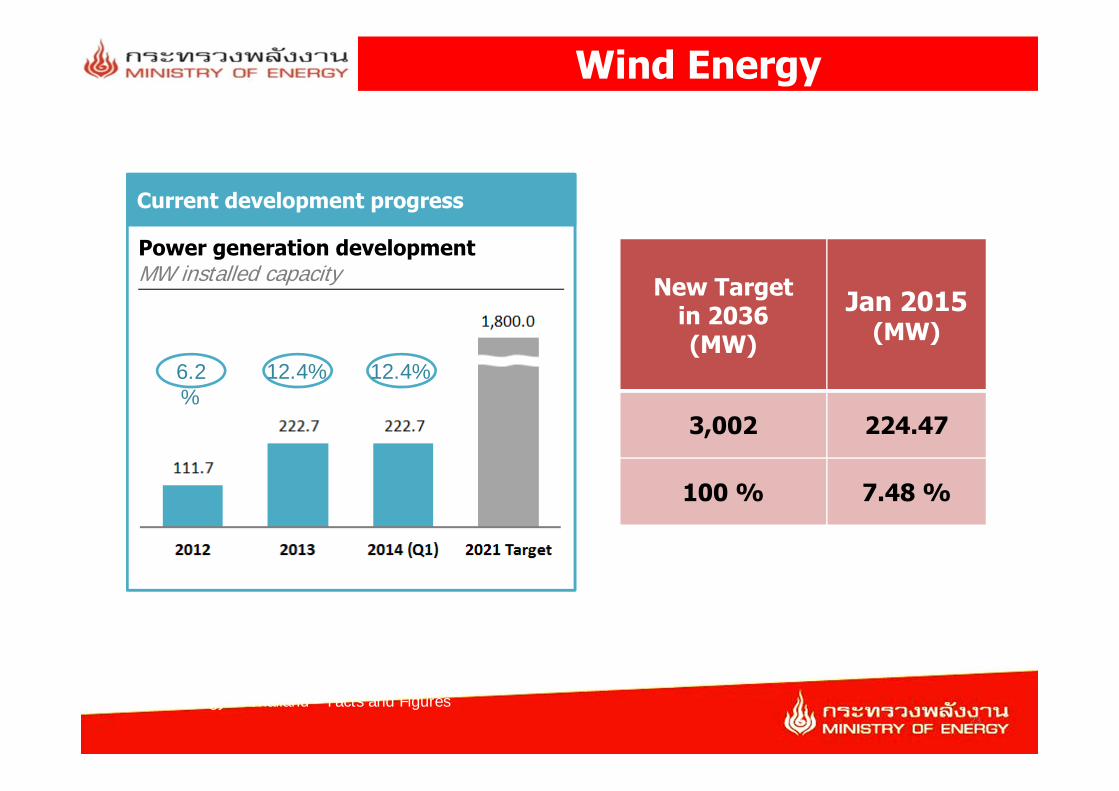

Wind Energy

Current development progress

Power generation developmentMW installed capacity

SOURCE: Energy in Thailand – Facts and Figures

6.2%

12.4% 12.4%

New Target in 2036(MW)

Jan 2015(MW)

3,002 224.47

100 % 7.48 %

23

2

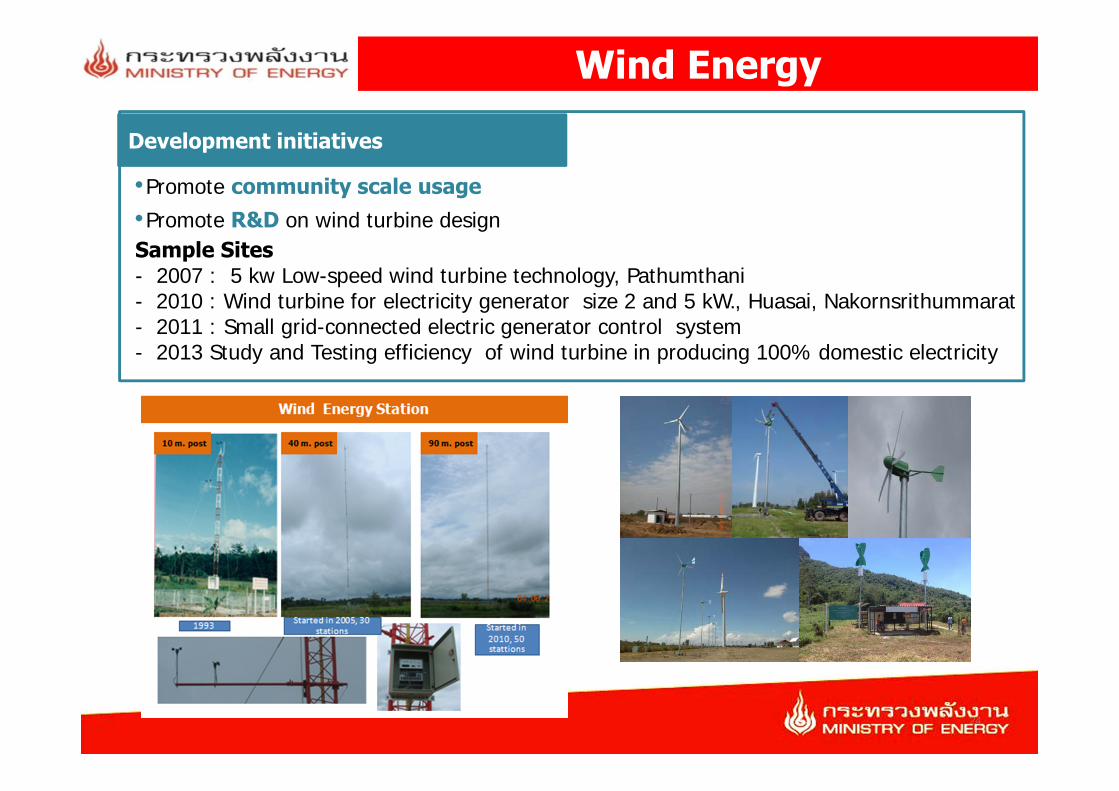

Wind Energy

•Promote community scale usage•Promote R&D on wind turbine design

Development initiatives

Sample Sites- 2007 : 5 kw Low-speed wind turbine technology, Pathumthani- 2010 : Wind turbine for electricity generator size 2 and 5 kW., Huasai, Nakornsrithummarat- 2011 : Small grid-connected electric generator control system- 2013 Study and Testing efficiency of wind turbine in producing 100% domestic electricity

24

2

Wind Energy

Wind Farm in Korat

25

2

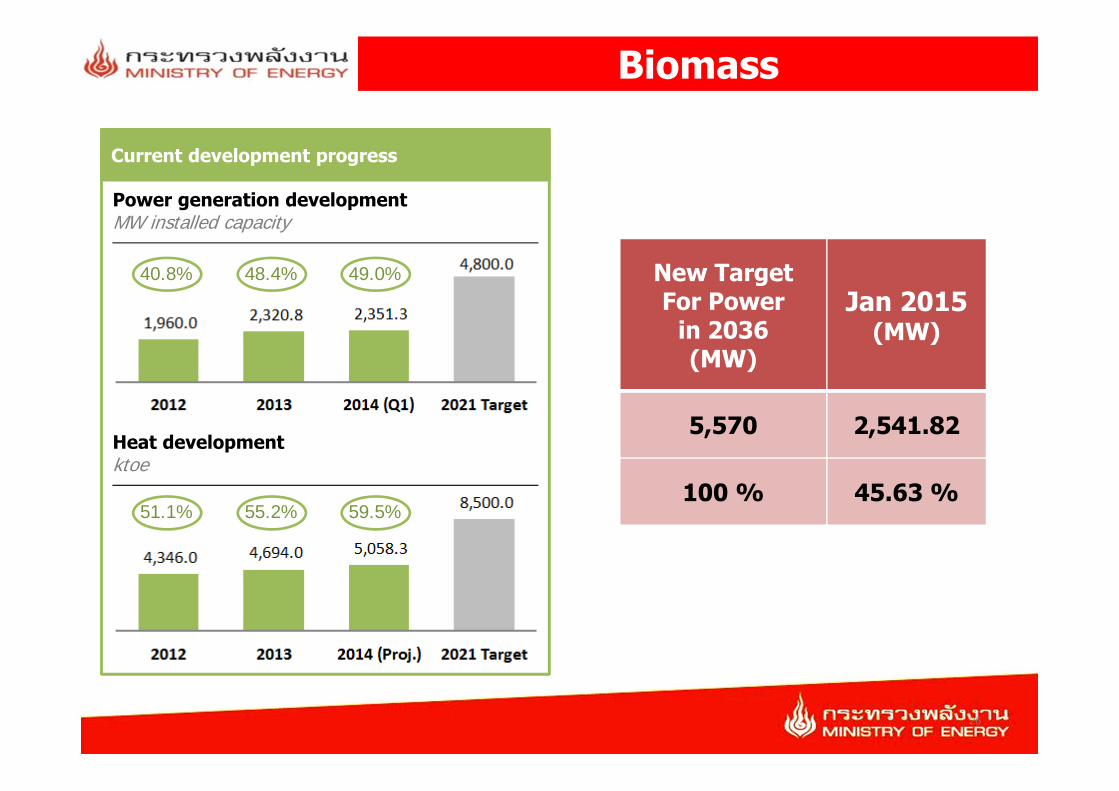

Biomass

Current development progress

Power generation developmentMW installed capacity

Heat developmentktoe

48.4% 49.0%40.8%

55.2% 59.5%51.1%

New Target For Power

in 2036(MW)

Jan 2015(MW)

5,570 2,541.82

100 % 45.63 %

26

2

Biomass

Development initiatives

• Promote fast growing trees

• Develop biomass pellets

• Develop advanced gasifierand gas engine technology

• Promote high pressure boilers

• Promote Distributed Green Generation (DGG) –

• Develop transmission and distribution infrastructure

27

2

BiogasCurrent development progress

Power generation developmentMW installed capacity

Heat developmentktoe

7.4% 7.6%5.4%

49.5% 52.8%45.8%

New Target in 2036(MW)

Jan 2015(MW)

1,280 311.50

100 % 24.33 %

28

BiogasDevelopment initiatives

•Promote household biogas

•Support community self-management

•Alternative feedstock resources

•Promote compressed bio-methane gas (CBG) from biomass and energy crops

•Develop regulations for biogas safety standards

•Promote public relations and awareness

29

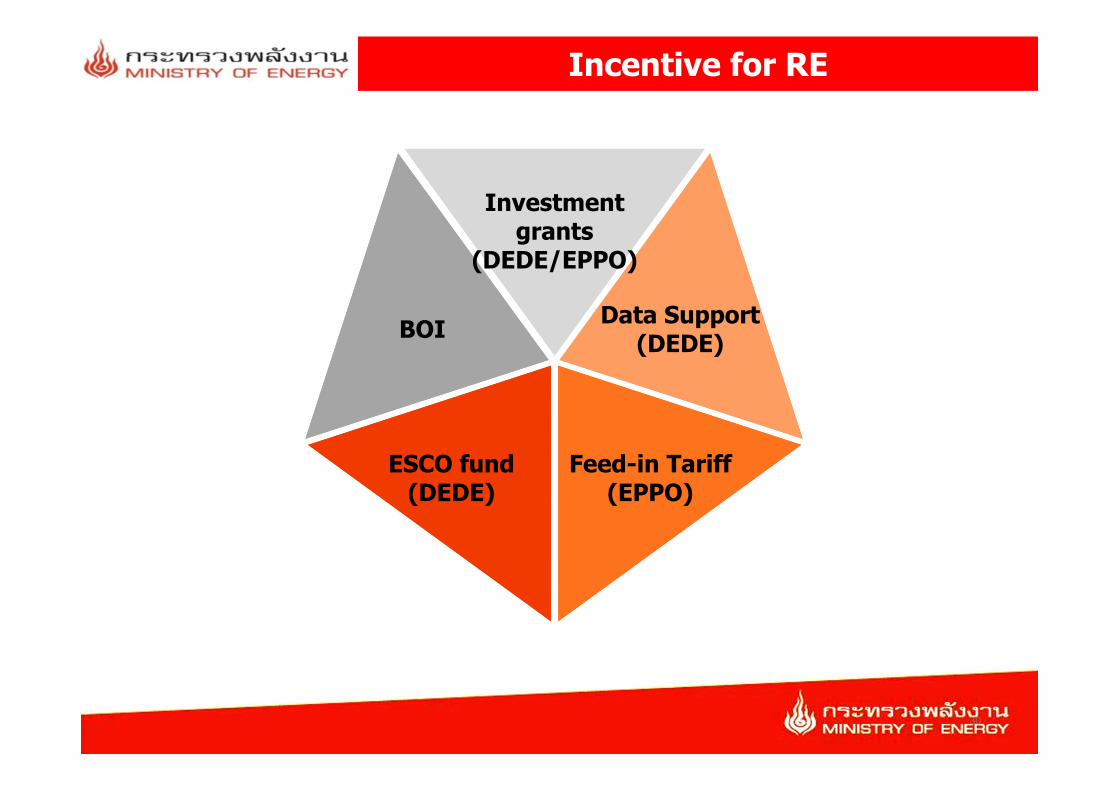

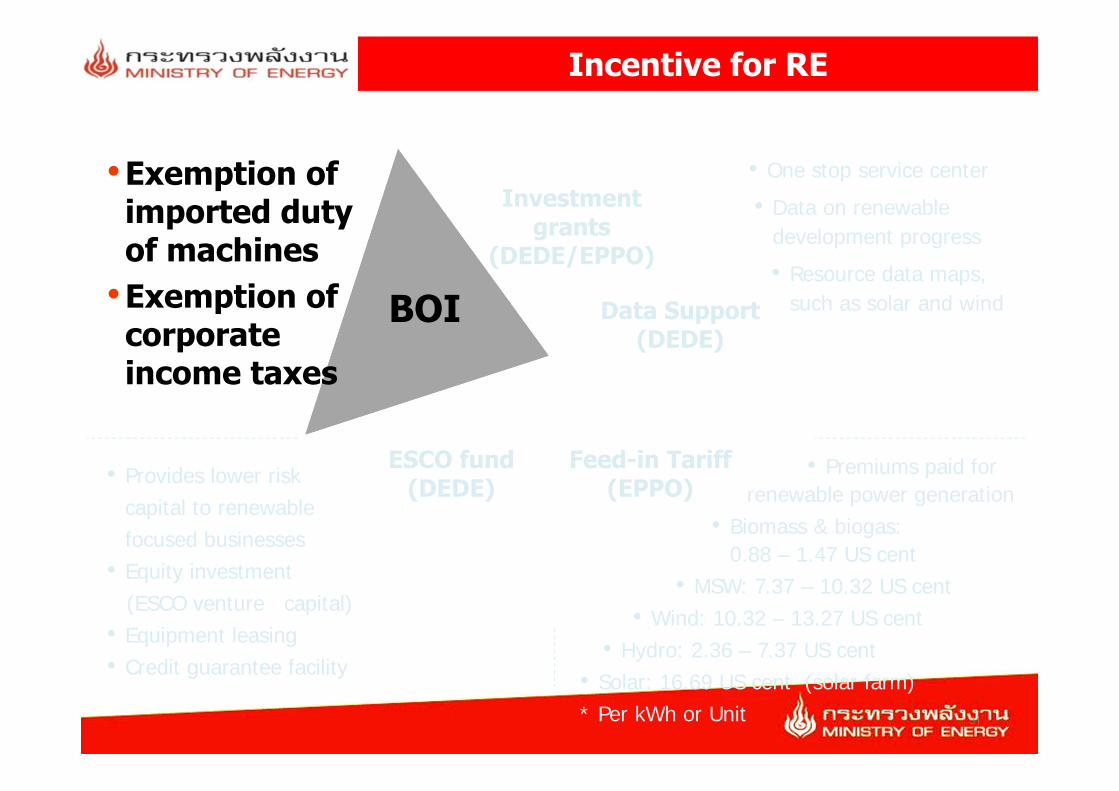

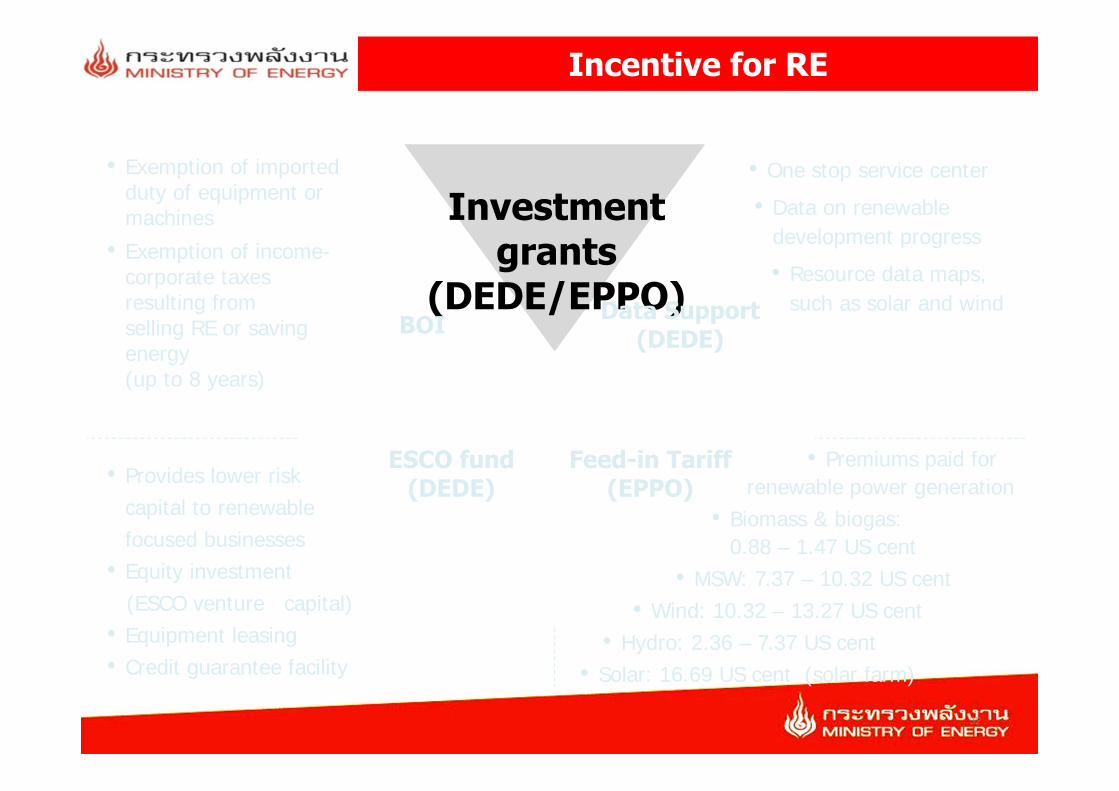

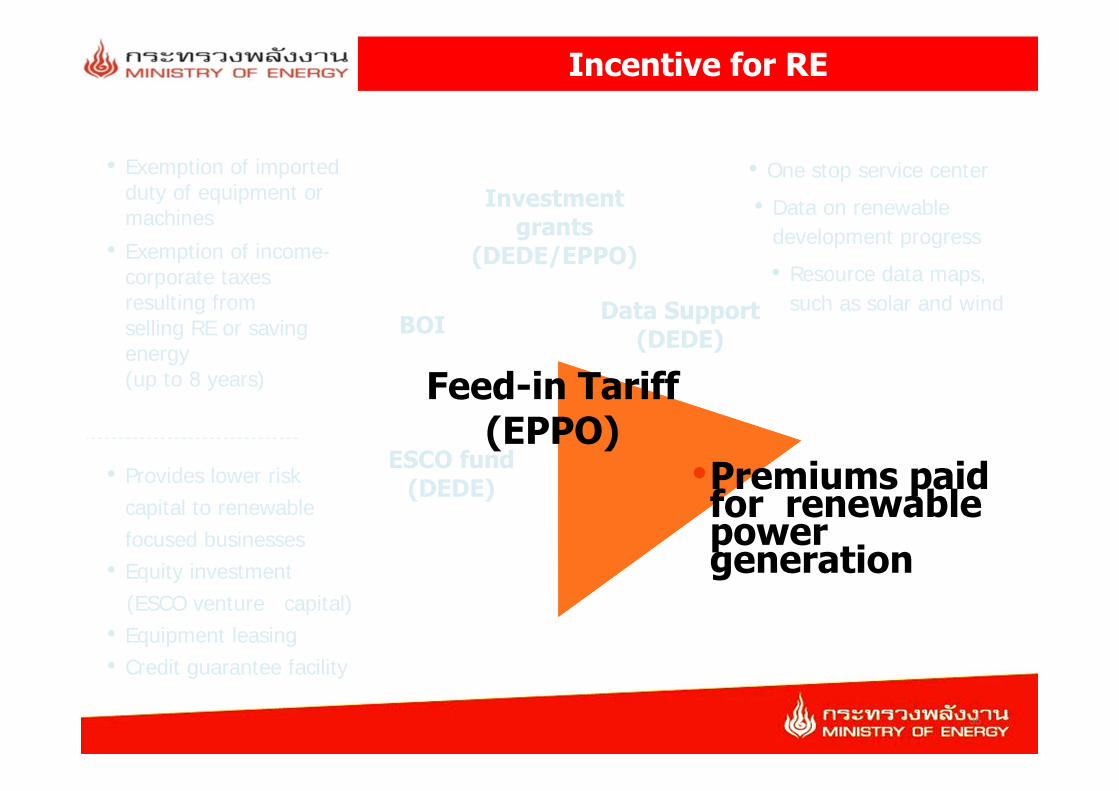

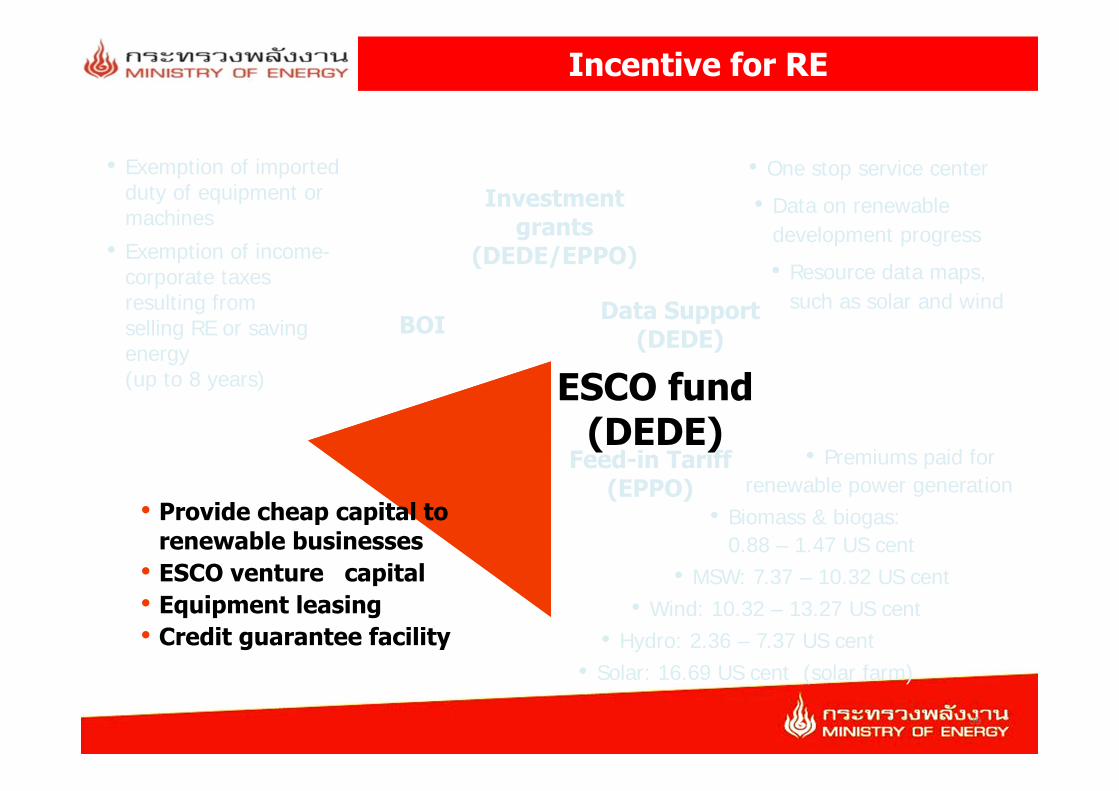

Incentive for RE

Investment grants

(DEDE/EPPO)

BOI Data Support (DEDE)

Feed-in Tariff(EPPO)

ESCO fund(DEDE)

30

2

Incentive for RE

Investment grants

(DEDE/EPPO)

BOI Data Support (DEDE)

Feed-in Tariff(EPPO)

ESCO fund(DEDE)

•Exemption of imported duty of machines•Exemption of corporate income taxes

• One stop service center• Data on renewable

development progress• Resource data maps,

such as solar and wind

• Provides lower riskcapital to renewable focused businesses

• Equity investment (ESCO venture capital)

• Equipment leasing • Credit guarantee facility

• Premiums paid forrenewable power generation

• Biomass & biogas: 0.88 – 1.47 US cent

• MSW: 7.37 – 10.32 US cent• Wind: 10.32 – 13.27 US cent

• Hydro: 2.36 – 7.37 US cent• Solar: 16.69 US cent (solar farm)* Per kWh or Unit 31

2

Incentive for RE

Investment grants

(DEDE/EPPO)BOI Data Support

(DEDE)

Feed-in Tariff(EPPO)

ESCO fund(DEDE)

• Exemption of imported duty of equipment or machines

• Exemption of income-corporate taxes resulting from selling RE or savingenergy (up to 8 years)

• One stop service center• Data on renewable

development progress• Resource data maps,

such as solar and wind

• Provides lower riskcapital to renewable focused businesses

• Equity investment (ESCO venture capital)

• Equipment leasing • Credit guarantee facility

• Premiums paid forrenewable power generation

• Biomass & biogas: 0.88 – 1.47 US cent

• MSW: 7.37 – 10.32 US cent• Wind: 10.32 – 13.27 US cent

• Hydro: 2.36 – 7.37 US cent• Solar: 16.69 US cent (solar farm)

32

2

Incentive for RE

Investment grants

(DEDE/EPPO)

BOI Data Support (DEDE)

Feed-in Tariff(EPPO)

ESCO fund(DEDE)

• Exemption of imported duty of equipment or machines

• Exemption of income-corporate taxes resulting from selling RE or savingenergy (up to 8 years)

•One stop service •Data on renewables

• Provides lower riskcapital to renewable focused businesses

• Equity investment (ESCO venture capital)

• Equipment leasing • Credit guarantee facility

• Premiums paid forrenewable power generation

• Biomass & biogas: 0.88 – 1.47 US cent

• MSW: 7.37 – 10.32 US cent• Wind: 10.32 – 13.27 US cent

• Hydro: 2.36 – 7.37 US cent• Solar: 16.69 US cent (solar farm)

33

2

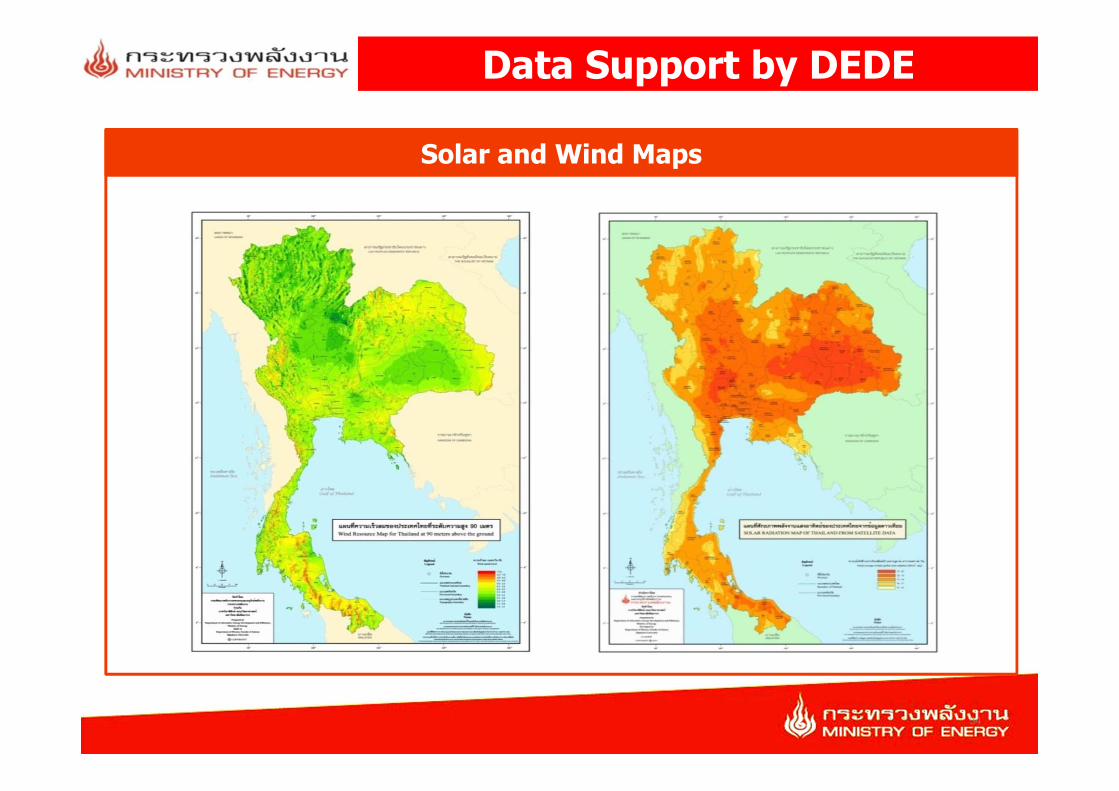

Data Support by DEDE

Solar and Wind Maps

34

2

Incentive for RE

Investment grants

(DEDE/EPPO)

BOI Data Support (DEDE)

Feed-in Tariff(EPPO)

ESCO fund(DEDE)

• Exemption of imported duty of equipment or machines

• Exemption of income-corporate taxes resulting from selling RE or savingenergy (up to 8 years)

• One stop service center• Data on renewable

development progress• Resource data maps,

such as solar and wind

• Provides lower riskcapital to renewable focused businesses

• Equity investment (ESCO venture capital)

• Equipment leasing • Credit guarantee facility

•Premiums paid for renewable power generation

35

2

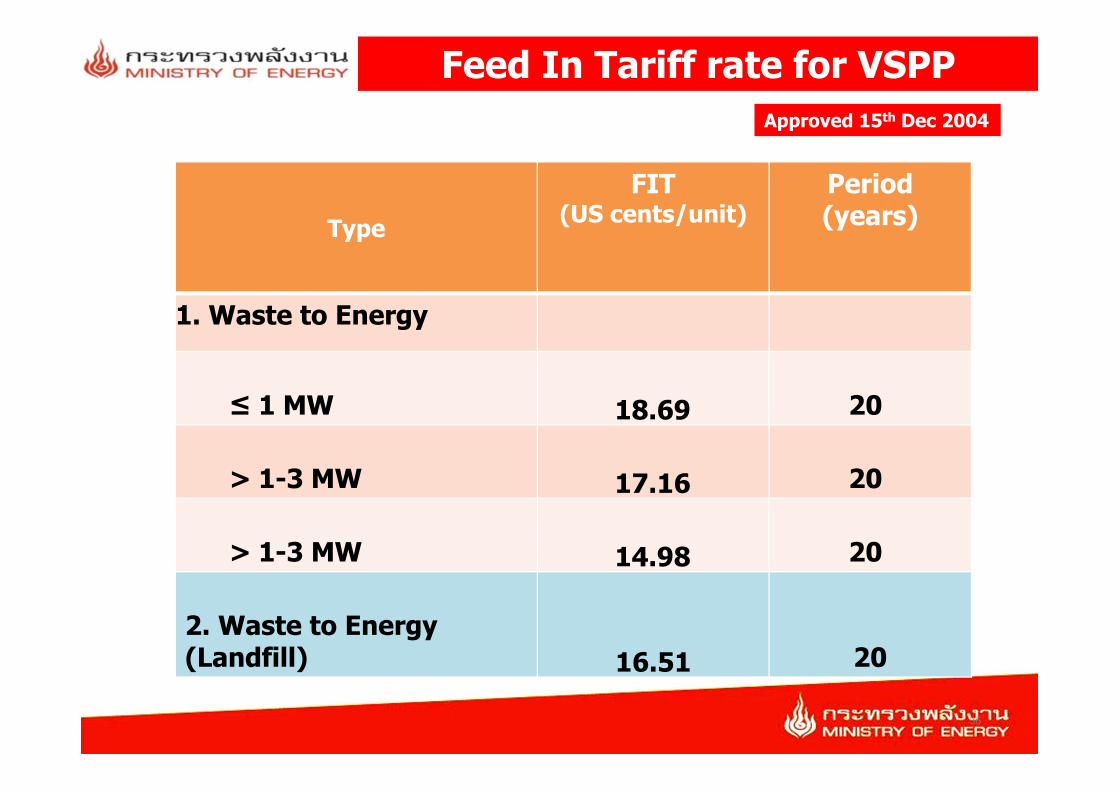

Feed In Tariff rate for VSPPApproved 15th Dec 2004

TypeFIT

(US cents/unit)Period(years)

1. Waste to Energy

≤ 1 MW 18.69 20

> 1-3 MW 17.16 20

> 1-3 MW 14.98 20

2. Waste to Energy (Landfill) 16.51 20

36

2

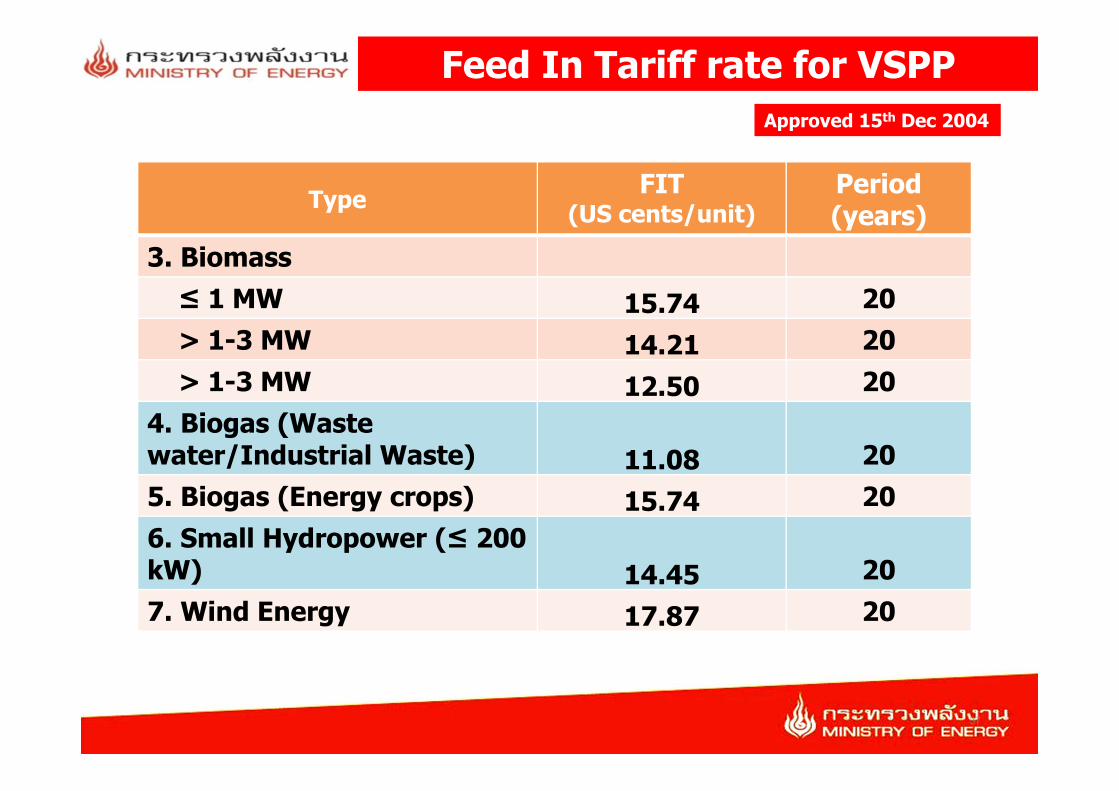

Feed In Tariff rate for VSPPApproved 15th Dec 2004

Type FIT (US cents/unit)

Period(years)

3. Biomass≤ 1 MW 15.74 20> 1-3 MW 14.21 20> 1-3 MW 12.50 20

4. Biogas (Waste water/Industrial Waste) 11.08 205. Biogas (Energy crops) 15.74 206. Small Hydropower (≤ 200 kW) 14.45 207. Wind Energy 17.87 20

37

2

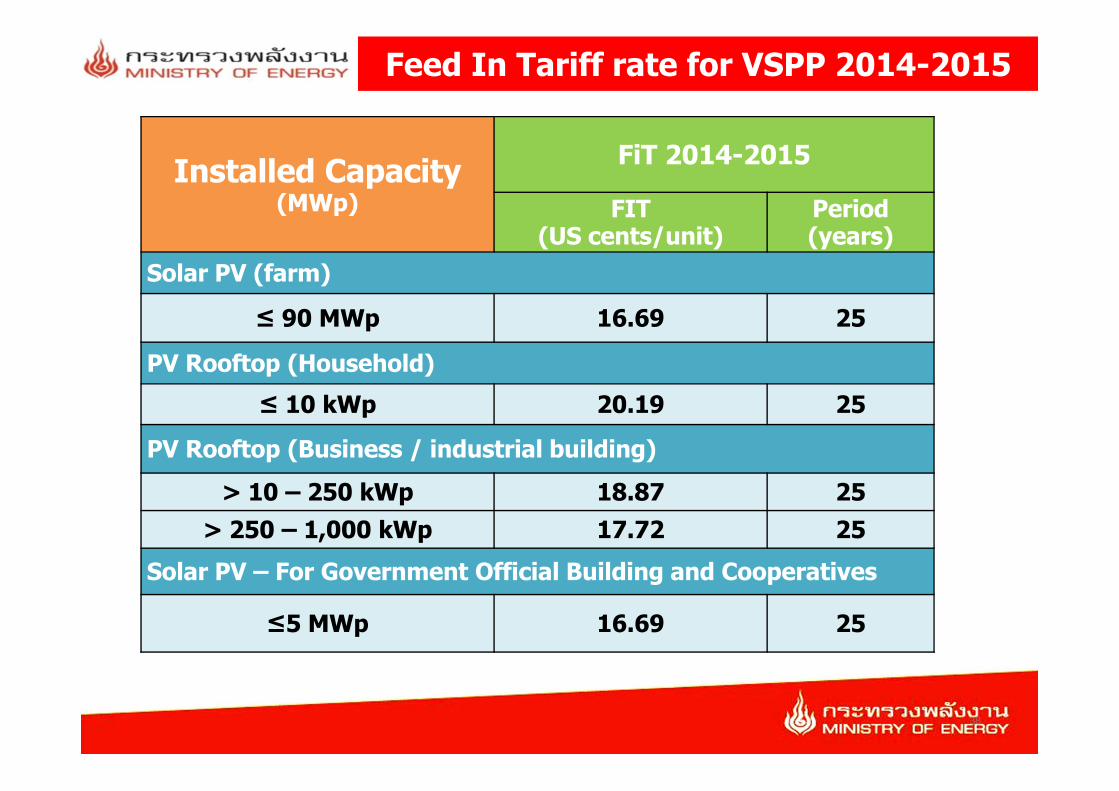

Feed In Tariff rate for VSPP 2014-2015

Installed Capacity (MWp)

FiT 2014-2015

FIT(US cents/unit)

Period (years)

Solar PV (farm)

≤ 90 MWp 16.69 25

PV Rooftop (Household)≤ 10 kWp 20.19 25

PV Rooftop (Business / industrial building)> 10 – 250 kWp 18.87 25

> 250 – 1,000 kWp 17.72 25 Solar PV – For Government Official Building and Cooperatives

≤5 MWp 16.69 25

38

2

Incentive for RE

Investment grants

(DEDE/EPPO)

BOI Data Support (DEDE)

Feed-in Tariff(EPPO)

ESCO fund(DEDE)

• Exemption of imported duty of equipment or machines

• Exemption of income-corporate taxes resulting from selling RE or savingenergy (up to 8 years)

• One stop service center• Data on renewable

development progress• Resource data maps,

such as solar and wind

• Provide cheap capital to renewable businesses

• ESCO venture capital• Equipment leasing • Credit guarantee facility

• Premiums paid forrenewable power generation

• Biomass & biogas: 0.88 – 1.47 US cent

• MSW: 7.37 – 10.32 US cent• Wind: 10.32 – 13.27 US cent

• Hydro: 2.36 – 7.37 US cent• Solar: 16.69 US cent (solar farm)

39

2

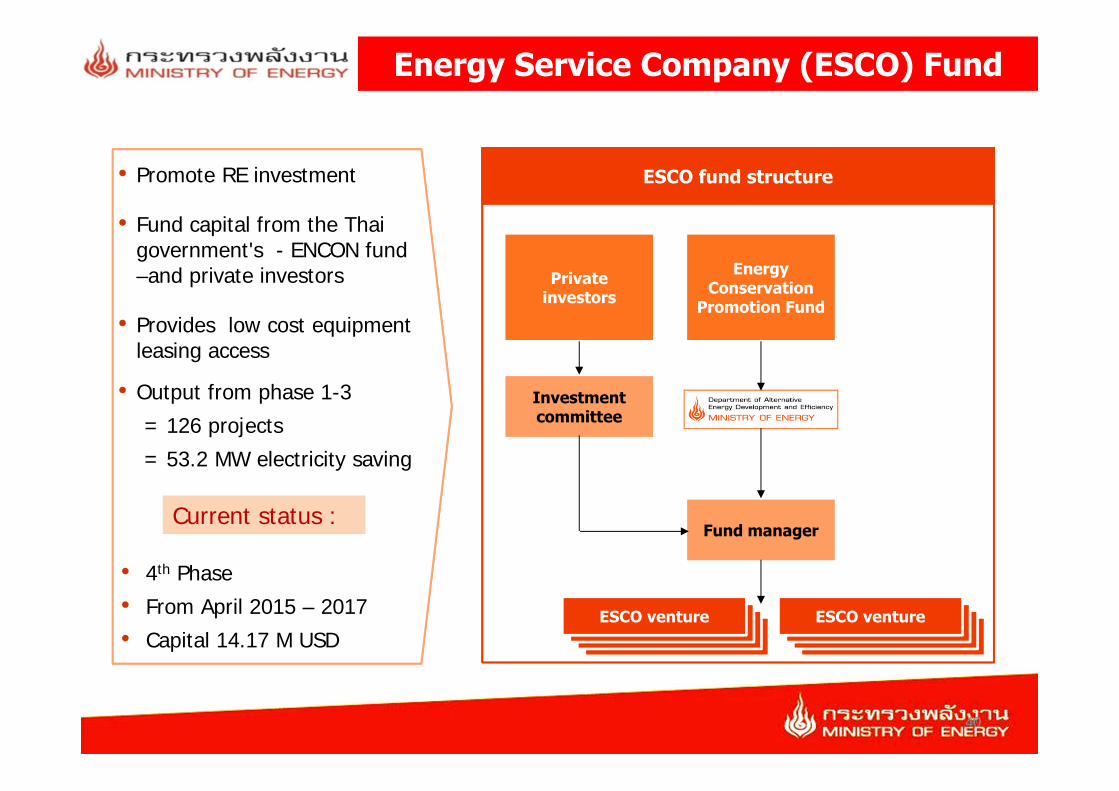

Energy Service Company (ESCO) Fund

40

• Promote RE investment

• Fund capital from the Thai government's - ENCON fund –and private investors

• Provides low cost equipment leasing access

• Output from phase 1-3= 126 projects = 53.2 MW electricity saving

ESCO fund structure

ESCO ventureESCO ventureESCO ventureESCO ventureESCO ventureESCO ventureESCO ventureESCO venture

Fund manager

Investment committee

Private investors

Energy Conservation

Promotion Fund

Current status :

• 4th Phase• From April 2015 – 2017• Capital 14.17 M USD

40

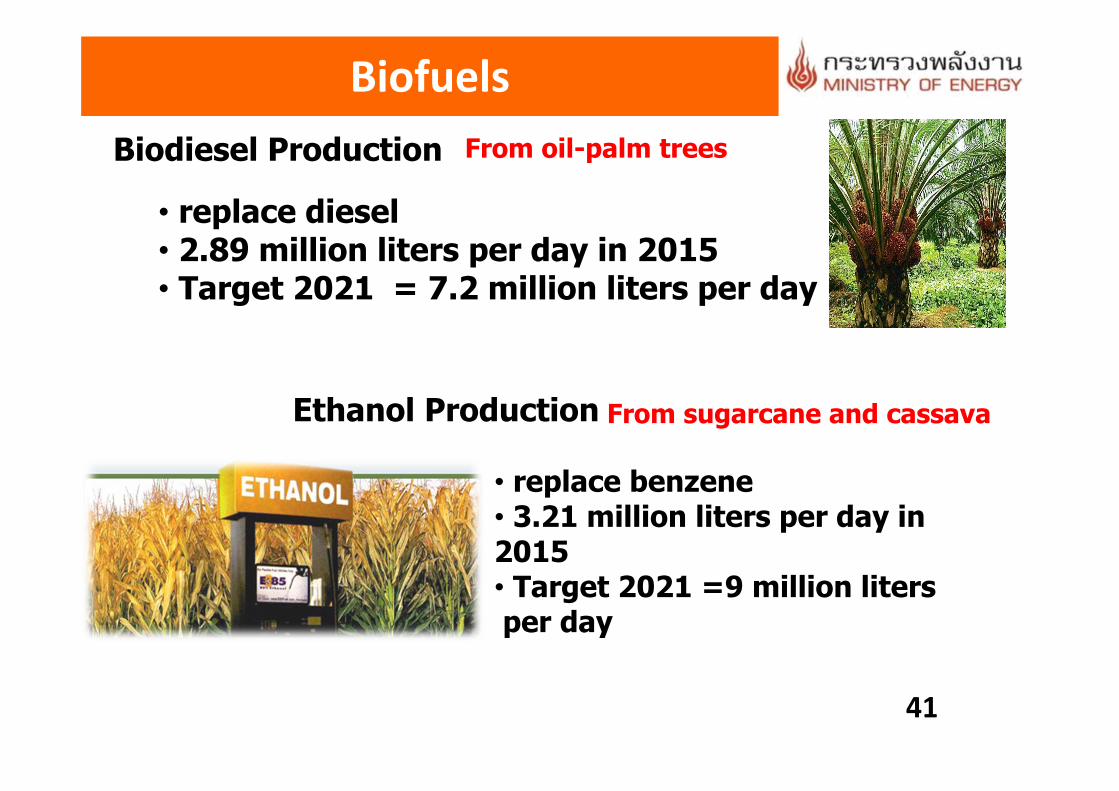

BiofuelsBiodiesel Production

• replace diesel• 2.89 million liters per day in 2015• Target 2021 = 7.2 million liters per day

From oil-palm trees

41

• replace benzene• 3.21 million liters per day in 2015• Target 2021 =9 million liters per day

Ethanol Production From sugarcane and cassava

Biofuel ; Ethanol

Development initiatives

• Continue to increase the share of “Gasohol” on the market (current share, including E10, E20, and E85 is 92%)

E10 stations are all over

Thailand

Sources - DOEB

194 271542

830

1311

2045

2665

4 5 10 38 67280

596

2008 2009 2010 2011 2012 2013 2014

E20 stations E85 stations

42

2

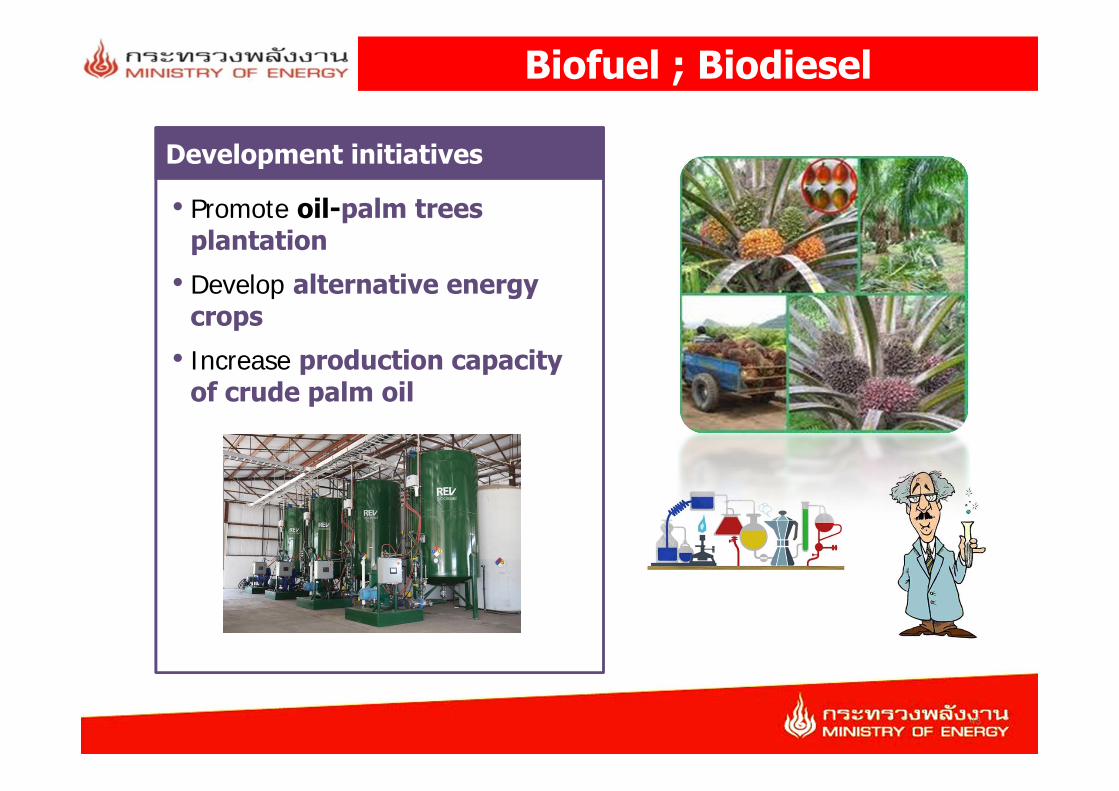

Biofuel ; Biodiesel

Development initiatives

• Promote oil-palm trees plantation• Develop alternative energy

crops• Increase production capacity

of crude palm oil

43

3. Challenges for RE Project Development

44

2

Challenges for RE project development

Barrier to Investment

• High investment cost

• Limited grid capacity

45

2

Challenges for RE project development

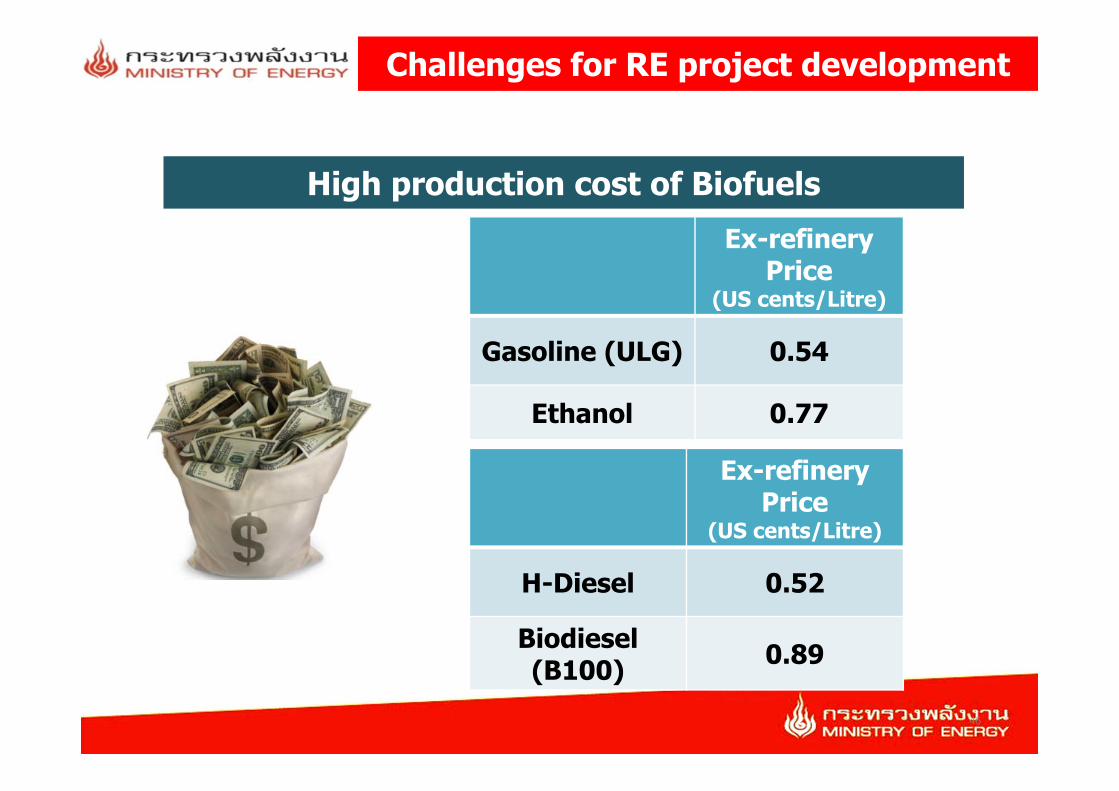

High production cost of BiofuelsEx-refinery

Price(US cents/Litre)

Gasoline (ULG) 0.54

Ethanol 0.77

Ex-refineryPrice

(US cents/Litre)

H-Diesel 0.52

Biodiesel (B100) 0.89

46

2

Challenges for RE project development

Public acceptance• Lack of support/ acceptance for power plants from nearby communities

47

2

Challenges for RE project development

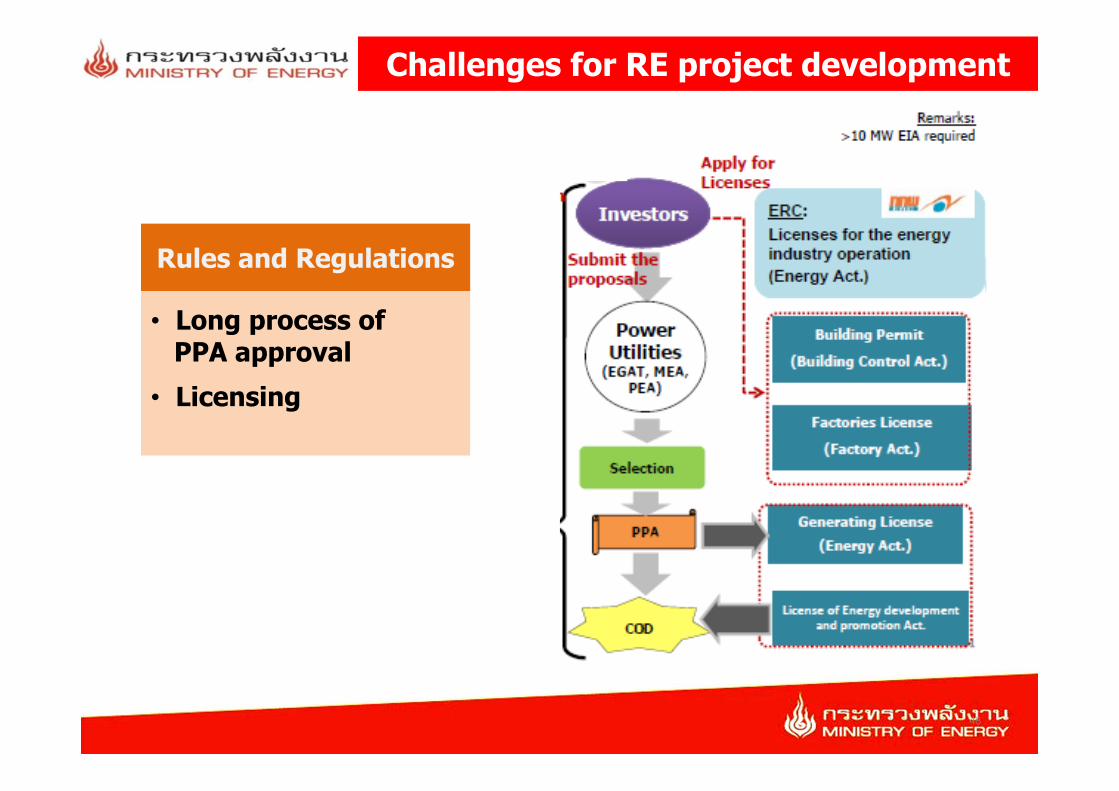

Rules and Regulations

• Long process of PPA approval

• Licensing

48

2

Challenges for RE project development

Supply of Feedstock

• Uncertainty of RE supply resources• Inefficient feedstock logistic/management system• Food VS Energy Issue

49

4. Way forward for future RE Development

50

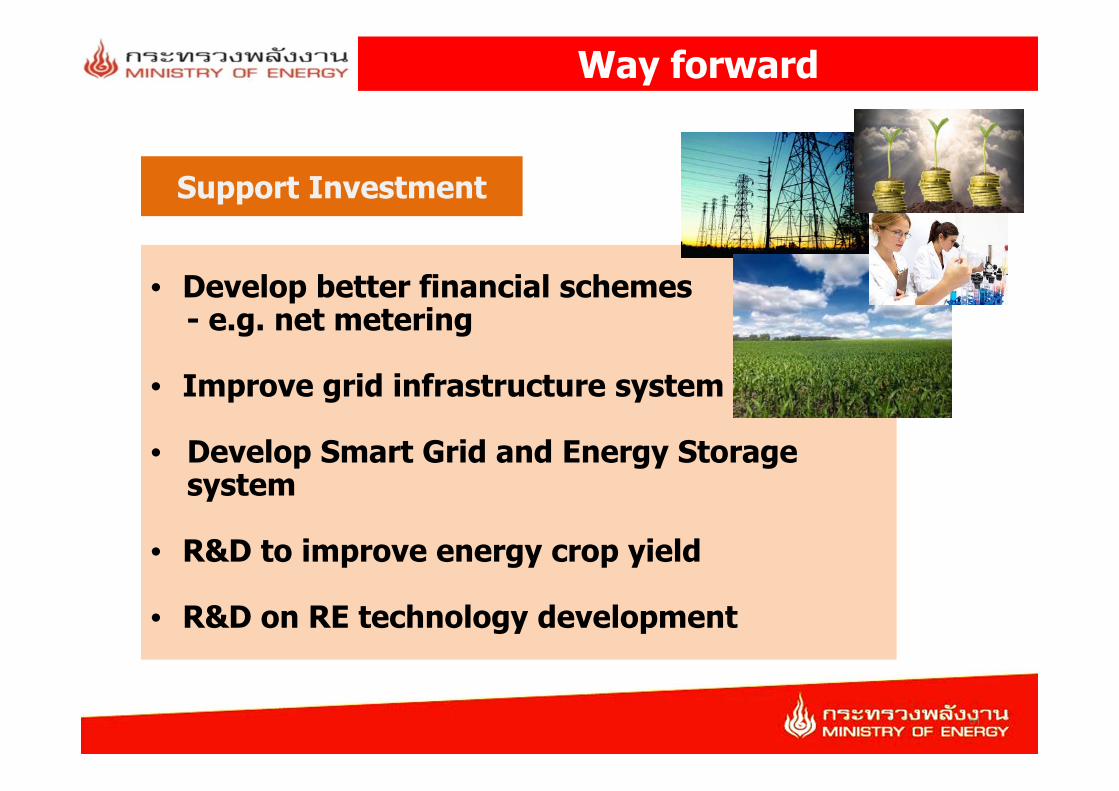

• Develop better financial schemes- e.g. net metering

• Improve grid infrastructure system

• Develop Smart Grid and Energy Storage system

• R&D to improve energy crop yield

• R&D on RE technology development

2

Way forward

Support Investment

51

2

Way forward

Public acceptance

• Promote public understanding/awareness

• Increase community participation

• More acceptable EIA/public hearing process

• Law enforcement on environmental protection

52

2

Way forward

Rules and Regulations

• Facilitate PPA approval

• Deregulate to support RE development

• Standardize RE equipment

53

2

Way forward

Supply of Feedstock

• Zoning for crops

• R&D on feedstock development

• Management of feedstock logistic and supply chain

54

Acceptable

Available

Affordable

55